WisdomTree 1-Day Equity Put Premium

WisdomTree 1-Day Equity Put Premium is a fully collateralised, UCITS eligible Exchange Traded Product (ETP) designed to provide investors with a total return exposure to a systematic daily put writing (selling) strategy. The ETP aims to replicate the Daily US Equity Put Premium Total Return (TR) Index by tracking the Daily US Equity Put Premium Excess Return (ER) Index and adding the associated interest revenue, adjusted to reflect fees and costs of the product.

For example, if the Daily US Equity Put Premium TR Index rises by 1% over a day, then the ETP will rise by 1%, excluding fees. However, if the Index falls by 1% over a day, then the ETP will fall by 1%, excluding fees.

The Index provides exposure to a systematic, daily, deep out-of-the-money (DOTM) put writing strategy seeking to generate positive returns that display a low degree of correlation to broader equity markets.

At any given time, the Index will hold three short put positions, each with a notional of 100%. This means that the total exposure of the index will be 300%.

The index incorporates an adjustment to reflect costs associated with maintaining the relevant underlying exposure. This adjustment is embedded in the Index / Sub-index level as part of the Index calculation methodology.

Why Invest?

- Gain exposure to a systematic premium driven by demand for downside protection, which tends to make deep out-of-the-money put options consistently more expensive.

- Smooth return profile with limited correlation to equity markets.

- Easy to invest: rules-based exposure to a systematic daily put-selling strategy without the need to manage option positions.

- UCITS eligible and fully collateralised.

- Transparent performance and fees.

- Risk Management: You cannot lose more than the amount invested.

- Liquidity: Trades on exchange, with multiple authorised participants (APs) and market makers (MMs).

Potential Risks

- An investment in an ETP involves a degree of risk. Any decision to invest should be based on the information contained in the relevant prospectus. Prospective investors should obtain independent accounting, tax and legal advice and should consult their professional advisers to ascertain the suitability of this ETP as an investment to their own circumstances.

- This ETP is structured as a debt security and not as shares (equity) and can be created and redeemed on demand by authorised participants and traded on exchange just like shares in a company. This ETP is not a UCITS product.

- Investing in ETPs that incorporate leverage is only suitable for sophisticated and or informed investors who understand leverage, impact of rebalancing and compounded returns and are willing to magnify potential losses. Any investment in a short or leveraged ETP should be monitored regularly to ensure consistency with your investment strategy.

- Market Risk: The value of securities in this ETP is directly affected by increases and decreases in the value of the Index. Accordingly, the value of a security may go up or down and a security holder may lose some or all of the amount invested, but can not lose more than the amount invested.

- Liquidity risk: There can be no certainty that securities can always be bought or sold on a stock exchange or that the market price at which the securities may be traded on an exchange will always accurately reflect the performance of the Index.

- Currency Risk: The price of securities in this ETP is generally quoted in USD. To the extent that a security holder purchases securities in another currency, the value will be affected by changes in the exchange rate.

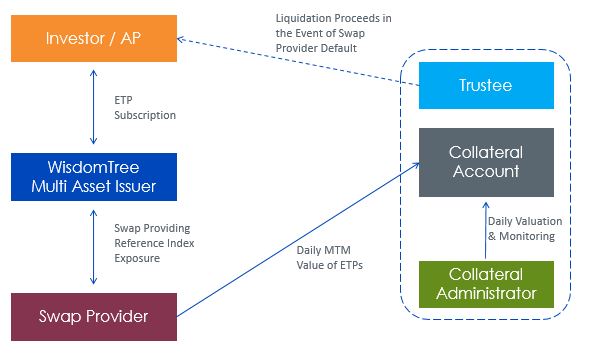

- Counterparty risk: The Issuer is reliant on there being swap counterparties available to enter into swap agreements on a continuing basis, and if no swap counterparties are willing to do so, the ETP will not be able to achieve its investment policy of tracking the performance of the Index.

- Credit Risk: The Issuer is subject to the risk that third-party service providers may fail to return property or collateral belonging to the Issuer or pay money due to the Issuer. The ETP is backed by swaps. The payment obligations of the swap counterparties to the Issuer are protected by collateral held, which is marked to market daily. The collateral is held in segregated accounts at The Bank of New York Mellon. In the event a swap counterparty defaults, the proceeds from the realisation of the collateral may be less than what the investor expects. Details of the collateral held can be found in the Collateral section of the WisdomTree website (www.wisdomtree.com).

- Option Selling Risk: options on equity indices may be subject to volatile swings in price influenced by changes in the value of the underlying instrument. The seller (writer) of a put option assumes the risk of a drop in the market price of the underlying below the strike price of the put option in exchange for the payment of a premium by the option buyer.

