ECB QE risks lacking scale, scope, and fiscal support. Position defensively!

A boost to inflation expectations that will reverse deflation in the Eurozone is what the markets hope a large-scale asset purchase program will achieve.

But Limits to the scale and scope of QE - amidst ongoing fiscal tightening and no investment stimulus - risk QE to fail.

The pressure on the euro and sovereigns of Eurozone’s indebted economies is unlikely to ease.

Unless open-ended and unconditional, QE may disappoint investors following the announcement.

Subjecting QE to limitations on its size and scope, driven chiefly by Germany’s insistence to not encourage moral hazard and to not be held liable for potential losses, could risk QE to fall short of what’s required to reflate the Eurozone economy. It would also undermine market’s perception of Draghi’s “whatever it takes” speech when OMT (Outright Monetary Transactions) was announced but never implemented: the promise to fully exhaust all its stimulus options, including buying as many assets as is necessary, for as long as is necessary, to safe the euro. OMT, effectively an implicit promise of QE, was regarded as open-ended and unconditional.

Limiting the asset purchase program by its size, for instance by setting a ceiling of how much of outstanding debt can be bought by the ECB, or restricting it to sovereigns adhering to strict fiscal conditions offer ammunition to speculators to build short positions around Eurozone’s indebted governments most prone to the deflation threat and the rise of fringe parties hostile towards austerity.

Notwithstanding Greece, it is Italy that stands out as the Eurozone member where bond markets may succumb to increased volatility and potentially rising yields, if deflation becomes entrenched. Last year, the nervousness of investors holding Italian BTPs was evident when Italy’s macro indicators disappointed. The release of disappointing 1Q GDP in May and 2Q GDP in August in 2014 led to brief spikes in Italy’s long dated government bond yields. The message of the bond markets therefore is clear: lacklustre growth will be bearish for bonds if it risks entrenching deflation, (much in contrast to a situation where in the presence of inflation, stalling growth is usually bullish for bonds!). As disinflation has slowed down the efforts of the public and private sector in the Eurozone to cut down the level of indebtedness, deflation (by raising the value of real debt and reducing (taxable) income as spending delays are incentivised) works to undermine the deleveraging of balance sheets altogether.

It is likely that the pass-through effects of slumping energy and base metals prices have yet to fully feed through into core consumer prices. Therefore, while upbeat inflation expectations may be building around QE initially, actual deflation may deepen in the Eurozone over the coming months. Given financial markets’ increased sensitivity to weakening CPI readings, the upbeat sentiment may prove to be temporary. It will drive the notion that the overall stimulus of QE is too little and toothless without some degree of fiscal stimulus.

Unless deficit spending is encouraged, deflation will become entrenched

While the ECB can create money, it cannot create aggregate demand. But the domestic demand fallout is what gives deflation in the Eurozone structural causes. This is why the longer term success of ECB’s QE program will hinge on EU leaders to relax budgetary rules and promote investment. It is the growing investment deficit which, since the 2008 credit crisis has failed to sustain output growing close to trend.

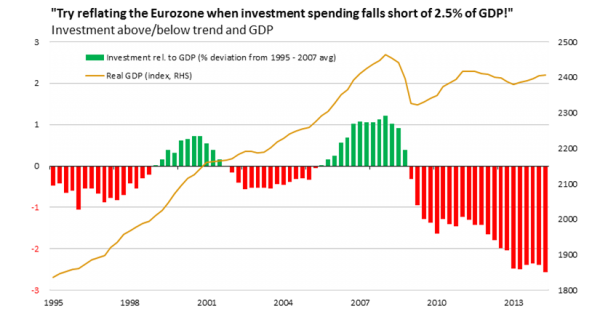

Eurozone’s investment shortfall is significant and, according to our own estimates, has grown from 1.5% in 2010 to 2.5% of GDP in 2014 (see chart below). This is a cumulative investment shortfall of EUR 200 billion which can potentially be closed via a large scalable investment plan, such as endorsed by the EU last year. An initial EUR 21 billion injection of EU money into infrastructure projects should crowd-in private sector capital to potentially grow into a scalable investment stimulus package worth several hundred billion euros. It’s what is needed to give QE support and reverse structural deflation.

Tactically bearish euro and fixed income, bullish Eurozone deep value quality plays

Given the risks outlined above, renewed contagion risk of Greece subjects Italian and Spanish sovereigns to potentially more volatility and rising credit spreads, driving allocations to concentrate within the safest safe havens. Coupled with deflation, further suppression of record low bond yields in Germany and Europe’s healthier core is expected. US’s broad based economic expansion and higher interest rates is also adding further pressure to the euro.

Tactically, investors sharing this sentiment may want to consider the following ETPs:

The low yield but high risk bond environment may entice investors to consider equities with a quality bias.

European equity markets offer comparatively better value than bonds. Cash rich balance sheets and attractive valuations of European stocks mean prospective dividends yields offer investors an historic unprecedented premium to long dated government bond yields. The export bias and global footprint of corporate Europe furthermore mitigate the equity market’s exposure to macro-political risks to which the bond markets will overwhelmingly remain subjected. WisdomTree Europe Equity Income UCITS ETF (EEI) offers investors a 6.3% dividend yield (as of December2014).

Investors sharing this sentiment may want to consider the following ETF: