Positioning defensively in Europe with yield premium intact and more sustainable dividends

Part one of our European index rebalance articles highlighted an investment case for our Eurozone Quality Dividend Growth and Europe Small Cap Dividend strategies. In part two we now explore the valuation, style and country/sector opportunities for WisdomTree's Equity Income and Export-Tilted strategies.

Taken together, these ETFs offer distinctive and unique style strategies that enable investors to position defensively even in the context of Europe’s improving macro-economic backdrop, including:

- a diversified broad exposure of high dividend yielders in Europe and UK, or

- a focused exposure of exporter stocks in the Eurozone and Germany.

If the Eurozone shifts towards economic status quo, political risk will likely revive, resulting in renewed downside pressure on the Euro. In such a scenario, yield over growth would be the preferred strategy, as would be styles emphasising exporter stocks with currency-hedged overlays.

Annual rebalance boosts dividend sustainability for European High Dividend and Export-Tilted strategies

WisdomTree’s Equity Income strategy screens for high-yielding equities in European markets, resulting in a bias towards defensive equities such as EDF, Sanofi-Aventis, Vodafone and GSK, complementing the traditional large-cap oil majors and bank stocks. In contrast to this, WisdomTree’s export-tilted strategy, is a cyclically-biased, narrower equity basket focusing on Eurozone exporters and multi-nationals, including Anheuser-Busch InBev, Unilever, Daimler, BMW, Siemens and BASF.

The annual rebalance has resulted in strengthened investment cases for both strategies, with a marked improvement in fundamentals accompanied by continued attractive valuations that compare favourably against market-cap peers. In summary, the strategies rebalanced into stocks, or remained invested in stocks, that have delivered a recovering trend in earnings and have underpinned their dividends. We summarise our findings in Figures 1 and 2.

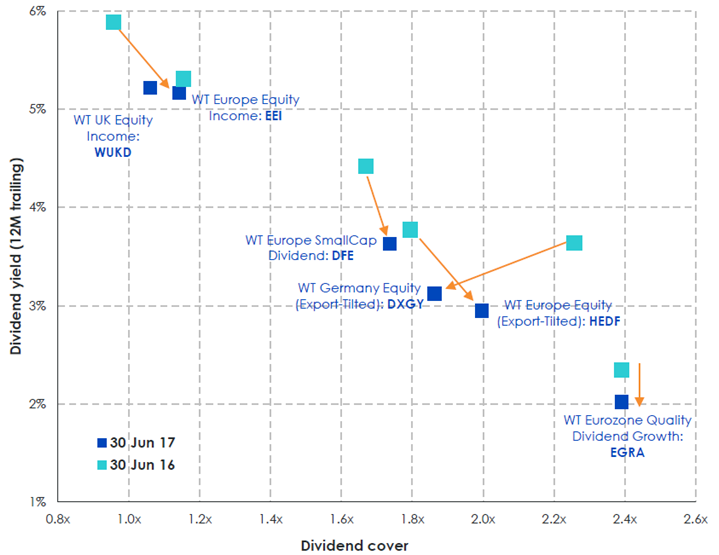

Figure 1 plots the relationship between dividend yield and sustainability, as measured by dividend cover1, for WisdomTree’s European dividend-weighted indices. As can be observed, this year’s rebalance saw an overall improvement in dividend cover with this factor compensating for the decline in dividend yields compared to last year’s rebalance. However, more important is the degree of yield sacrificed to attain a higher dividend cover.

Figure 1: Rebalancing towards dividend sustainability

Dividend yield vs Dividend cover vs. one year ago

Source: WisdomTree, Bloomberg. Data from 30 June 2016 and 30 June 2017

In this context, the most dramatic improvement occurred within Europe Equity Income, our highest yielding European strategy. Whereas Europe Equity Income 5.9% dividend yield looked vulnerable last year against a pay-out ratio above one (hence a dividend cover of < 1x), the rebalance traded a 60 bps loss in dividend yield (to 5.3%) for increased dividend sustainability as the dividend cover increased to 1.15x. A more fundamentally supportive dividend outlook should preserve a still high yield and ease investors’ concerns about potential value traps where pressure on share prices, more than dividend policy, drives the yield. Quite the contrary, against strengthened fundamentals for future dividends, share prices should be supported. The UK equity income strategy saw no significant change as a result of the rebalance: a modest drop in the dividend cover to 1.1x continues to suggest that its 5% dividend yield remains relatively strong.

