The income imperative: why high dividend equities belong at the core of every portfolio

Key Takeaways

- Reinvested dividends account for the overwhelming majority of real long-run equity wealth accumulation, making income generation a core, not peripheral, portfolio objective.

- The current macroeconomic backdrop (high energy prices, sticky inflation and heightened volatility) creates a particularly strong environment for high dividend strategies.

- A globally diversified, fundamentally weighted dividend strategy provides geographic and sector balance unavailable in single-region income products, while trading at a material valuation discount to the broad market.

- Related Products WisdomTree Global High Dividend UCITS ETF - USD Find out more

The enduring case for high dividend-yielding equities

High dividend yield strategies have long served as a cornerstone of sophisticated equity income portfolios. Yet in the current environment, the appeal extends well beyond the simple mechanics of income generation. For investors seeking resilient, risk-adjusted returns amid elevated macroeconomic volatility, dividend-focused equities may offer a strong investment proposition.

- A reliable and compounding income stream: Dividends have historically contributed a significant proportion of total equity returns over the long run, accounting for more than 40% of total equity market returns over the past century on a global basis1. Unlike capital gains, dividend income provides a visible, recurring cash flow that compounds powerfully over time. For liability-driven investors, defined benefit schemes, and income-oriented mandates, it is a structural requirement.

- Downside protection and lower drawdowns: Historically, dividend-paying companies have exhibited lower drawdowns during periods of market stress than some non-dividend-paying companies, although this has not been consistent across all market environments. The income cushion partially offsets capital declines, while the quality bias inherent in dividend selection tends to skew portfolios away from speculative, capital-hungry businesses that are most vulnerable to tightening financial conditions.

- Inflation linkage and real return preservation: Companies with pricing power (utilities, financials, energy majors, and consumer staples) often feature prominently in high dividend universes. Many can pass through inflationary cost pressures to end customers, which may help support returns during periods of elevated inflation.

The macro backdrop: why now matters

The current macroeconomic backdrop strengthens the structural case for high dividend equities. Three interlinked forces are reshaping the investment landscape in ways that are directly advantageous to high dividend strategies. Firstly, the US-Iran conflict has introduced a significant and sustained risk premium into global energy markets. With Brent crude elevated and supply-chain disruption cascading across oil-dependent sectors, headline inflation is proving stickier than central bank projections anticipated. For dividend investors, this creates two tailwinds: energy-sector constituents, which feature prominently in high-yield indices, are direct beneficiaries of elevated oil prices, and dividend yields gain relative attractiveness as real fixed-income yields come under pressure.

Secondly, in a regime of structurally higher inflation, the real yield on government bonds, even with nominal rates elevated, remains compressed. Equities yielding 3-4%, particularly when backed by dividend growth potential, may offer a stronger risk-adjusted income profile than investment-grade or short-duration fixed income.

Lastly, market volatility has been elevated throughout 2025–2026, reflecting geopolitical uncertainty, central bank policy divergence, and weakening global growth momentum. In such environments, portfolios anchored to cash-generative, dividend-paying businesses tend to demonstrate superior risk-adjusted performance.

This is because dividend income may provide a partial cushion during periods of market weakness: as prices fall, yields rise, attracting incremental buyers and compressing drawdowns relative to growth-oriented benchmarks. Furthermore, dividend streams are typically less volatile than earnings or price momentum, providing portfolio anchoring during periods of macroeconomic turbulence.

Introducing the WisdomTree Global High Dividend UCITS ETF

Against this backdrop, WisdomTree has launched of the WisdomTree Global High Dividend UCITS ETF (Ticker: WDIV). The fund tracks the WisdomTree Global High Dividend UCITS Index (Ticker: WTGDHYU), a proprietary, fundamentally-weighted index designed to deliver exposure to high dividend yielding companies across developed global markets, while actively screening for quality and sustainability to reduce the risk of value traps.

The index is built on three core design principles:

- Income-oriented: The Index targets companies in the top 30% by dividend yield within their region and Global Industry Classification Standard (GICS) sector, delivering a portfolio yield that is materially above market-cap weighted benchmarks.

- Quality-aware: Eligible companies are scored on a composite risk factor, equally weighting two signals: a Quality factor, measuring return on equity, return on assets, gross profitability and cash flow quality, scored within industry groups and a Momentum factor, measuring risk-adjusted price returns over 6 and 12 months to identify stocks with deteriorating market signals. Companies in the bottom decile of this composite score are excluded entirely. Critically, companies in the top 5% by dividend yield that also score in the bottom half of the composite risk score are removed as this is the index's explicit yield trap screen.

