A year to focus on currency risk: What can UK investors do?

This past year, Brexit and Sterling depreciation has dominated the headlines and we expect currency volatility will remain a feature of markets in 2017 due to the significant number of macroeconomic forces at play.

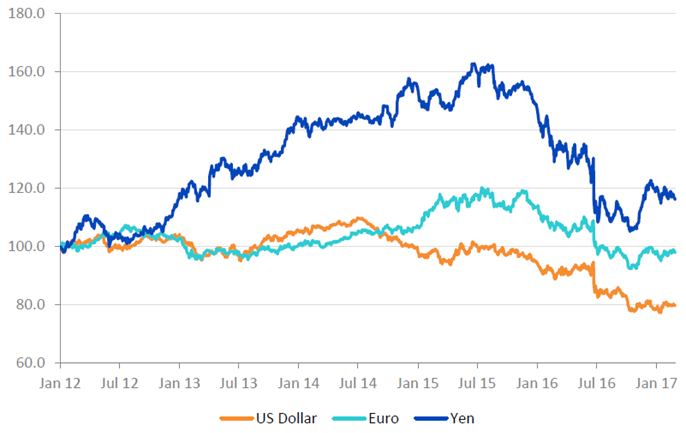

As US equities comprise over 60% of a standard MSCI World Developed Markets benchmark, for many, it’s been happy days as Sterling reached fresh lows against USD in the aftermath of Brexit. Sterling also fell against the Euro – last year through November, the Sterling-Euro exchange fell by 22.5%. But, since that point in November, Sterling rallied by almost 6%.

First Brexit. Now what?

With Article 50 due to be triggered this month and the added uncertainty around key European elections, 2017 is a big year for foreign exchange rates and risk. In a span of just two years, the realised 60 day volatility of Sterling against the US Dollar went from 3.73% (August 2014) to 23% (August 2016).

Realised volatility has since bounced back to 11.5%1 and in the short term, Sterling risk remains evenly poised relative to the US Dollar. But, with the Euro’s viability being undermined by concerns from various political angles, it is entirely possible that Sterling could strengthen versus the Euro.

Figure 1: Sterling relative to US Dollar, Euro and Yen

Source: Bank of England

Against this backdrop, an investor should consider two themes:

- The potential that the Sterling could strengthen:

Having a hedged exposure to US equities will be important to preserve the equivalent of local equity returns. But investors also have an option to use an unhedged share class, so they can switch according to their currency view.

With the weak Euro, Eurozone export oriented companies are also attractive as they typically benefit from such currency moves, and are dominated by large multinationals deriving their revenues outside the Eurozone.

We offer European equity strategies in both GBP-hedged and unhedged versions providing investors with different choices from a portfolio perspective.

- A weakening Yen leading to a stronger Japan:

Optimistic growth expectations for Japan’s economy has been riding high over the last several months, thanks Yen depreciation. Expected are substantial structural reforms, a continued government bond-buying programme and a rebound in corporate earnings –

all contributing to stimulated domestic demand and increased economic activity.

Against this backdrop of a decline in the Yen – even in the face of Sterling’s weakness – unhedged investors in Japanese investors saw their returns impacted. Therefore, we believe that an export tilted basket of dividend paying equities combined with a currency hedge is appropriate.

UK investors can use WisdomTree’s GBP-hedged and unhedged share classes allowing for a flexible approach to managing currency risk.