Will you miss the commodity comeback?

Do commodities have a place in a portfolio?

This is an interesting question in today’s environment. Those of us who have read various finance text books including sections on the benefits of things like “asset allocation” and “diversification” would, almost without thinking, say “yes.”

But if we look at the reality of what market participants have experienced in the past five years, we then recognize that, behaviourally, what has been practiced may look quite different.

US Equities delivered very strong returns, while broad commodities ran into the wind

Sources: WisdomTree, Bloomberg. US Equities: S&P 500 Index. US Fixed Income: Bloomberg Barclays US Aggregate Index.

Broad Commodities: Thomson Reuters Continuous Commodity Index.

You cannot invest directly within an Index. Period from Dec. 31, 2012 to Feb. 15, 2018.

- With some small exceptions in mid to late 2015 and early 2016, US equities have moved inexorably upwards, exhibiting, at least until February of 2018, historically low volatility. 15.90% average annual returns for about 5 years is a strong result.

- For the better part of this 5-year period, interest rates have remained at or near historic lows, accounting for the low returns in US Fixed Income, but notably, this asset class was also positive and would have dampened equity volatility within a broader portfolio.

- Broad commodities, on the other hand, lost almost a third of their value on a cumulative basis, or equivalently -6.5% per year.

What those who have had exposure to commodities have seen in the past five years has been a money-losing proposition, in the face of stellar returns in their US equity portfolios.

Shifting drivers of commodity strategy returns

Taking a step back, it is first important to understand what factors have been responsible for such horrible returns in commodities, as the fact of the matter is that either these drivers remain powerful headwinds (and returns suffer) or they are poised to shift (leading to better returns to come).

1. Collateral: In commodity strategies that utilize futures contracts to generate their commodity exposure, one component of their returns comes from the exposure of the collateral for those contracts, typically short-term treasuries. The US Federal Reserve has embarked on a path of raising its policy rate, thereby raising collateral returns for commodity strategies from near-zero levels.

2. Spot: These are the prices of the actual commodities that are reported on a daily basis—and in many cases, this is the component of returns that commodity investors may think that they are going to receive. Since commodities tend to be priced in US dollars and the US dollar has been trending more towards weakness than towards strength, an important headwind may be shifting, allowing spot prices to rise.

3. Roll: When futures contracts are used to generate exposure to commodities, at certain times the strategy must shift from one expiring contract into a new contract—not a cost-free exercise. If the prices of commodities in futures markets are higher and rising relative to current spot prices, the impact of this “roll yield” will be negative (contango); conversely, if the prices of commodities in futures markets are lower and falling relative to current spot prices, then the impact of this component of return will be positive (backwardation).

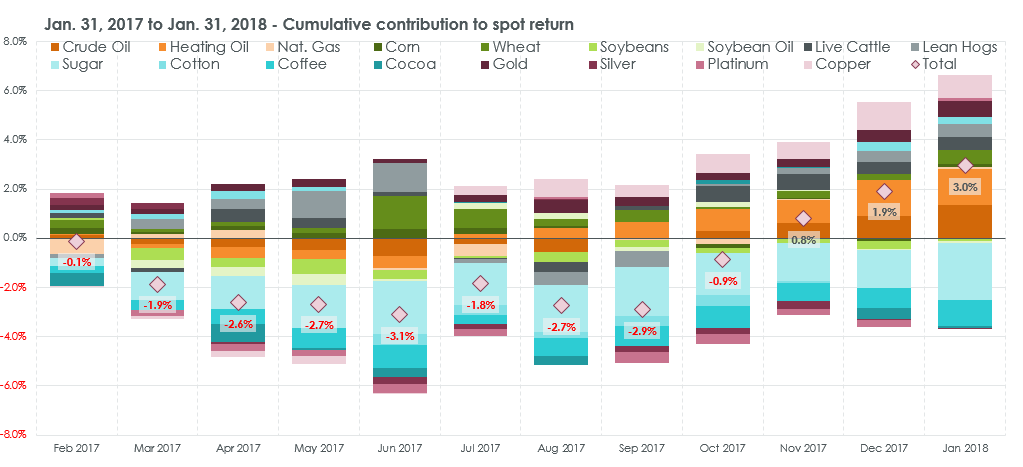

Over last year: Spot prices have begun to rise

Sources: WisdomTree, Bloomberg. Commodities selected from the Thomson Reuters Continuous Commodity Index universe.

- One of the most important trends—signified by the larger and larger positive proportion of the grey colours—has been the rising of energy commodity spot prices. In fact, on a spot basis it has only been the softs that have struggled over this period.

Fairly recently roll yields have stabilized

Sources: WisdomTree, Bloomberg. Commodities selected from the Thomson Reuters Continuous Commodity Index universe.

- While roll yields were still negative over the past year, we have begun to see stabilization, particularly in the green (grains) and grey (energy), that contribute the most to the roll yield. If roll yields in energy and grains are truly becoming less negative, this will be an important factor to monitor for broad commodity investors.

While a “less negative” roll yield might not seem all that exciting, if we place it in context where we would estimate that the cumulative impact on the return of the Thomson Reuters Continuous Commodity Index was more than -50% cumulatively over the past 10 years1, a less negative picture could look more like an important development.

Connecting commodity price behaviour to other macroeconomic factors

Now, many people may be asking what other variables they can watch in order to indicate how commodities may perform. It is natural to look at how markets are pricing inflation expectations, and one measure there is the 5-Year Forward Breakeven Inflation Rate that the US Federal Reserve often uses.

Thomson Reuters Continuous Commodity Index indicated a close relationship with expected inflation

Sources: WisdomTree, Bloomberg, with data from August 31, 1999 to Jan. 31, 2018.

You cannot invest directly within an Index.

Inception date for Continuous Commodity Index: Aug. 20, 1999.

We know that the US Federal Reserve has embarked on a path of raising interest rates and normalizing the size of its balance sheet. Inflation expectations of late have in fact ticked up. Historically, commodities have been an interesting “inflation hedge” type of investment. We know worrying about inflation has not been fashionable for the last five years—and there really hasn’t been significant inflation to speak of. Going forward, we think it is important to consider that inflation may not be non-existent forever and that certain pieces of an asset allocation which may have lain dormant may yet again be awakening.

You may also be interested in reading…

+ Shale and Sheikhs’ oil war drives the Brent/WTI spread wider

+ Five reasons why you might use an enhanced commodity strategy

1 Sources: WisdomTree, Bloomberg, with data measured from 1/31/2008 to 1/31/2018.