- Fundamentally weighted: Rather than weighting by market capitalisation, the index weights constituents by their dividend stream (annual dividend × shares outstanding), amplified by a 1.5× quality multiplier for companies that fall within the top two deciles of the composite risk factor. This tilts the portfolio towards larger, higher- dividend payers and away from the price-momentum bias inherent in cap-weighted indices.

Why WisdomTree launched the Global High Dividend UCITS ETF

WisdomTree has been a global pioneer in dividend-weighted equity strategies for over two decades, with a live track record in dividend investing that spans multiple market cycles. The launch reflects three clear strategic imperatives:

- Strong investor demand: Equity income strategies continue to attract robust inflows across retail and institutional channels globally, reflecting a structural shift in portfolio construction towards income generation.

- Portfolio completion: The WisdomTree Global High Dividend exchange-traded fund (ETF) provides a genuinely global dividend vehicle that completes WisdomTree's High Dividend family, which already includes dedicated US, European, and Emerging Market high dividend ETFs with a unified global solution built on the same investment philosophy, index construction principles and ESG screening framework.

- Differentiated design: The Index applies a more rigorous dividend sustainability screen than many competing products and is designed to help address one of the common risks associated with high dividend strategies.

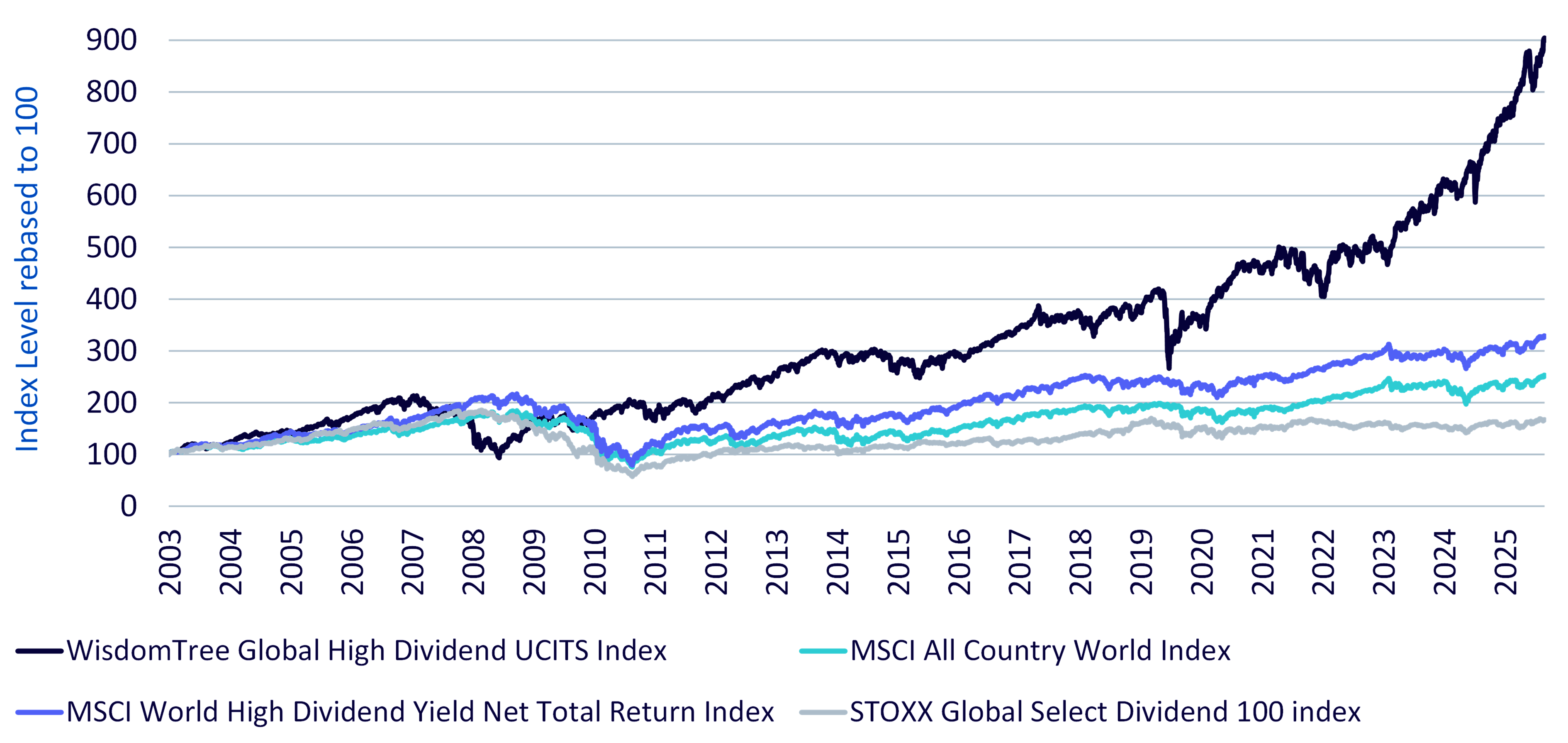

Backtested historical performance

The figure below illustrates the simulated performance of the Index against the MSCI All Country World Index (ACWI), the MSCI World High Dividend Yield Net Total Return Index and the Stoxx Global Select Dividend 100 Index since 29 September 2003, capturing multiple full market cycles including the Global Financial Crisis and the COVID-19 pandemic. The backtest indicates that the Index would have outperformed the referenced benchmarks over the period shown.

Figure 1: Backtest of WisdomTree’s Global High Dividend UCITS Index versus peers

Source: FactSet, Bloomberg Finance L.P., WisdomTree from 30 September 2003 to 29 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

