European macro outlook: Political risk at the gates - If 2017 is no threat to equities, it is for the Euro and peripheral bonds

Given the near term economic outlook is solidifying in the US, stabilising in the emerging markets and moderating in Europe, we believe that European equity markets should prove resilient to the looming European political uncertainty in 2017 that could redefine the European economic and financial landscape for decades. For now, the banks’ efforts to fast-track restructuring and recapitalisation ahead of potential political fallout in 2017 are driving increased European equities strength. This is removing concerns over systemic risks lurking within some of the largest lenders which, combined with the deep discount at which banks stocks trade generally, present investors an entry point to position opportunistically around the European equity market.

We expect that European equity strategies with broad exposures tilted to large and midcaps will perform strongly off the back of positive financial sector sentiment. Furthermore, strategies with currency-hedge overlays and/or an emphasis on exporting companies will help investors counteract risk against a downbeat Euro sentiment.

Our outlook for European fixed income is equally downbeat. Underpinned by Trump’s US presidential election win, bullish conviction has waned across high and low grade issuers of government debt. Other macro events adding to bearishness in fixed income include “Brexit”, the ECB’s tapering of debt purchases and Italy’s “no” referendum on constitutional reform. All inadvertently raised the cost of borrowing, undermining any momentum in domestic demand-led growth in 2017 and potentially delaying a meaningful recovery in jobs and wages in France and Italy – Europe’s weakest core countries.

The greatest European 2017 macro risks will be the absence of deficit spending and a Trump-equivalent agenda to boost investments. Eurosceptic movements will see it as an opportune year to redefine the political agenda for Europe in a big way if – after the general elections in the Netherlands (March), France (May), Germany (September) and in Italy (date currently unknown) – the newly elected governments sway decisively against the rigid fiscal rules and bank rescue regimes imposed on by the EU. The EU’s weakest link is Italy, where a caretaker government looks vulnerable against surging support for Eurosceptic parties on both the left (The Five Star Movement) and the right (The Northern League).

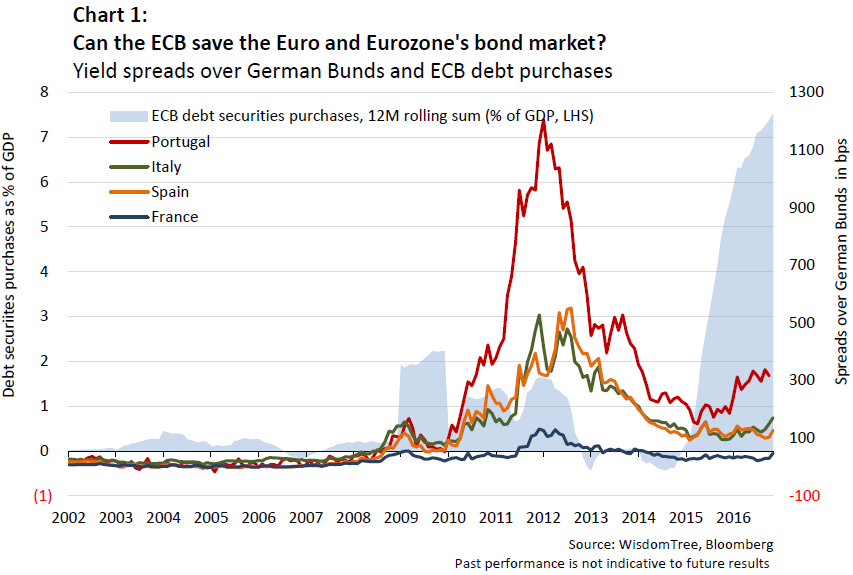

Underpinned by these macro events, Chart 1 shows how Europe’s weakest sovereigns have become subject to increased selling pressure, with spreads over German Bunds widening even as the ECB’s intervention in bond markets rose to the tune of 7.5% of Eurozone GDP on an annualised basis.

