What's Hot: Supply concerns stoke palladium higher

Key Takeaways

- The combination of announcements from Russia alongside Sibanye Stillwater’s restricting plans have resulted in a notable turnaround in sentiment towards palladium.

- The palladium market is expected to remain in a deficit in 2024.

- If the gasoline car production were to stabilise at the 2023 levels, it has the potential to further increase palladium’s demand estimate thereby widening the deficit.

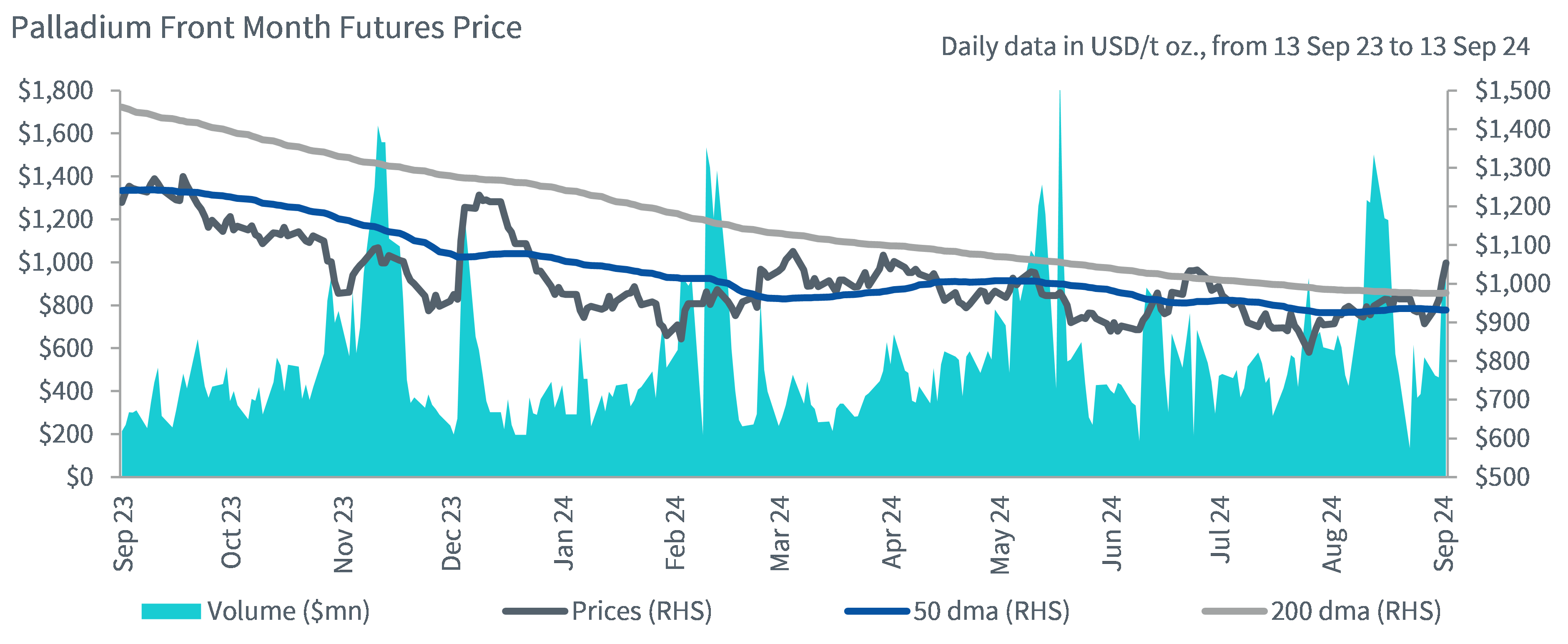

Palladium has hit its highest level this year, surpassing above the US$1,100 per troy ounce mark. There has been a confluence of factors behind the recent turnaround in sentiment and price momentum. Palladium has been under pressure over the past year owing to falling demand for catalysts used in traditional Internal Combustion Engine (ICE) cars.

Figure 1: Palladium front month futures price and volume over the past year

Source: Bloomberg, WisdomTree as of 10 September 2024. Historical performance is not an indication of future performance, and any investments may go down in value.

Russia considering export restrictions on metals

One of the key catalysts behind palladium’s stellar performance was Russian President Putin’s comments1 about possible export restrictions on certain metals in retaliation to Western sanctions. While palladium was not explicitly mentioned as part of the list of metals, nickel was. Since palladium is a by-product of nickel, palladium would be indirectly affected if Russia were to reduce its nickel production. With more than 40% of global mine supply, Russia is the most important palladium producer, followed by South Africa. This is why a reduction in Russian supply would quickly result in a shortage in the palladium market.

Sibanye-Stillwater restructures operations

The second factor behind palladium’s price rise came on the back of Sibanye Stillwater’s plans to reduce production by about 200,000 ounces by 2025 from its US operations, which accounts for 7-8% of global palladium supply. This reduction is significant in a market that has already been facing a supply deficit. Sibanye’s restructuring efforts to make its palladium operations more profitable, coupled with cost cutting and mine closures add to risks of lower supply. Historically palladium prices have been sensitive to supply disruptions, and this could potentially serve as an important catalyst especially when we are facing supply challenges from Russia.

