Late in the economic cycle? Look at Commodities!

From an equity market perspective, the first quarter of 2019 was a complete blockbuster . One has to go back to the third quarter of 2010 to see stronger performance for the MSCI World Index, which delivered a return of 12.5%. Now, the MSCI World Index doesn’t perform strongly without the US equity market performing strongly: one must go back to the third quarter of 2009 to see stronger quarterly performance on the S&P 500, which returned 13.5%.

One reaction to this is to think that equity markets will continue to run and that the rally will continue. However, we see more thinking that this is classic “late-cycle” behaviour and that it is only a matter of time until the US economy experiences its next recession.

It’s been a long time…

Since 1945, there have been 11 business cycles in the US, according to the National Bureau of Economic Research (NBER). The five longest expansions have been2:

- March 1991 to March 2001, 120 months.

- February 1961 to December 1969, 106 months.

- November 1982 to July 1990, 92 months.

- November 2001 to December 2007, 73 months.

- March 1975 to January 1980, 58 months

From June 2009 to April 2019, in the current period, we’ve seen an economic expansion of 118 months. In a couple of months, for all indications we can see today, we will have experienced the longest economic expansion since such things have been recorded.

Late cycle signals are flashing

On 22 March 2019, based on closing values the 3-month US Treasury bill had a yield that was higher than that of the 10-Year US Treasury Note3. This hasn’t happened since August of 2007, and it corresponds to the longer tenors of the US Treasury curve pricing in a future slowdown in economic growth after the US Federal Reserve has been raising interest rates.

This is something that has, historically, tended to precede economic recessions. Whether people prefer to focus on the 2-Year vs. 10-Year spread or other variants, few disagree with the perception that the US is late in the economic cycle and that a recession could occur over the course of the next few years.

US Federal Reserve has hiked rates 9 times since December 2015

The Federal Funds rate went from a range of 0-25 basis points to a range of 2.25% to 2.50% over the course of 18 December 2015 to 20 December 20194. Historically, the US Federal Reserve (Fed) regarding rates looks to control the risks of rising unemployment and rising inflation. The conclusion of a rate hiking cycle has tended to coincide with being late in economic cycles where the Fed is beginning to see potential weaknesses that couldn’t handle further hikes.

Figures 1a and 1b show that the behaviour of broad, diversified commodity prices has tended to deliver positively during periods where the Fed has been hiking rates. In our view, this has corresponded to the late cycle nature of stronger commodity price performance as monetary policy is responding to rising risks of inflation.

Fed policy has indicated a relationship to Commodity price behaviour

Figure 1a: Fed funds policy interest rate

Figure 2a: Annualised performance of S&P GSCI Index (Spot price) during different Fed interest rate cycles

Source for both figures: Bloomberg, 31 December 1970 to 28 February 2019. Includes backtested data. The S&P GSCI Index began live calculation 11 April 1991.

You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

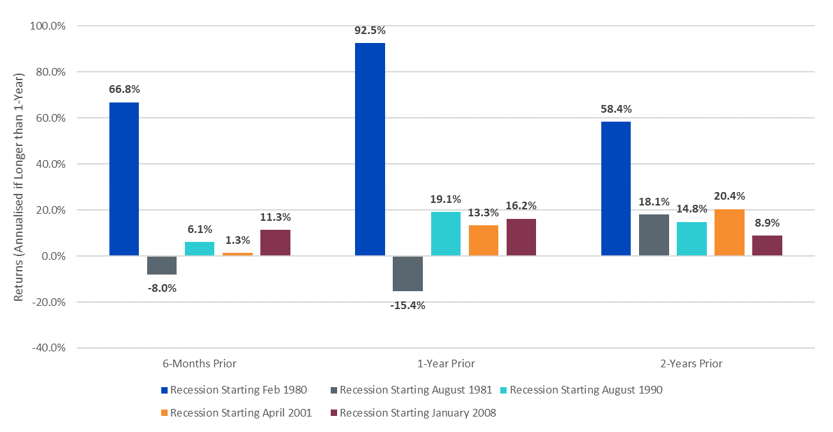

Leading into recessions: how have Commodities performed?