Bare minimum monetary support undermines confidence in bonds and the Euro

The ECB’s decision to prolong and at the same time also cut debt purchases suggests a bare minimum approach to monetary support for the Eurozone whose path to recovery is far from self-sustaining. The timing of the tapering in particular is poor, if not outright risky, given the looming general elections in Europe this year and the Fed’s hawkish stance on US monetary policy.

While we believe the extension of ECB’s QE programme should serve as a shock-absorber over a period where investors are bracing themselves for renewed political uncertainty (with Eurosceptic parties gaining in the polls ahead of the Netherlands, France, Germany and Italy general elections), the cutback of monthly purchases to EUR 60 billion (from EUR 80 billion) starting March to at least December 2017, means ‘tapering’ will occur precisely at the onset of a tightening monetary conditions in the US.

Trying to prevent bond yields in Europe from rising at the same time that US Treasury rising bond yields pressures are mounting may prove ultimately difficult with EUR 20 billion per month reduction in high-grade debt purchases. Yield hungry European investors will look at the sizable yield premium offered in US Treasuries and the upside potential of the Dollar, questioning the value of holding German Bunds or Italian BTPs. There is the risk that the widening US and European interest rate gap will force the ECB to revert back to increasing QE to contain the selling pressure in European government bonds. By risking its credibility as an effective intervener in bond markets, the ECB has made itself prone to enticing speculators back into the fore to bet against Eurozone’s weakest sovereigns and the Euro this year.

Restraint fiscal easing raises the stakes for political unity in Europe

The rise of Euroscepticism across the continent presents the biggest risk for Europe’s financial markets. Putting the Euro to a referendum, such as is demanded by The Five Star Movement in Italy or Front National in France depends on these anti-Euro parties winning the general elections. It need not get that far if Europe’s mainstream parties on the left and right harden their stance against fiscal tightening and immigration in an effort to blunt the message of extremist fringe parties. But time is running out. Mainstream parties have only half-heartedly adopted popular rhetoric and Eurozone finance ministers have been reluctant to resist fiscal restraint and bail-in rules. We believe it could be too little too late to sway public support and preserve political unity.

At the EU level, officials have been reluctant to unleash an aggressive fiscal stimulus package, or a ‘Trump-equivalent’ investment infrastructure plan to boost jobs and restore confidence. The language of the European Commission suggests an uncompromising focus on budgetary restraint. In its latest assessment of the 2017 draft budgets submitted by Eurozone members, it identified eight members (Italy, Spain, Portugal, Belgium, Finland, Slovenia, Lithuania and Cyprus) as in danger of being non-compliant with fiscal rules for next year, to which the Eurogroup – an informal group of finance ministers of Eurozone members – have broadly concurred.

Eurozone’s Achilles’ heel

The threat overhanging the Eurozone is now Italy and its large public debt. In spite of Italy’s tough austerity measures and the government saving close to 2% of GDP per annum over the last three years, the debt repayment burden (in the form of interest and principle) of more than 4% of GDP over the same period has simply overwhelmed the country in its attempt to bring down debt. To put this aggressive belt-tightening into context, the primary budgets as percentage of GDP in 2015 showed Italy (+1.5%), along with Germany (2.3%) and Austria (1.3%) to be the top savers at the state level amongst Eurozone’s main economies (see chart 2). The realisation has not hit the EU that for Italy to bring down debt it must outgrow it. This now seems elusive, having voted no to constitutional reform – which would have reinvigorated Italy’s economic recovery through reform bills being ratified faster in much needed areas such as the budget, infrastructure spending, the tax code, the pensions system, and – crucially – the labour market. With significant deficit spending off the table – after it being granted more budgetary leeway following last year’s earthquakes which, on top of the refugee crisis, have burdened state finances – there appears to be no lever for the country to revive growth. Stuck at over EUR 2.2 trillion, or 133% of GDP, Italy’s government debt load will remain the Eurozone’s Achilles’ heel.

Banks: rising rates and market-based resolutions boost the outlook for profits and a re-rating

Trump has reawakened the risk-on asset allocation shift in Europe, driving bond yields out of sub-zero territory. The ramifications of rising US rates to European bank stocks are potentially bullish, as conditions for net lending margins in loan books improve and fears of deposit holders fleeing savings account for fear of extra charges recede. Furthermore, steepening yield curves and widening spreads in Europe have reinvigorated profit opportunities for the trading book.

