Was this Cloud grown organically?

The Software & Services industry can be divided into two factions: the cloud software providers vs. the traditional software providers.

Despite this divide, the industry stands more united than ever. There is widespread agreement that software deployment via cloud, otherwise referred to as providing Software-as-a-Service (SaaS), is the preferred business model.

Software companies and their shareholders particularly align in support of the SaaS subscription-based revenue model. While traditional software companies derive revenue from single, large, and upfront transactions, cloud SaaS companies employ a recurring revenue model with smaller and more frequent transactions. The SaaS model is preferred because it results in a more predictable, annuity-like revenue stream.

Traditional software company Citrix Systems (CTXS) recently announced a strategic transition to a subscription-based revenue model. Its CEO discussed a few commonly cited reasons for the shift to cloud[1]:

Transparency - “…the strength that we're seeing in subscription bookings serves to improve our predictability and certainly accelerate our growth in future periods.”

Faster Growth - “…the fastest-growing part of the business is pure SaaS.”

Client Demand - “There are secular changes going on in networking driven by the adoption of cloud more than anything else…we've seen…a more pronounced move to software versus hardware. And that's simply because customers are looking for more flexibility, more choices in a way that they deploy their capabilities.”

Traditional software companies are pursuing the cloud model both organically, like CTXS, and inorganically through mergers and acquisitions (M&A). Meanwhile, the intensifying competition within the Software & Services industry has driven consolidation among SaaS providers, as well as private take-outs.

As evidenced by M&A activity within the BVP Nasdaq Emerging Cloud Index (EMCLOUD), SaaS companies have been acquired by traditional software companies, cloud peers, and private equity firms at premium valuations.

Since EMCLOUD’s inception in October 2018, there have been 10 transactions announced at an average deal premium of ~40%. Notably, all but 2 of the transactions involved an EMCLOUD constituent as the M&A target.

Sources: WisdomTree, Bloomberg as of 5/12/2019.

The above figure summarizes announced merger and acquisition transactions involving constituents of the BVP Emerging Cloud Index (EMCLOUD) since inception on 2/10/2018 through 5/12/2019. EMCLOUD constituents are designated with highlighted borders.

You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Acquirers of SaaS businesses are paying a premium for both expected and realized growth.

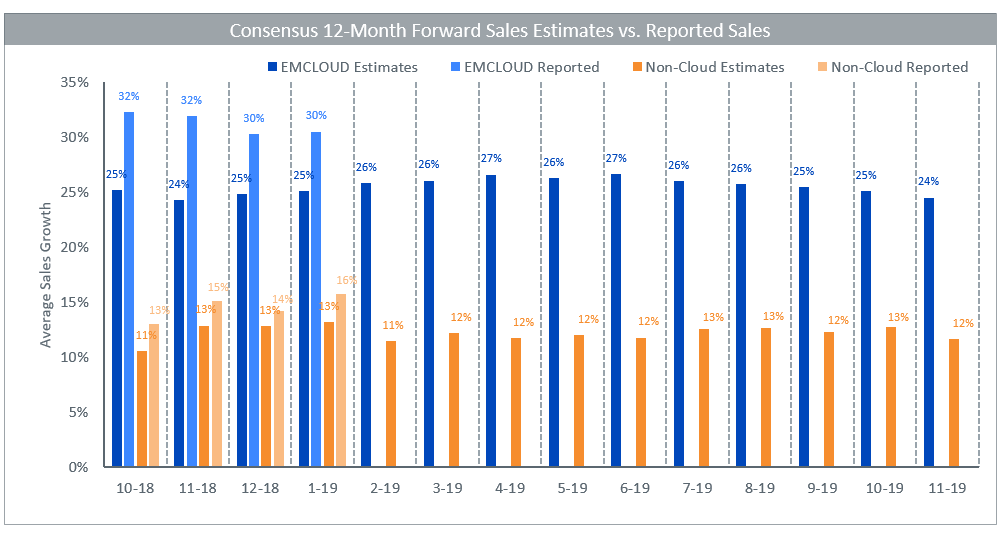

Consensus sales growth estimates for cloud SaaS companies are consistently double those of traditional non-cloud software companies; the average sales growth expectation for cloud has been ~25% as compared to ~12% for traditional software. More importantly, reported sales growth for cloud companies have exceeded consensus forecasts at a wider margin than non-cloud companies. The disruptive, organic growth and the compelling economics of the SaaS revenue model are key reasons behind why many cloud businesses have become acquisition targets.

Sources: WisdomTree, Bloomberg as of 30/11/2019.

Average sales growth estimates for the BVP Nasdaq Emerging Cloud Index and the non-cloud basket calculated as the average growth rate of forward-twelve-month consensus sales estimates relative to reported sales over the trailing-twelve-month across companies held in each basket at the indicated date. Reported sales growth calculated as the average year-over-year percentage change in reported trailing-twelve-month sales for the companies held in each basket at the indicated date. Please see disclosure at the bottom of this writing for the list of companies included in the non-cloud basket.

You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Source

[1] Source: WisdomTree, FactSet, Citrix Systems, Inc. Q2 2019 Earnings Call

Related blogs

+ Why we're bullish on Cloud Computing

+ The Cloud Computing megatrend for growth amidst uncertainty

Related products