Macro Outlook for Europe: Structurally-Led, Europe’s Domestic Growth Presents an Opportunity For Small-Caps in 2017

Europe’s investment case is underpinned by a structurally-led – and not a cyclically-led economic recovery. We anticipate growth to pick up over the course of the next 12 months, propelled by consumer spending mainly in the Eurozone and the UK, along with a modest pickup in investment spending. Net exports and government spending will work as stabilisers but not drivers for growth.

This recovery is unlikely to be cut short by political uncertainty despite talk of triggering Article 50 in the UK and the 2017 general elections in France and Germany: Brexit is already priced-in. The floor to Europe’s downside risk to political events remains the ECB ultra-loose policy stance.

More fiscal stimulus and QE directed towards long term bonds boosting strategic investments in Europe are expected in 2017. Suppression of high-grade bond yields and flat yield curves will continue to justify a re-rating of European equities.

Our investment case for Europe is clear: domestic growth and quality, small caps and broad exposures emphasising the consumer and industrials sectors.

Positioning for European growth with small cap dividend payers

Chart 1 summarises our investment case for Europe. It shows the performance of the WisdomTree Small Cap Dividend strategy since July 2006, broken down by its core components: dividends, earnings and valuation. It shows how the cumulative contribution of each has shifted gradually towards strengthening equity fundamentals: stable dividend returns, falling valuation risk and rising earnings.

Past performance is not indicative of future returns

As has been the case for all risk assets, the ECB’s actions in 2012 to restore confidence in Europe’s banking sector and bond markets has triggered a major re-rating of equities, including European small caps. This re-rating continued as exceptional monetary stimulus by the ECB and recently the BoE pushed bond yields of European high-grade issuers to historic lows.

But since mid-2015, the performance of Europe’s small-cap dividend payers has been increasingly carried by strengthening fundamentals that have underpinned their re-rating: earnings have started to accelerate and together with steady dividend streams, which have accounted for nearly half the shareholder’s net total return over the entire equity market cycle, have caught up with stock prices.

In our view, it’s a result of a resilient and more confident consumer in Europe who, coupled with banks acting as willing lenders and monetary policies stimulating investments, underpins a sustainable path for stronger economic growth. Biased towards Consumer Discretionary, IT, Industrials and Financials, the basket is well positioned for the domestic demand-led transformation of Europe.

Improved competitiveness and easing credit conditions bolsters spending power

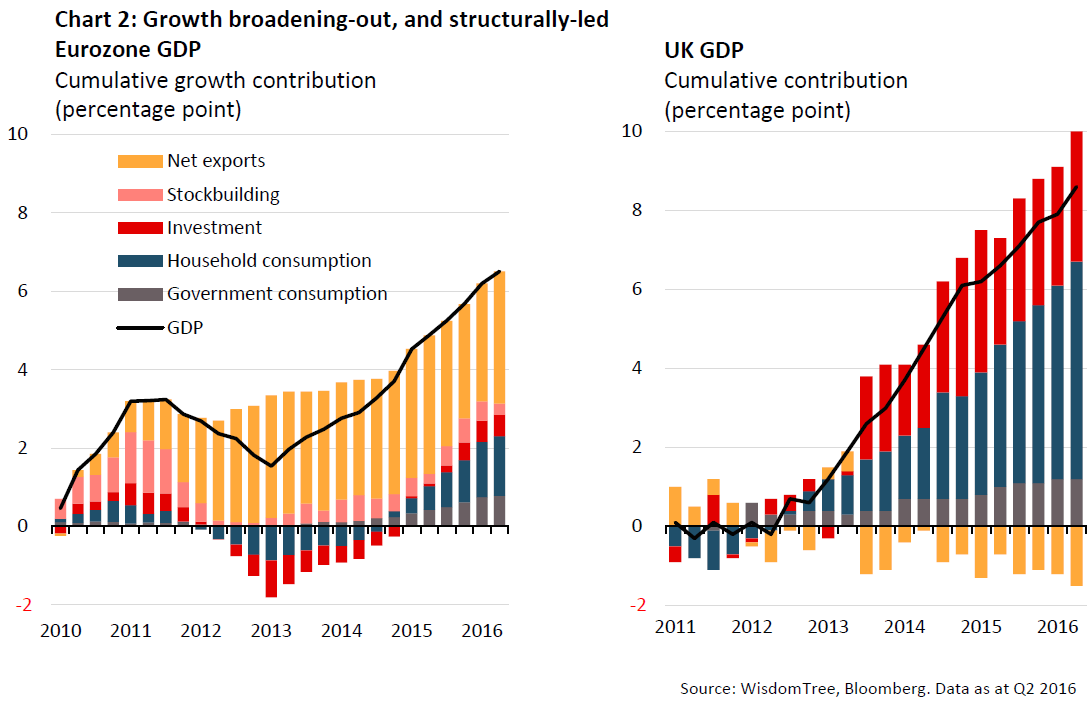

Chart 2 shows how Eurozone’s economic rebalancing since 2010 – away from cyclical, export-led to structural, domestic demand-led – has broadened-out growth and laid the foundations to quicken the pace of expansion similar to the UK. Driving this trend into 2017 is a more competitive labour force and banks willing to extend cheaper loans.

