When using Short Exchange Traded Products (ETPs), consider volatility and its drivers

Using short ETPs are effective hedging instruments, but it is crucial to consider the volatility of the ETP and the (hedged) investment period.

Generally, the higher (lower) the leverage factor, the less (more) capital efficient you are. If the hedged investment period is longer than 1 day, rebalancing the hedged exposure will be necessary to keep the long position protected. This is because of the relative large impact daily compounding can have on the returns of short ETPs when the holding period is longer than one day. Again, generally, the longer the holding period, the more likely it is that the cumulative return of short ETPs will deviate from the expected return (the cumulative return of the underlying index multiplied by the leverage factor). The deviation of actual from expected returns of a short ETP is subject to its volatility, effectively driven by:

1) The type of market condition/sentiment: is the market volatile, or stable and trending?

2) The asset class it tracks: is the underlying fixed income, equity, commodity, etc.?

3) The leverage factor: is the exposure 2x, 3x, 4x, 5x, or more (or less) leveraged to the underlying?

Market conditions

A volatile market condition, where an asset price zig-zags up and down and lacks direction will tend to see short ETPs producing cumulative returns that decay more rapidly over time than that of the underlying benchmarks. In directional down (up) trends, leveraged short ETPs will tend to produce cumulative returns that amplify more rapidly over time than that of the underlying benchmarks.

For example, the financial crisis clearly saw high-rated government debt as susceptible to the systemic risks in the banking sector and caused greater price movements than in the aftermath of policy rate cuts and QE which restored market confidence. These events reduced the perceived downside risks to bonds and lowered the volatility as a result. Hence, investors need to be first and foremost mindful of the type of market condition they find themselves invested in when assessing volatility and its effect on daily compounded returns of short ETPs.

The asset class

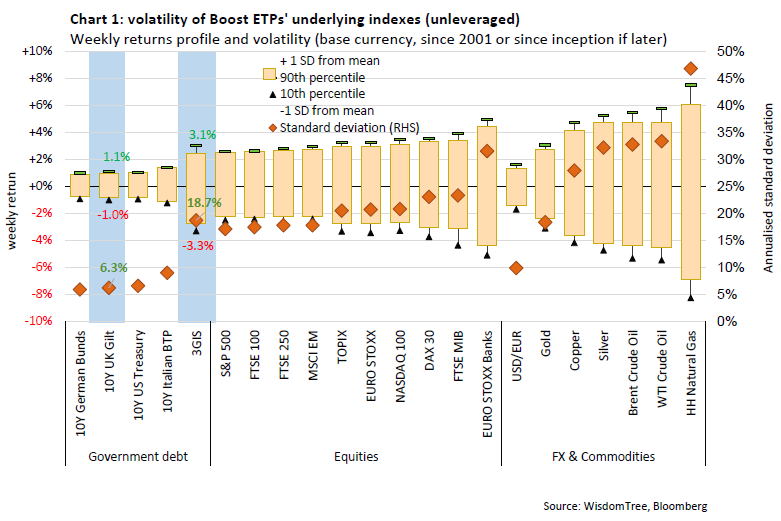

The volatility of the asset class itself is another important factor which impacts the daily compounding of short ETPs. Seen as safe haven assets, high-rated government debt is subject to much lower volatility than riskier asset classes such as equities or commodities. This is shown in Chart 1, which depicts volatility in two ways: first as single measure of standard deviation (annualised) of historic weekly returns (orange diamonds) and second, as a dispersion of historic weekly returns (the top and bottom deciles and one standard deviation above and below the average).

This chart shows that across underlying benchmarks of our range of Boost ETPs, UK Gilts are amongst the least volatile. For example, the orange diamonds in Chart 1 show 10Y UK Gilts as having a standard deviation (annualised) of 6.3%, about 3x lower than that of major equity markets and about 5x lower than most single commodities. Because the measure in itself is hard to conceptualise, a more intuitive way of describing the volatility is this: 10Y UK Gilts’ standard deviation of 6.3% is equivalent to a 1 in 5 probability for investors to gain or lose at least 1% on a weekly basis.

The leverage factor

The gains/losses become more pronounced when the leverage factor is introduced. Over a relative short holding period of one week, investors holding a 3x Short ETP on 10Y UK Gilts – such as 3GIS [1] --

would most likely be exposed to risks where, against similar odds of the underlying benchmark (ie the 10Y UK Gilt), the up and downside price movement is about 3x greater. In Chart 1, the light-blue highlighted areas compare the volatility between 10Y UK Gilts and the 3x short ETP tracking it. Putting this into context of the volatility of other (unleveraged) asset classes, the volatility of 3x short ETPs tracking 10Y UK Gilts would be similar to that of major (unleveraged) European equity markets, such as the FTSE 100 and EURO STOXX 50.

This shows that the effect of daily compounding on short ETPs tracking high rated government debt to be markedly less than on short ETPs tracking equity or single-commodity benchmarks. Investors need to be mindful that, in the first instance, it is the volatility of the benchmark index the short ETP is tracking that is driving volatility. A leverage factor greater than 1 built into the short ETP is then inherently the additional factor that increases volatility.

Once fully understood, investors may consider using leveraged short ETPs as a means to construct hedges around asset classes.

Sources

[1] 3GIS is the ticker of Boost 10Y Gilt 3x Short Daily ETP