How can AT1 CoCos sit within an investment portfolio?

Additional Tier 1 Contingent Convertible bonds (AT1 CoCos) have been an asset class in the limelight this year, with many investment houses gaining exposure for the first time. AT1 CoCo bonds which are predominately issued by European banks have benefitted from investor demand for higher yielding assets. In some cases, investors are looking to allocate to the European banking sector but find greater value in AT1 CoCos versus the respective banks common equities which have historically exhibited significantly greater annualised volatility than AT1 CoCos since 31 December 2013 (earliest common performance history) using the STOXX 600 banks index and the iBoxx Contingent Convertible Liquid Developed Europe AT1 Index (EUR hedged) as a reference.

AT1 CoCos are hybrid securities that combine features of both debt and equity securities as these instruments, if triggered, can be converted to equity or written-down. Coupon payments on some CoCos are entirely discretionary and can be cancelled. It is important for an investor to review all the features embedded in AT1 CoCos and become comfortable before investing. For investors who are comfortable with the risks inherent in this asset class, they provide the potential for a yield pick up over the banks more senior debt. Additionally, AT1 CoCos have seniority over common equity holders within the capital structure of the bank.

Why a diversified index is the best way to invest?

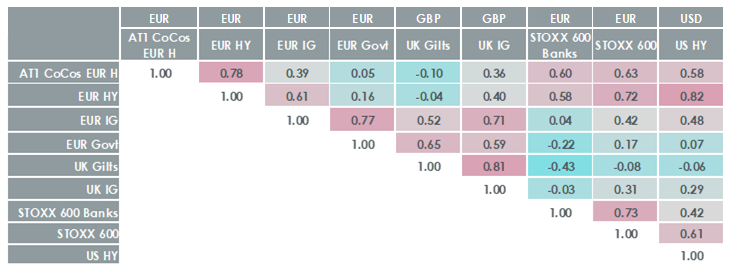

Each asset class has its unique features which should be reviewed and understood within the context of how it could be incorporated within a diversified portfolio of assets. AT1 CoCos are no different in that it offers investors the possibility to enhance the yield within their portfolio and diversify portfolio returns as the asset class exhibits low to negative correlations to many traditional fixed income asset classes as referenced in table 1.

Table 1: Monthly return correlations with other asset classes

Source: WisdomTree, Bloomberg. Period from 31 December 2013 to 31 March 2019. Based on monthly returns and includes backtested data. All Indices are in their base currency (specified in the table). All fixed income indices are total return, all equity indices are net total return. AT1 CoCos EUR H is the iBoxx Contingent Convertible Liquid Developed Europe AT1 Index (EUR hedged), EUR HY is the iBoxx EUR Liquid High Yield Index, EUR IG is the iBoxx EUR Liquid Corporates Large Cap Index, EUR Govt is the iBoxx Euro Sovereign Overall Index, UK Gilts is the FTSE Actuaries UK Conventional Gilts All Stocks Total Return Index, UK IG is the iBoxx GBP Liquid Corporates Large Cap TRI Index, STOXX 600 Banks is the STOXX Europe 600 Banks Index, STOXX 600 is the STOXX Europe 600 Index, US HY is the iBoxx USD Liquid High Yield Capped Index. You cannot invest directly in an index.

Historical performance is not an indication of future performance and any investments may go down in value.

As a high-level snapshot of the AT1 CoCo market, a large portion of issuers are Banks within Developed Europe with roughly 13%1 of the market accounted for by emerging market issuers. This is an important distinction as investors who are looking to buy AT1 CoCos but do not want the additional risks inherent in issuers from emerging markets (EM) should consider strategies that exclude EM exposure. Sometimes this can be easier to find within passive strategies that use pre-defined index restrictions in creating portfolios versus active managers which are inclined to take on more risks to aim to outperform the market. Additionally, a passive strategy that limits exposure to any individual issuer can also help mitigate the unsystematic risk of a specific issuer through issuer diversification benefits. This can usually be found in an exchange traded fund that invests in a diversified pool of AT1 CoCos issued by a large basket of issuers.

1. Consider a strategy that gains exposure to all three currencies

AT1 CoCos are typically issued in three currencies USD, Euro and GBP and each currency benefits from unique issuers that may only issue AT1s in one of the three currencies. Table 2 provides an overview of issuers that issue AT1 CoCos in different currencies with those that only issue in one currency highlighted in grey2. Gaining exposure to a diversified universe of AT1 CoCos in all three currencies can provide better issuer diversification over only gaining exposure to AT1 CoCos in one currency. For example, as of 31 March 2019, Bloomberg reported ABN AMRO with a common equity tier 1 ratio (CET1) of 18.4% and Nationwide at 31.7% both examples of issuers with very high cushions against maximum trigger levels which are typically 5.125% for low trigger CoCos and 7% for high trigger CoCos.