Perhaps more noteworthy has been the improved dividend profile for WisdomTree's export-tilted strategies, which screen and select stocks based on revenue generated outside of Europe. The stability of large exporters’ revenue streams typically ensures low stock turnover and less change to fundamentals compared to high-dividend yield screening strategies. In keeping with this, across WisdomTree’s European strategies has seen the lowest index turnover (9%) at rebalance, improved its dividend cover to 2x from 1.8x. Only the Germany export-tilted strategy has shown a reduction in dividend sustainability and the dividend yield on offer, whilst lower than the 2.3x after last year’s rebalance it remains relatively high at 1.9x.

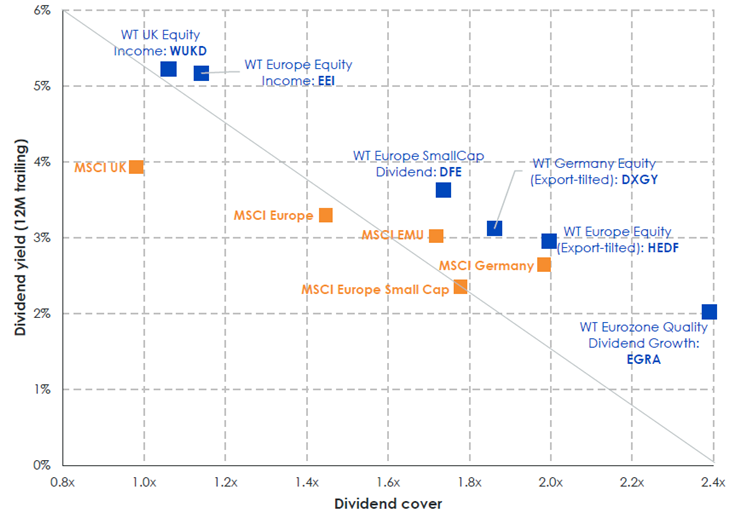

The rebalance has also preserved the attractive valuations and fundamentals for several WisdomTree's strategies compared to their cap-weighted peers, as shown in Figure 2. This comes despite a rotation into more expensive stocks. Post rebalance, the dividend yields of WisdomTree’s equity income strategies continue to trade at a substantial premium to equivalent market-cap based strategies, with equal, if not better, dividend fundamentals also evident.

The Eurozone export-tilted strategy also delivers higher dividend cover for near identical dividend yield when compared to MSCI EMU. The Germany export-tilted strategy on the other hand offers investors a negligible trade-off compared to market cap: a premium dividend yield comes at the expense of a lower dividend cover, although at 1.9x, the dividend cover is arguably not undermining the 3.1% dividend yield, which is substantially more than market-cap.

Figure 2: Dividend sustainability: Dividend yield vs dividend cover

vs. benchmarks

Source: WisdomTree, Bloomberg. Data as of 30 June 2017.

Equity Income and Currency-Hedged Exporters offer a defensive choice

Underpinning the defensive nature of equity income and export-tilted strategies is the prospect of rising market tensions predicated on the likelihood of a Five Star Movement victory in Italy’s election. Of equal concern is the potential for Macron failing to deliver on his reform agenda resulting in an economically risky outcome that reinforces a status quo of no reform. Both scenarios threaten to derail Europe’s economic momentum, intensifying downwards pressure on the Euro and potentially enticing the ECB to prolong monetary easing.

Such a backdrop favours defensive equity sectors such as Telecoms, Utilities and Health Care, whereby the low-beta nature of these sectors helps dampen market volatility. At 35%, Europe Equity Income offers significant exposure to these sectors, alongside large non-Eurozone geographic exposure (UK, Nordics and Switzerland) of 48% that helps insulate against Euro political and economic uncertainty.

Alternatively, Eurozone exporters also offer an attractive defensive bet, with renewed pressure on the Euro presenting a boon to Eurozone multinationals as investors upgrade top and bottom-line growth expectations. WisdomTree’s export-tilted strategies may offer an efficient means to achieve this having recently rebalanced into more export-oriented sectors such as Materials, whilst preserving the underweight in Financials. Investors looking to discriminate between exporters further may also consider greater defensive tilt as a result of overweighting consumer staples.

The most important feature of the export-tilted strategies however, is the availability of currency-hedged overlays in various currencies. Both Eurozone and German exporters can be hedged into USD or GBP, allowing investors to position around Euro FX volatility or mitigate currency risk altogether.

Conclusion

The annual rebalance of WisdomTree’s European Equity ETFs have fundamentally strengthened the investment case of the different styles and strategies available for income orientated investors seeking exposure to Europe. The markedly improved post-rebalance valuations, and the fundamentals underpinning them, continue to compare favourably against market-cap weighted alternatives.

The defensive tilt offered by Equity Income coupled with the global multinational exposure of European exporters offer an attractive means to position around Europe's political and economic risk.

You may also be interested in reading…

Source

1 Dividend cover refers to ratio at which earnings per share covers dividend distributions per share.