Value trumps growth in emerging markets

Commodity prices have had a strong run (up 32%)1 driven in part by the recent surge in energy prices. Commodity price surges can redefine the fortunes of major commodity exporters, most of which are present in Emerging Markets (EM). According to a paper drafted by the International Monetary Found (IMF)2 in 2016, most emerging markets had experienced a high period of growth during the commodity price boom. We have seen many emerging and developing economies prosperity rise and fall in tandem with global prices of their leading commodity exports. EM is a net commodity exporter to the tune of 2.6% of gross domestic product (GDP) while developed markets are a net commodity importer to the tune of 1.6% of GDP3. Russia is a case in point. Not only is Russia a major exporter of oil and natural gas (accounting for nearly 40% of Europe energy supply) but it is also an important exporter of nickel, palladium and aluminium. The ongoing energy crisis has taught us that there is still a considerable period until when global reliance on fossil fuels will be phased out and green energy is phased in. And so, Russia stands to benefit amidst this current energy crisis. Brazil is another key exporter of oil, iron ore, soybeans, and coffee from the Latin American region is poised to benefit from the surge in commodity prices. The energy transition will also drive consumption of the raw materials required to generate and consume energy in a cleaner way such as – aluminium, copper, nickel, cobalt and lithium. In addition to being a key copper producer, Chile remains an important source of wind and solar power and is expected to emerge as a low-cost producer and exporter of green hydrogen. China dominates global production of rare earth minerals (around 66%)3 which are required for the manufacture of new energy goods. Amidst the ongoing commodity price increase, a new trend is taking root evident from the outperformance of value versus growth stocks within the EM landscape over the past year.

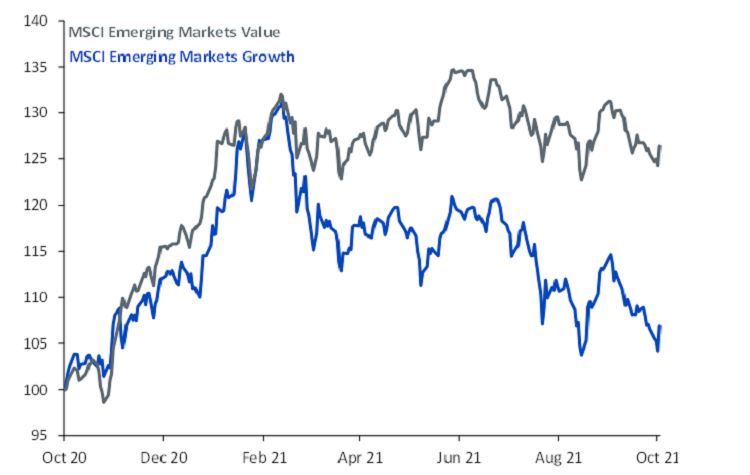

Figure 1 – Outperformance of value versus growth in EM

Source: Bloomberg, WisdomTree, data available as of close 08 October 2021.

You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Many would argue that the composition of EMs has changed dramatically over the decade and EMs are less reliant on commodities. However, in commodity exporting nations, the commodity intensive value sectors remain an important source of public sector revenues and state subsidies. Commodities account for 44% of EM trade compared to just 29% in DMs2. As prices of most of these commodities have risen, alongside improving terms of trade – it should lend a tailwind for these economies. EMs have faced a sharp setback owing to the regulatory onslaught in China alongside the Evergrande crisis rendering their valuations at a significant discount to developed markets. Keeping in mind where we are in the economic cycle, with inflation concerns rising and growth starting to plateau and monetary conditions starting to tighten, investors would benefit by taking exposure to dividend paying commodity exporting EM economies. The WisdomTree EM Equity Income Index’s offers a higher geographical tilt towards commodity exporters within EM such as Russia (12.41%) and Brazil (4.14%) and a lower tilt towards China (-15.3%) versus the MSCI Emerging Markets Index (benchmark). The benefit of these allocations towards commodity intensive regions is reflected in the WisdomTree EM Equity Income Index’s 14.8%4 outperformance versus the benchmark. Its emphasis on allocating towards the commodity intensive sectors such as materials and energy drove a large share of its outperformance versus the benchmark. In addition, the WisdomTree EM Equity Income Index’s allocation towards the highest dividend paying stocks also played an important role in its outperformance versus the benchmark evident from the attribution table below.

Figure 2: Dividend Yield Attribution

.png?sc_lang=en-gb&hash=59CB20DDC0EAE9424D771419EBB3D96C)

Source: Factset, WisdomTree from 30 September 2020 to 30 September 2021.

You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Sources

1 Price performance of Bloomberg Commodity Index from 31 December 2020 to 7 October 2021

2 IMF 2018 Annual Data

3 IMF Working Paper – Trading on their terms? Commodity Exporters in the Aftermath of the Commodity

4 Statista

5 Factset performance from 30 September 2020 to 30 September 2021

Related blogs

+ Kicking the implicit guarantee of State-Owned Enterprise

Related products

+ DEM/DEMD WisdomTree Emerging Markets Equity Income UCITS ETF