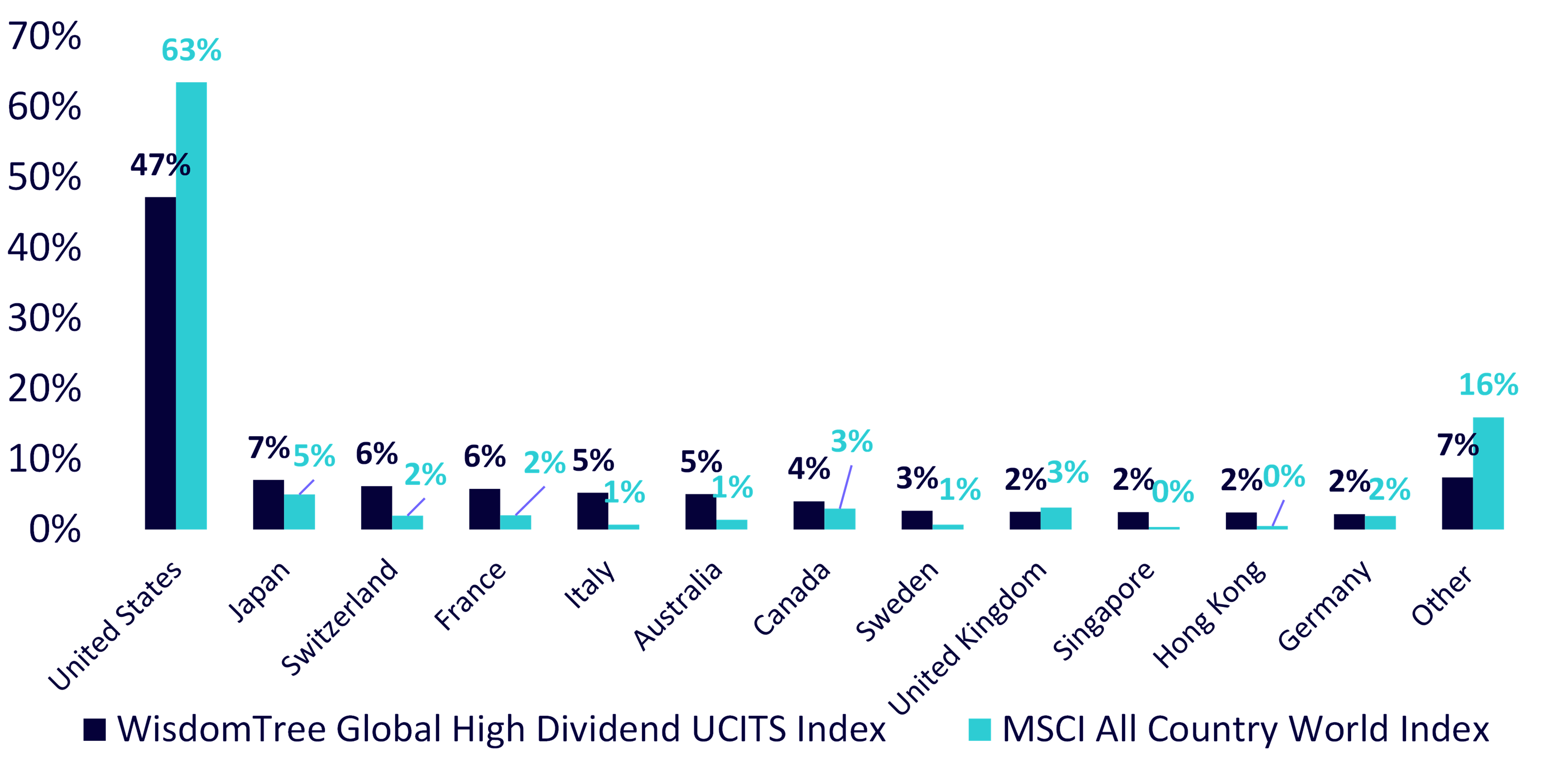

Portfolio tilts: geographic allocation

WisdomTree’s Global High Dividend UCITS ETF maintains a distinctly different regional profile versus the MSCI All Country World Index (ACWI). While US equities remain the single largest allocation (47.2%), the Index is materially underweight the US relative to market capitalisation benchmarks. This reflects the dividend-weighted construction: high dividend payers are disproportionately represented in Europe, Japan, Australia and Asia, where corporate payout cultures are more entrenched. Switzerland (6.2%), France (5.8%), Italy (5.2%), Australia (5.0%) and Japan (7.0%) all feature as significant overweights versus MSCI ACWI weights.

Figure 2: Comparison of geographic allocation

Source: FactSet, WisdomTree as of 29 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Portfolio tilts: sector allocation

The Index's sector profile reflects the distribution of dividend-paying quality companies globally. Financials (22.6%), information technology (18.7%) and health care (18.7%) represent the three largest sector exposures. The technology weight benefits from large, highly cash-generative technology companies that have materially grown their dividends in recent years, an often-overlooked feature of the Global High Dividend index methodology versus older dividend indices that are structurally underweight technology. The Index is significantly underweight information technology relative to MSCI ACWI (18.7% versus 32.2%), with the difference largely offset by higher allocations to financials, health care and utilities. This results in a more diversified sector mix and a risk profile that is better aligned with income generation.

Figure 3: Comparison of sector allocation

Source: FactSet, WisdomTree as of 29 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Fundamental characteristics

