Back In Vogue: Why A ‘Total China’ Approach With Quality Tilt Is The Way Forward

Chinese equities should be back on investors’ radar screens. Why now? Put simply, the country provides a deep value proposition especially when considering the ‘Total China’ approach. Up until now, investors only had fragments of the story – onshore or offshore. But as the second largest economy, China presents a world of opportunity.

In a nutshell, a ‘Total China’ approach to index investing will:

+ avoid heavily indebted bureaucratic companies, by reducing the exposure to state-owned enterprises (SOEs)

+ embrace new economy sectors of China; these being predominantly IT and consumer stocks that deliver higher return on investments

+ allow for a broadly defined China equity universe that is better diversified and reduces volatility to provide better risk-adjusted returns

Speculative bubble burst presents entry point and value opportunity

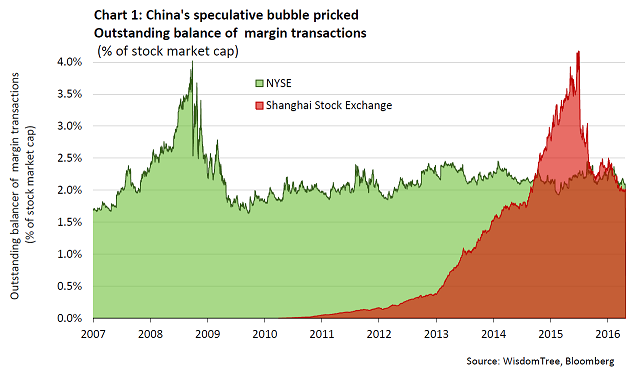

As seen in Chart 1, the Chinese equity bubble burst in the summer of 2015, caused by excessive speculation and poor oversight exposing weaknesses in the financial system which officials have only recently come to grips with. In July 2015, the crisis of confidence reached its peak when a mass suspension of trading meant investors could no longer sell Chinese shares of more than half of all listed companies on the Shanghai and Shenzhen Stock Exchange. Almost RMB 1.5tn (approx. $240bn) of Chinese shares were held by retail investors in margin accounts at the time. Such excessive speculation approximately 4% of the total market cap of The Shanghai Composite – was last observed in US shares in 2008 (mainly in banks and monoline insurers). This has since gradually disappeared as officials curbed excessive speculation and trading Chinese shares on margin. The crackdown has brought speculation back down to levels on par with US shares traded on the NYSE, suggesting speculative positions have dissipated since.

Today, we believe that Chinese equities present a value proposition for investors. At the macro level, China may now also be a good entry point as commodity prices have started to stabilise and government officials are curbing speculation in raw materials prices, most notably in rebar steel. The valuations also look more compelling with a more upbeat outlook for many of its exporters: Mainland and offshore Chinese equity benchmarks trade around 16x and 14x trailing P/E, respectively, and well below their historic average. The equity yield premium over bonds also compares favourably against its own history as well as against peers in Emerging Markets.

Titling towards high profitability and lower leverage stocks

What is left to consider is the basket of China stocks: how does an investor get access to it all? The ‘Total China’ approach is best captured by the S&P China 500 Index. The tilt towards stocks representing China’s new economy will work as an important counterforce and diversifier to the fundamental concerns of investors over China’s old economy stocks being burdened by high indebtedness and poor financial performance.

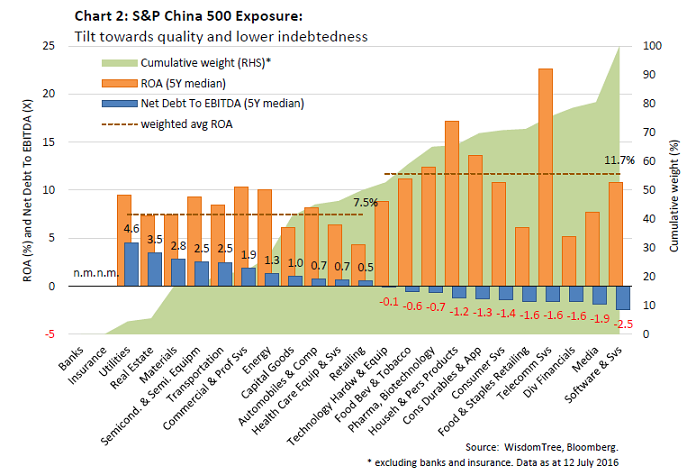

Against this backdrop, the focus will be on quality stocks in China, which could potentially be selected based on companies generating high returns on investments with relatively low debt. The S&P China 500 Index tilts towards such quality stocks, as is also shown in Chart 2. The chart breaks down the Index by Industry Groups to show how the most operationally profitable tend to also be the least leveraged. A significant weight is allocated to such Industry Groups[1].

For instance, when looking at the last five years’ historic fundamentals of the S&P China 500 constituents, nearly half of the 24 GICS Industry Groups show a median net debt to EBITDA ratio below zero (i.e. negative values). With the overwhelming majority of companies having reported positive operating earnings over the period, cash and liquidity is more than enough to pay down debt[2]. The stand out Industry Group having high liquidity and low indebtedness are China’s Information Technology stocks. Representative of these new economy stocks are the likes of Tencent, Baidu and Alibaba which in Q1 2016 reported net debt to EBITDA ratios of -0.4x, -2.5x and -2.4x, respectively. The IT sector overall reported -2.5x net debt to EBITDA on average over the last five years. There are 10 other Industry Groups, most of which are consumer related, that exhibit similar balance sheet strengths of sufficient liquidity to repay debt that collectively contrast the older established industries such as Energy, Materials and Capital Goods, where indebtedness, i.e. financial leverage, has been much higher. Representative of such industries are companies like Sinopec, Baotou Steel and China State Construction Engineering, which have net debt to EBITDA of 2x, 5.5x and 1.9x, respectively.