To further test the thesis, we can look at the last five known recessions. While we’d never know the precise starting date of a given recession beforehand, we can look at a period six months beforehand, 1 year beforehand and 2 years beforehand, as seen in Figures 2a and 2b.

- 2-Years prior: The S&P GSCI Index, on an annualised basis, delivered positive returns in each of the five previous 2-year periods preceding recessions. This seems to have been the most consistent behaviour we’ve noticed, and it was also true for the Bloomberg Commodity Index in Figure 2b.

- 1-Year prior: Both the S&P GSCI Index in Figure 2a and the Bloomberg Commodity Index in Figure 2b exhibited positive returns in the 1-Year periods prior to the last five recessions, except for the 1-Year period prior to the recession beginning in August 1981.

- 6-Months prior: This was the least consistent of the periods shown. The recession starting August 1981 did see both the S&P GSCI Index and the Bloomberg Commodity Index with a negative return over these six months. The S&P GSCI Index also exhibited a negative return in Figure 2a during the 6 months leading into the recession starting April 2001, whereas the Bloomberg Commodity Index in Figure 2b was positive by a small amount during this same period.

- Recession Starting February 1980: In both Figures 2a and 2b, one can see that the periods leading into this particular recession were very strong for both the S&P GSCI Index and the Bloomberg Commodity Index. We know that inflationary pressure was very, very high in this period and has not approached levels similar to this in the US at any time since.

Figure 2a: Commodity price behaviour prior to five most recent recessions, S&P GSCI Index

Sources: Bloomberg, National Bureau of Economic Research. Returns are calculated on the basis of total return and do include the impact of rolling between different futures contracts. Includes backtested data. The S&P GSCI Index began live calculation 11 April 1991. Recession Starting Feb 1980 refers to a period from 31 January 1978 to 31 January 1980. Recession Starting August 1981 refers to a period from 31 July 1979 to 31 July 1981. Recession Starting August 1990 refers to 31 July 1988 to 31 July 1990. Recession Starting April 2001 refers to a period from 31 March 1999 to 31 March 2001. Recession Starting January 2008 refers to a period from 31 December 2005 to 31 December 2007.

You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Figure 2b: Commodity price behaviour prior to five most recent recessions, Bloomberg Commodity Index

Sources: Bloomberg, National Bureau of Economic Research. Returns are calculated on a total return basis and do include the impact of rolling between contracts. Includes backtested data. The Bloomberg Commodity Index began live calculation 11 April 1991. Recession Starting Feb 1980 refers to a period from 31 January 1978 to 31 January 1980. Recession Starting August 1981 refers to a period from 31 July 1979 to 31 July 1981. Recession Starting August 1990 refers to 31 July 1988 to 31 July 1990. Recession Starting April 2001 refers to a period from 31 March 1999 to 31 March 2001. Recession Starting January 2008 refers to a period from 31 December 2005 to 31 December 2007.

You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Time to consider Broad Commodities?

It’s no secret—commodities do not tend to perform with positive price performance in all periods with equal magnitude. While there can never be any guarantees, we believe the current environment has more of the signals of a period where commodities may represent an important, additive allocation to a given portfolio. It’s interesting that the period in Figures 2a and 2b from 30 September 2007 to 30 November 2015 where the S&P GSCI Index delivered negative average annual returns has soured so many investors on this asset class, leaving them to think first of other asset classes that have done better, like equities. Moments like these with imminent policy transitions late in the economic cycle suggest fresh consideration for broad commodities.

Source

1 Bloomberg, with data measured over the period 31 December 2018 to 31 March 2019.

2 US Recession Data: National Bureau of Economic Research US Business Cycle Expansions and Contractions. Nber.org/cycles.html.

3 Bloomberg.

4 Bloomberg.

Related blogs

+ Broad commodities: Does an optimised strategy still make sense?

+ Will you miss the commodity comeback?

Related products