The Index trades at a meaningful valuation discount to the broad global benchmark, with a forward P/E of 14.3x compared with 18.5x for MSCI ACWI, and a price-to-book ratio of 2.4x versus 4.0x. It also has historically exhibited a dividend yield above that of the MSCI ACWI while maintaining quality characteristics, although there can be no guarantee this will continue. Despite its lower valuation and higher income profile, the Index maintains strong quality characteristics, with a return on equity of 14.0%, compared with 15.4% for MSCI ACWI.

Figure 4: Comparison of fundamental valuations

Source: FactSet, WisdomTree as of 29 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Conclusion

The WisdomTree Global High Dividend UCITS ETF offers investors a differentiated path to access global dividend yielding companies. Built on a transparent, rules-based methodology that targets yield sustainability and quality, the ETF delivers a dividend yield more than double that of the MSCI ACWI, without compromising on the balance sheet and earnings quality that defines WisdomTree's approach to dividend investing. In an environment defined by geopolitical risk, inflationary persistence, and elevated market volatility, the dividend equity proposition has rarely been more relevant. The WisdomTree Global High Dividend UCITS ETF is both a natural complement to existing regional dividend allocations and a standalone core income sleeve for sophisticated multi-asset portfolios.

Investments in equity securities can fall in value and investors may lose some or all of their investment. Companies paying high dividends may reduce, suspend or cancel dividend payments at any time. A high dividend yield may be the result of a falling share price and does not necessarily indicate financial strength. The Fund invests globally and may be exposed to market, currency, sector and regional risks. The Fund's investment strategy may underperform broader equity markets or other income-focused strategies. Past performance and simulated backtested performance are not reliable indicators of future results.

1 Source: Hartford Funds Data, at 29 May 2026.

Related Products