Table 2: AT1 CoCo issuers within each currency bucket

Source: WisdomTree, Markit. Data as of 31 March 2019. The strategy is represented by the iBoxx Contingent Convertible Liquid Developed Europe AT1 Index. Issuers in grey cells are issuing in the specified currency only. You cannot invest directly in an index.

Historical performance is not an indication of future performance and any investments may go down in value.

2. Issuance patterns point to Euro and GBP denominated AT1 CoCos becoming a larger share of the market

As AT1 CoCo issuance from banks in different currencies differ annually, not allocating to the Euro or GBP segment would mean the investor would miss out on exposure to vast new issuance. Since 2013 when USD denominated AT1 CoCo issuance accounted for nearly 90% of the supply, the market has evolved and in 2017 the Euro and GBP denominated segment accounted for nearly 52% of new issuance. In 2018, the Euro and GBP denominated issues accounted for nearly 45% of new issuance with the 1Q of 2019 dominated by USD and Euro issuance. Further highlighting the importance of a multi-currency approach to the asset class.

Figure 3: AT1 CoCo market issuance patterns since 2013

Source: WisdomTree, Markit, Bloomberg. Data as of 31 March 2019. AT1 CoCo market is represented by the constituents of the iBoxx GBP Contingent Convertible Index, the iBoxx EUR Contingent Convertible Index and the iBoxx USD Contingent Convertible Index. The issuance is based on the first settlement date of the underlying CoCos in the referenced indices. The exchange rate applied to Euro and GBP issuance is the exchange rate reported by Bloomberg based on the last price available as of 18:00 London time on the first settlement date. You cannot invest directly in an index.

Historical performance is not an indication of future performance and any investments may go down in value.

3. Data highlights that European banks from developed Europe generally have well-funded CET 1 ratios

Figure 4: CET1 ratio breakdown by currency exposure and CoCo trigger type for the AT1 Index

Source: WisdomTree, Markit, Bloomberg. Data as of 31 March 2019. The AT1 Index is represented by the iBoxx Contingent Convertible Liquid Developed Europe AT1 Index. Maximum trigger level is represented by the maximum trigger observed across all CoCo issues of a given issuer.

The CET1 ratio is the Common Equity Tier 1 Capital ratio. High trigger CoCo is a CoCo with the trigger level set at 7% of RWA (risk-weighted assets), low trigger CoCo is a CoCo with the trigger level set at 5.125% of RWA. You cannot invest directly in an index.

Historical performance is not an indication of future performance and any investments may go down in value.

When considering the issuers within the AT1 CoCo universe, issuers within each currency bucket exhibit different levels of capital adequacy as represented by their CET1 ratios. According to data from Figure 4, it is worth mentioning that while the GBP segment is small, the CET1 ratios tend to concentrate on the higher levels while the Euro and GBP issues exhibit a broader spectrum of CET1 ratios. As of 31 March 2019, the CET1 ratios of issuers within the iBoxx Contingent Convertible Liquid Developed Europe AT1 Index were above their trigger levels with approximately 70.8% of the issuers within the index reporting CET1 ratios between 12% to 18% or higher.

When incorporating any new asset class within a portfolio, it is judicious to review the market to understand the underlying dynamics of the universe and more specifically to understand which vehicle to use to gain market access. For AT1 CoCos, an investor can potentially find benefits to investing in a diversified passive approach that limits issuer exposure, requires the bonds within the index to have at least one rating by one of the three main rating agencies and gains access to a multi-currency approach that invests in a broad number of issuers meanwhile excluding unwanted risks such as emerging market exposures. The holdings transparency inherent in an ETF also allows an investor to better manage exposures across their portfolio and try to optimise the diversification benefits of adding an allocation to AT1 CoCos.

Source

1 Data inferring about the AT1 CoCo market is represented by the constituents of the iBoxx GBP Contingent Convertible Index, the iBoxx EUR Contingent Convertible Index and the iBoxx USD Contingent Convertible Index.

2 Bond issues and issuers are based on data from the iBoxx Contingent Convertible Liquid Developed Europe AT1 Index.

Related blogs

+ Can AT1 CoCos be the better way to play the European bank trade?

+ AT1 CoCo bonds are in the news…but why?

Related products