Demand outlook hinges on the auto sector

The demand outlook for the palladium market hinges on vehicle output. Palladium demand from the auto sector, which accounts for nearly 80% of total demand has undergone structural changes – (1) shift to electric vehicles (2) substitution with platinum in catalytic converters (3) falling demand for ICE. There is no denying the auto sector has faced considerable challenges – including a slowdown in new orders, rising inventories of completed vehicles and a risk of component shortages owing to Red Sea supply disruption. The gasoline car sector has held up quite well. In North America, a recovery in ICE production supported automotive palladium demand last year, at 1.9Moz2. Imports in the US have remained steady so far this year. Given the recently announced delays to electrification programmes at several large automakers, it is possible that ICE vehicle output (that palladium relies on) could hold up better than expected in 2024.

Palladium market remains in a deficit in 2024

The palladium market is expected to remain in a deficit in 2024 although the deficit is expected to shrink significantly to around 360,000oz in 20243. Palladium demand is expected to decline by 6%, yet industrial consumption is expected to hold up well, supported by some modest gains in the electronics and pollution control sectors. If the gasoline car production were to stabilise at the 2023 levels, it has the potential to further increase palladium’s demand estimate thereby widening the deficit.

Sentiment improves on the palladium market

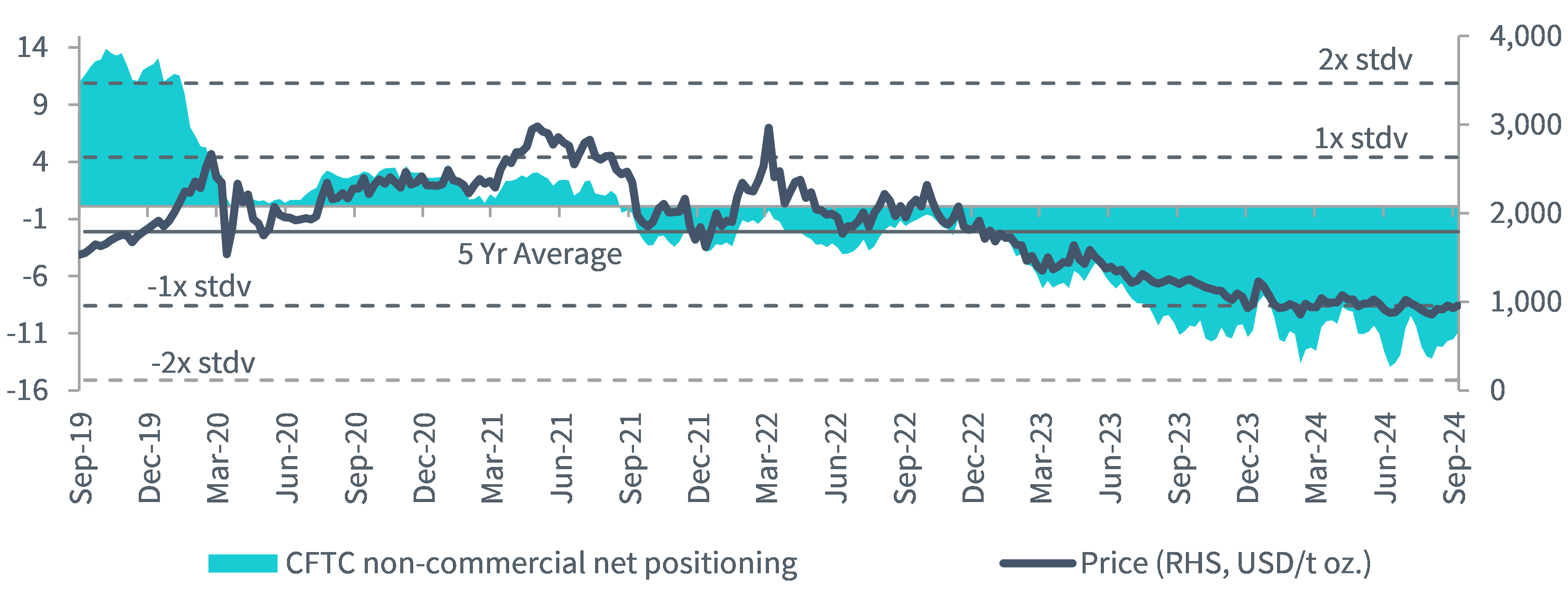

Despite fundamental supply deficits in the palladium market, sentiment has remained weak since Q3 2022, evident from the chart below. Yet over the past week, the confluence of announcements from Russia alongside Sibanye Stillwater’s restricting plans have resulted in a notable turnaround in sentiment. Net speculative positioning in palladium has increased 10.5% over the prior month as investors scrambled to cover their short positions, further driving up prices.

Figure 2: Palladium – Net speculative positioning versus price over the past 5 years

Source: Commodity Futures Trading Commission, Bloomberg, WisdomTree as of 10 September 2024. Historical performance is not an indication of future performance, and any investments may go down in value.

1 Reuters as of 12 September 2024

2 US International Trade Commission as of 31 December 2023

3 Johnson Matthey