- Risk of Large Losses: The strategy earns small, frequent option premiums but may incur significant losses if the S&P 500 Index experiences a prolonged negative return environment.

- Volatility Risk: The strategy can be negatively affected by abrupt increases in market volatility. When volatility rises significantly within a short time period, the probability of sold options expiring in the money may increase, leading to losses.

- Non-Linear Returns Risk: Losses may increase more rapidly than gains. In falling markets, the value of the investment may decline disproportionately.

- Crowding Risk: If many investors follow similar strategies, returns may be reduced and losses may be amplified during periods of market stress.

- Income Not Guaranteed: Although the strategy aims to generate income, this is not guaranteed and investors may lose part or all of their investment.

- Please see the risk factors section of the Prospectus for a more detailed discussion of the potential risks.

Overview

| Product Overview | |

|---|---|

| Base/Trading Currency | USD/EUR |

| Bloomberg Ticker | 1PUT IM |

| Index Bloomberg Ticker | BNPXTU21 |

| Index Name | Daily US Equity Put Premium TR Index |

| ISIN | XS3330165328 |

| Leverage Factor | N/A |

| Structure | |

|---|---|

| Physical Assets | Yes (Collateral) |

| Structure | ETP |

| Domicile | Ireland |

| Replication Method | Fully Collateralised Swap |

| Legal form | Debt security |

| Further Legal and Tax Information | |

|---|---|

| ISA | Eligible |

| SIPP | Eligible |

| UCITS Eligible | Eligible |

| UK Fund Reporting Status | Yes |

| Key Service Providers | |

|---|---|

| Issuers | WisdomTree Multi Asset Issuer PLC |

| Administrator | Apex IFS Limited |

| Custodian | Bank of New York Mellon |

| Trustee | Law Debenture Trust |

| Auditor | Deloitte LLP |

| Swap Provider | BNP Paribas Arbitrage SNC |

| Market Makers | Market Makers |

| Authorised Participants | APs |

| Fees | |

|---|---|

| Annual Management Fee Rate | 0.34% |

| Annual Swap Rate | 0.25% |

Listings & Codes

| Listings & Codes | ||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

||||||||||||||||||||||

|

||||||||||||||||||||||

|

||||||||||||||||||||||

|

Index Details

Daily US Equity Put Premium Index

The Daily US Equity Put Premium ER Index (the “Index”) is a BNP Paribas index designed to implement systematic options-based strategies that seek to generate income through the sale of short-dated, deep out of the money put options on the S&P 500 Index. Each day, the indices notionally sell three short-dated, deep out-of-the-money put options on the S&P 500 Index, taking advantage of time decay acceleration close to the option expiry as well as elevated implied volatilities for deeply out-of-the-money put options (“volatility skew”).

When an investor sells an option, they receive an upfront premium from the option buyer. This premium represents the compensation for assuming the risk that the S&P 500 Index may fall below the strike price of the option during the option’s one-day life. Because the options sold by the strategy are short dated (one trading day to maturity), and set with strike levels significantly below the prevailing market, the daily premiums received are, on an absolute basis, typically smaller than those of longer dated or at the money options, but accrue more frequently due to the strategy’s daily rebalancing. The cumulative effect of receiving these small, recurring option premiums is the primary source of income for the strategy.

More information on the above Index, such as details of the index calculation and construction methodology, appears in the index handbook, which can be found at: https://indx.bnpparibas.com/.

| Index Details | |

|---|---|

| Index Name | Daily US Equity Put Premium TR Index |

| Currency | USD |

| Index Provider | BNP Paribas |

| Bloomberg Ticker | BNPXTU21 |

| Leverage Method | No Leverage |

| Documents and Links |

|---|

Collateral Details

| Collateral Details | |

|---|---|

| Collateral Coverage Ratio | 105.0% |

| Collateralised | Yes |

| Over Collateralised | Yes |

| Custodian | Bank of New York Mellon |

Collateral Structure

Documents

Historical Data

WisdomTree Multi Asset Issuer PLC (the “Issuer”) issues products under a Prospectus (“WTMA Prospectus”) approved by the Central Bank of Ireland, drawn up in accordance with the Directive 2003/71/EC. The WTMA Prospectus has been passported to various European jurisdictions including the UK, Italy and Germany and is available on this document.

Options on equity indices may be subject to volatile swings in price influenced by changes in the value of the underlying instrument. The seller (writer) of a put option assumes the risk of a drop in the market price of the underlying below the strike price of the put option in exchange for the payment of a premium by the option buyer.

