Understanding Commodities

This blog is instalment 4 of our new educational blog series on investment strategies and asset classes. Today we address the potential of commodities for diversification of investments, particularly when accessed through exchange traded products.

Commodities provide diversification potential for investors, as they are typically not as highly correlated to the movements of stocks or bonds. But traditionally, commodities have been harder to access—especially for individual investors.

Figure 1: Some commonly referenced commodity groups

Source: WisdomTree

Click to enlarge

Today, commodity investing is typically achieved through two primary means:

- Using physically-backed investment strategies to gain access to commodity price movements.

- Using derivatives that are designed to help investors gain sensitivity to underlying commodity price movements.

Some commodities are easier to store than others—like metals. Metals don’t “go bad” and, since they are dense, more of them can be held in a smaller amount of space. Many agricultural commodities, on the other hand, would be much more difficult to store.

Today, there is a wide array of different exchange traded products (ETPs) that are designed to help investors access the price movements and returns of commodity markets. ETPs that provide exposure to commodities are sometimes called exchange traded commodities (ETCs).

Why access commodities through an ETP?

Generally, it is very difficult to get exposure to the (spot) price of a commodity without actually owning the physical commodity. Some ETPs are physically-backed and do represent holdings of an underlying commodity. Depending on the goal of the investor, as well as which specific commodities are desired, this approach may make sense.

Other ETPs are designed to gain exposure to commodities through derivatives. Futures contracts are a popular tool used in these ETPs.

For investors just starting to look at commodity investments, one of the most important considerations is whether a physically-backed or a derivative, futures-based strategy would be most appropriate. Neither is “better” or “worse”, but there are important differences to be aware of for each of these avenues

What is roll yield?

A futures contract is an agreement to buy something, in this case a commodity, at a future date at a set price. The agreement could be that you would buy it in a month, 6 months, a year or longer. Since most investors do not actually want to take physical delivery of the underlying asset, they tend to roll their investment into new contracts before the expiration date (also called expiry date, delivery date, futures expiry, expiry, etc.). One challenge is that the price you are agreeing to pay for the underlying asset may be above or below the current spot price (the price you would pay to buy it and take delivery right now).

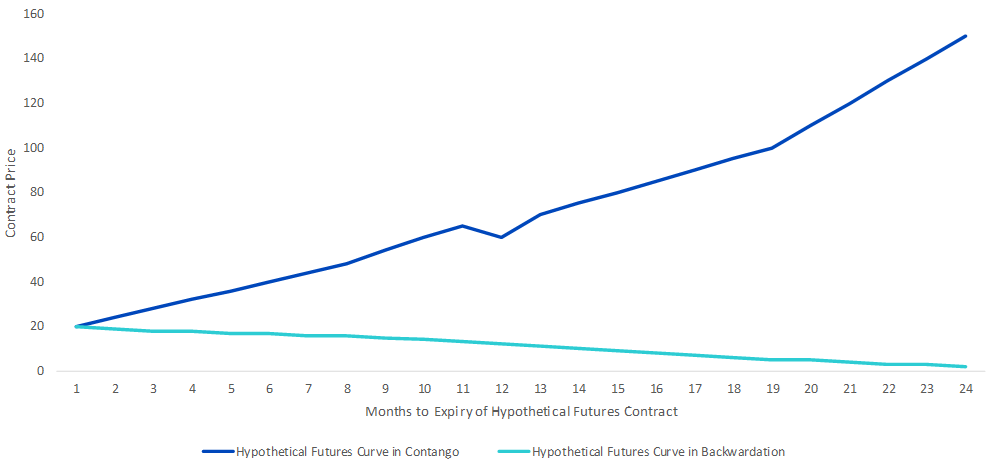

The Futures Curve

The collection of contract prices for available futures contracts of different expiries is called the futures curve or the futures term structure (see Figure 1). As you roll the assets, the prices of contracts with farther expiries may be higher or lower than the current spot price. These differences in contract prices can sometimes benefit investors and provide a profit or roll yield—or they can hurt investors and create a negative roll yield or loss.

In Contango

A commodity is said to be in contango when the price of a distant futures contract is higher than the near futures contract. Contango markets can act as a drag on a futures market investment. Take the example of an investor entering a front-month contract in a contango market. As time passes and the front-month futures contract comes close to expiry, for the investor to continue their exposure they would need to enter a new futures contract at a higher price, incurring a loss. The roll return in contango therefore may have a negative price impact on the futures return.

In Backwardation

A commodity is said to be in backwardation when the price of a distant futures contract is lower than the price of a nearer future. Backwardation markets can enhance the return on a futures market investment. Take the example of an investor entering a front-month contract in a backwardation market. As time passes and the front-month futures contract comes close to expiry, for the investor to continue their exposure, they would need to enter a new futures contract at a lower price, incurring a profit. The roll return in backwardation therefore may have a positive price impact on the futures return.

Figure 2: Futures curve in contango vs backwardation

Source: WisdomTree

Click to enlarge

Further in the series we will discuss potential ways to manage the risks—and capitalise on the potential opportunities—involved with investing in commodity futures.

Related blogs

+ The factors that drive performance