The relentless wage suppression, effectively occurring when the last round of automatic stabilisers used as shock absorbers by the governments during the financial crisis got wound down in 2010 is showing signs of abating. After private sector wages have been falling in real terms in Europe’s periphery and frozen across most of Europe’s core (excluding Germany) for five years, this ‘internal devaluation’ is starting to pay off with regained cost competitiveness. For instance, unit labour costs in Italy and France have fallen by 7.1% and 6.7%, respectively, relative to Germany’s since 2010. Helped by inflation-busting pay rises being negotiated by labour unions and employers in Germany, the downward pressure on wages in France and Italy is easing, allowing more room for Eurozone’s 2nd and 3rd largest members to raise spending.

The boost to consumer confidence delivers the positive feedback loop to the banking sector too, as the evaporating carry trade in high-grade debt instigated by QE incentivises banks to reinvigorate the loan book and ease credit conditions to households and businesses. September’s TLTRO by the banks was strong, suggesting that with the EBA’s bank stress test out of the way, banks will be looking to fully leverage up and exploit their access to ultra-cheap loans as their best option to reflate their net lending margins. We expect their take-up in December 2016 and March 2017 TLTRO allotments to be even stronger.

Political risk containable with mainstream parties’ compromising to fringe-party demands

The macro imbalance inflicted the UK economy as a result of Brexit has already played out in currency markets: the marked devaluation of sterling of around 12% to the dollar and euro since the outcome of the EU referendum (24/06/17)[1], adjusts for a deteriorating current account as financial services –the major contributor to UK’s total services trade surplus – risks losing EU passporting rights. To limit the damage to banks and insurers in the UK of losing access to Europe’s single market, a watered down version of Britain’s exit from the EU is the most likely scenario. Article 50, the motion that officially triggers UK’s break-up from the EU, will be pushed down the road as far as possible to allow time for the UK to strike the best deal. This prolonged uncertainty is expected to weaken UK’s economic outlook as trade and investment with the EU is held back, which in our view reflects why sterling’s marked devaluation should persist.

The political uncertainty leading up to the general elections in France and Germany in 2017 may drive a modest pickup in volatility in the euro, but not expected to derail Eurozone’s structurally-led recovery. Fending off the rise of extreme left and right-wing movements, the mainstream political parties will in all likelihood coalesce around embracing two central themes driving voter sentiment into the right and left-wing movements in Europe: more immigration control and less austerity.

Leaders of the main parties in France and Germany have little choice, as do EU officials in Brussels. For the latter it’s all about preserving the European project. For France, terrorist attacks are forcing President Hollande to toughen rhetoric on immigration and for ramping up security and policing. For Chancellor Merkel the pressure is now coming from within her own party, the CDU, which has lost badly in this year’s local elections.

While the likely outcomes in France’s election is not going to pose a threat to its EU membership, the chance of leadership change from Chancellor Merkel or the CDU losing out to fringe parties, means there will be some uncertainty over who will lead as a consensus-builder in EU-wide policymaking. We remain relatively sanguine about potential leadership in Germany as no matter who gets elected the next Chancellor, a tougher immigration policy will be, in all likelihood, quietly endorsed by politicians both within Germany and in Europe and unlikely to cut short the recovery.

ECB to anchor inflation expectations with rhetoric and targeted QE

The ECB will use rhetoric, not policy actions, to keep the spectre of inflation alive, to preserve its credibility and talk down the euro. For the southern peripheral countries whose exports compete less on quality and more on price the low euro remains an important stabiliser and shock absorber to the internal devaluation occurring in their labour markets.

The euro is expected to remain relatively volatile relative to the dollar, with the currency’s fundamentals – in spite of the improving economic growth for the Eurozone still stacked against the euro. The ECB’s QE and Draghi’s inflation rhetoric, along with a tightening US labour market conditions potentially driving a December rate hike are exacerbating downward pressure on the euro.

The ECB, in our view, will be aiming its bond buying programme at boosting discretionary spending by governments and businesses. The reason for this is the acute shortfall of investments in the Eurozone since 2009. We estimate this to have been as much as 2.5% of GDP per year, equivalent to a cumulative underinvestment of EUR 1.6 trillion to date. In Draghi’s press conference held in June, he referred to EU Commissioner Jean Claude Junker’s “Investment Plan for Europe” as a much needed trigger for growth. It’s an implicit acknowledgement that public funding will crowd-in and not crowd out private investments.

Over the months ahead, the QE programme will potentially focus on increasing it purchases of long-term bonds of public and private issuers promoting strategic investments in areas such as infrastructure, education, research and technology. The low yielding environment is to persist in this backdrop, with little downside risk expected for high-grade credit issuers in the Eurozone.

Conclusion

Europe is emerging out of an inflection point where consumer propensity to spend is improving. The region receives support from the BoE with the ECB accommodating (investment) spending with ultra-loose and targeted monetary policy and banks extending credit willingly. Domestic demand focused stocks in Europe are likely to benefit with this backdrop.