The strategy earns small, frequent option premiums but may incur significant losses if the S&P 500 Index experiences a prolonged negative return environment.

The Daily US Equity Put Premium Excess Return (ER) Index & Daily US Equity Put Premium Total Return (TR) Index is the exclusive property of BNP Paribas (“BNPP”). The Daily US Equity Put Premium Excess Return (ER) Index & Daily US Equity Put Premium Total Return (TR) Index is used by WisdomTree under licence. The Index-linked Securities are not endorsed or approved in any way by BNPP. BNPP do not make any warranties whatsoever in relation to use of The Daily US Equity Put Premium Excess Return (ER) Index & Daily US Equity Put Premium Total Return (TR) Index and are not liable for any losses caused by the use thereof.

The methodology of and rules governing the index (the ""Index Methodology"" and the ""Index"") are proprietary. None of the sponsor of the Index (the ""Index Sponsor""), the index calculation agent (where such party is not also the Index Sponsor, the ""Index Calculation Agent"") nor, where applicable, the index Investment Advisor (the ""Index Investment Advisor"") guarantee that there will be no errors or omissions in computing or disseminating the Index.

The Index Methodology is based on certain assumptions, certain pricing models and calculation methods adopted by the Index Sponsor, the Index Calculation Agent and, where applicable, the Index Investment Advisor, and may have certain inherent limitations. Information prepared on the basis of different models, calculation methods or assumptions may yield different results. You have no authority to use or reproduce the Index Methodology in any way, and neither BNP Paribas nor any of its affiliates shall be liable for any loss whatsoever, whether arising directly or indirectly from the use of the Index or Index Methodology or otherwise in connection therewith.

The Index Sponsor reserves the right to amend or adjust the Index Methodology from time to time in accordance with the rules governing the Index and accepts no liability for any such amendment or adjustment. Neither the Index Sponsor nor the Index Calculation Agent are under any obligation to continue the calculation, publication or dissemination of the Index and accept no liability for any suspension or interruption in the calculation thereof which is made in accordance with the rules governing the Index. None of the Index Sponsor, the Index Calculation Agent nor, where applicable, the Index Investment Advisor accept any liability in connection with the publication or use of the level of the Index at any given time.

The Index Methodology embeds certain costs in the strategy which cover amongst other things, friction, replication and repo costs in running the Index. The levels of such costs (if any) may vary over time in accordance with market conditions as determined by the Index Sponsor acting in a commercially reasonable manner.

BNP Paribas and its affiliates may enter into derivative transactions or issue financial instruments (together, the ""Products"") linked to the Index. The Products are not in any way sponsored, endorsed, sold or promoted by the sponsor of any index component (or part thereof) which may comprise the Index (each a ""Reference Index"") that is not affiliated with BNP Paribas (each such sponsor, a ""Reference Index Sponsor""). The Reference Index Sponsors make no representation whatsoever, whether express or implied, either as to the results to be obtained from the use of the relevant Reference Index and/or the levels at which the relevant Reference Index stands at any particular time on any particular date or otherwise. No Reference Index Sponsor shall be liable (whether in negligence or otherwise) to any person for any error in the relevant Reference Index and the relevant Reference Index Sponsor is under no obligation to advise any person of any error therein. None of the Reference Index Sponsors makes any representation whatsoever, whether express or implied, as to the advisability of purchasing or assuming any risk in connection with the Products. BNP Paribas and its affiliates have no rights against or recourse to any Reference Index Sponsor should any Reference Index not be published or for any errors in the calculation thereof or on any other basis whatsoever in relation to any Reference Index, its production, or the level or constituents thereof. BNP Paribas and its affiliates shall have no liability to any party for any act or failure to act by any Reference Index Sponsor in connection with the calculation, adjustment or maintenance of the relevant Reference Index and have no affiliation with or control over any Reference Index or the relevant Reference Index Sponsor or the computation, composition or dissemination of any Reference Index. Although the Index Calculation Agent will obtain information concerning each Reference Index from publicly available sources that it believes reliable, it will not independently verify this information. Accordingly, no representation, warranty or undertaking (express or implied) is made and no responsibility is accepted by BNP Paribas or any of its affiliates nor the Index Calculation Agent as to the accuracy, completeness and timeliness of information concerning any Reference Index.

BNP Paribas and/or its affiliates may act in a number of different capacities in relation to the Index and/or products linked to the Index, which may include, but not be limited to, acting as market-maker, hedging counterparty, issuer of components of the Index, Index Sponsor and/or Index Calculation Agent. Such activities could result in potential conflicts of interest that could influence the price or value of a Product.

© BNP Paribas. All rights reserved.".