The apparent link to lower indebtedness of China’s new economy stocks is the much higher levels of return on investments, with consumer and tech related stocks having returned 12% on average, on their total assets (ROA) in the last five years – 4% more than the average ROA of the old economy industries in the same period. Partly responsible for weaker financial performance is the omnipresence of governments which set national interest ahead of shareholders’. As the government is restructuring its state owned enterprises, investors should be mindful that:

+ industrial conglomerates’ restructuring efforts to reduce oversupply, trim a bloated workforce and improve management and bureaucracy, are subject to drawn out timescales. This will force the profit and growth potential to be weighed down for a considerable time thereby minimising the socio-political impact. Nevertheless, given their sheer size and scope, their restructuring potential is significant.

+ Banks will continue to be a vital part of China’s economy as the government orchestrates the rebalancing of its economy predominantly through its control over the “big four” banks: the combined total assets of Industrial and Commercial Bank of China (ICBC), China Construction Bank (CCB), Agricultural Bank of China (ABC) and Bank of China (BoC), is worth $12 trillion. Hence, free-float adjusted or not, the market capitalisation of Chinese banks will rightfully remain very large and as part of the ‘total China’ approach to index investing, a crucial industry to capture China’s domestic growth.

Methodology for ‘Total China’: balanced sector allocation and broader stock mix reduces volatility

Similar to the S&P 500, the main equity index for the US, the S&P China 500 index comprises the 500 largest Chinese stocks by float adjusted market cap. A distinct characteristic is its more balanced sector allocation through including multiple listings (on- and offshore) of different share classes.

The index methodology chooses deliberately not to discriminate between the type of share class or where the stock is listed. A shares, B shares, H shares or ADRs, Shanghai, Hong Kong, US or Singapore listed, Red Chips or P Chips, partially state-owned or 100% free-floating, it does not matter in the screening and selection of stocks. The most important factor is that the company is incorporated in China, its stock is liquid and accessible to foreign investors.

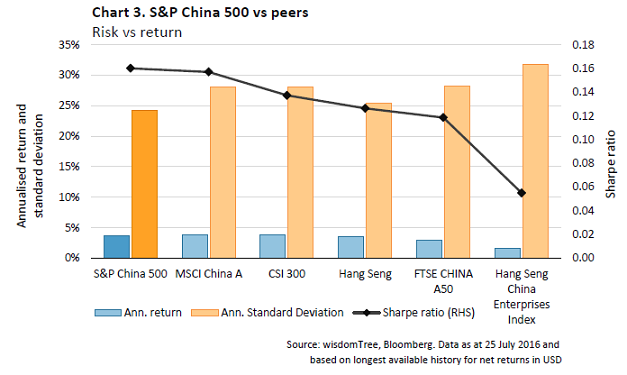

The result is that a broad, all-inclusive index is able to deliver a better diversified basket than alternative benchmarks focused on country of listings and share class type. As also shown in Chart 3, the S&P China 500 index offers a risk-adjusted performance profile that is much improved as a result of its broad mix of different share classes and exchange listings, exhibiting lower volatility than major peers tracking Chinese A or H share classes.

Through smart screening and selection of stocks, no sector is significantly under represented, so as to avoid a consequential sector bias. For instance, consumer stocks known for brand names such as Belle;Want Want; Mengniu;luxury car dealer Brilliance China Automotive, internet retailers and service providers such as Tencent, Alibaba, Baidu, and JD.com are all at the forefront of China’s increasing affluent consumer mass. They are part of the Index because the methodology allows for many of these shares investible only in offshore Chinese listings (US mainly) to be included.

As a majority of Chinese financials companies are large and tend to rank high by market cap, their concentration and sector weight in the large-cap segment tends to be much higher than that in the broad market. To avoid this sector bias, which is seen in many onshore and offshore China large cap indices, the S&P China 500 is designed with a unique feature that approximates sector composition of the broad Chinese equity market[3] during the stock selection process.

In a universe that is otherwise biased towards the large established government controlled companies, the S&P China 500 Index’s all-inclusiveness mitigates such concentration risks and in the process, creates a more balances, more diversified China exposure where the emphasis on quality stocks offers investors a more efficient exposure to the Chinese equity market.

+ ICBCCS WisdomTree S&P China 500 UCITS ETF (CHIN) (Trading Ccy = USD)

+ICBCCS WisdomTree S&P China 500 UCITS ETF (CHIP) (Trading Ccy = GBx)

[1] Because of banks and insurers’ balance sheet liabilities comprising both client and investor funds, debt metrics and operating returns have a lot of distortions that directly cannot be compared against non-financials, Real Estate and Div. Financials. These industry groups have been excluded from the comparison.[3] The S&P Total China BMI index, comprising almost 3000 stock constituents.