Signs have emerged in Italy of a heightened sense of urgency to deal with bank restructuring before the caretaker government under Renzi dissolves for new elections this year. Unicredit has opened up an opportunity to warm investors for a EUR 13 billion capital raising to bolster its capital buffers, and in so doing alleviate concerns of systemic risk posed by Italy’s largest bank. Underpinned by the deeply discounted valuations with which Italian banks trade, the large upside potential we believe will compel investors to react positively to the market-based solutions sought by Italy’s banks. We expect more restructuring, recapitalisations and consolidation through M&A in Eurozone’s banking sector.

Sterling and gilts at risk if formal breakaway from the EU is delayed

Bond market bearishness in the UK has been underscored by concerns over import-driven inflation fears following the Sterling’s plunge as a result of Brexit. The Sterling’s marked devaluation comes at the backdrop of debt-fuelled household spending who, faced with potentially much higher energy bills and transportation costs, could see their propensity to spend diminished this year. In that case the feedback loop is negative, with slowing growth for the economy translating into weakening tax take for the Treasury at a time when it is preparing to unleash more deficit spending. So far, it’s too early to see if Brexit has inflicted any damage to trade, investment and growth and going by the latest releases, the economy appears on a firm growth trajectory and sentiment is upbeat. The constant back and forth discussions of parties in parliament over the when and how to leave the EU in an orderly fashion suggests the stakes are high enough to expect the triggering of Article 50 – agreed to be on March 2017.

Conclusion

The marked devaluation of the Euro and the reset of bond yields of peripheral government debt reflect large 2017 European political and economic risks. As the EU shows no sign of urgency to reinvigorate fiscal stimulus and investments to get momentum back in domestic demand-led growth, the ECB appears to underestimate the threat this poses to the political union of Europe. We anticipate investors to discriminate government debt in Europe more vigorously on waning monetary supportive conditions and deteriorating credit metrics, subjecting bond markets in Europe’s weaker periphery to increased volatility and widening credit spreads. It’s ironic that, against this back backdrop, European equities are supported by their overseas exposure and will likely present investors a safer haven alternative to government bonds. US investors seeking an effective exposure to Europe’s equity market on the risk of the Euro devaluing should consider positioning in exporter stocks with a currency hedged overlay.

Potential investment implications

Long-term strategic strategies

+ WisdomTree Europe Equity income UCITS ETF (EEI)

+ WisdomTree Eurozone Quality Dividend Growth UCITS ETF (EGRA)

+ WisdomTree Europe Equity UCITS ETF – USD Hedged (HEDJ)

+ WisdomTree Europe Equity UCITS ETF – USD Hedged Acc (HEDK)

+ WisdomTree Europe Equity UCITS ETF – GBP Hedged (HEDP)

+ WisdomTree Europe Equity UCITS ETF – CHF Hedged (HEDD)

Short-term tactical trading opportunities

+ Boost BTP 10Y 3x Short Daily ETP

+ Boost BTP 10Y 5x Short Daily ETP

+ Boost Bund 10Y 3x Short Daily ETP

+ Boost Bund 10Y 5x Short Daily ETP

+ Boost Gilts 10Y 3x Short Daily ETP

+ Boost US Treasuries 10Y 3x Leverage Daily ETP

+ Boost Emerging Markets 3x Leverage Daily ETP

+ Boost EURO STOXX Banks 3x Leverage Daily ETP

+ Boost FTSE MIB 3x Leverage Daily ETP

+ Boost EURO STOXX® 50 3x Leverage Daily ETP

+ Boost FTSE 250 2x Leverage Daily ETP

You might also be interested in reading…

The Euro is falling – here’s our view on how to benefit

Our thoughts on allocation for a President Trump world

Gilts, Bunds, Treasuries: How to hedge the downside

Source: WidomTree, Bloomberg and ECB