It's a small (cap) world after all

As we have discussed many times at WisdomTree, small companies—and especially small companies that pay dividends—may offer investors some rather large opportunities.

And these opportunities can be quite global.

Small companies, big dividends

Small cap dividend payers exist in emerging markets, in Japan, in the US, as well as in Europe and everywhere around the world. Further, they often pay larger dividends than you may expect.

In Figure 1, we indicate WisdomTree’s approach to Small caps which:

1) Only includes dividend-paying small cap stocks and,

2) Weights those dividend-paying small cap stocks by their cash dividends.

This approach has led to the potential for higher dividend yields in markets around the world. While dividends themselves are something that investors can touch and feel at a regular frequency (so long as they are paid), Figure 1 represents the relationship between the current share prices of the underlying index constituents and the dividends that those constituents have paid over the prior 12 months. Within each respective colour, we are illustrating the difference that WisdomTree’s dividend-weighted approach has made relative to a relevant, well-known, market capitalization-weighted benchmark. While the magnitude of the dividend yield difference may change over time, the fact of the dividend-weighted approach having a higher dividend yield than the market capitalization-weighted approach has been consistent throughout the live history of these specified indices.

At each annual rebalance:

- Stocks whose share prices have risen quickly but whose dividend growth has not kept pace will tend to see their weights reduced within WisdomTree’s methodology. With market capitalization-weighted approaches, stocks with greater market capitalization receive greater weights, regardless of valuation.

- Stocks whose share prices have remained flat or fallen, but whose dividend growth has been relatively stronger will tend to see their weights increased within WisdomTree’s methodology. With market capitalization-weighted approaches, stocks with smaller market capitalization receive lower weights.

Figure 1: Illustrating the difference WisdomTree’s dividend methodology has made

Data is measured on 21 September 2018. You cannot invest directly within an Index.

Historical performance is not an indication of future performance and any investments may go down in value.

Why small caps globally?

As the world has become more interconnected, large cap companies tend to be multinational and do business globally. Small caps, on the other hand, tend to be much more exposed to their local economies. If one is thinking of diversification on the basis of economic conditions and growth potential in different segments of the world, small caps may provide an interesting tool to use for this type of execution.

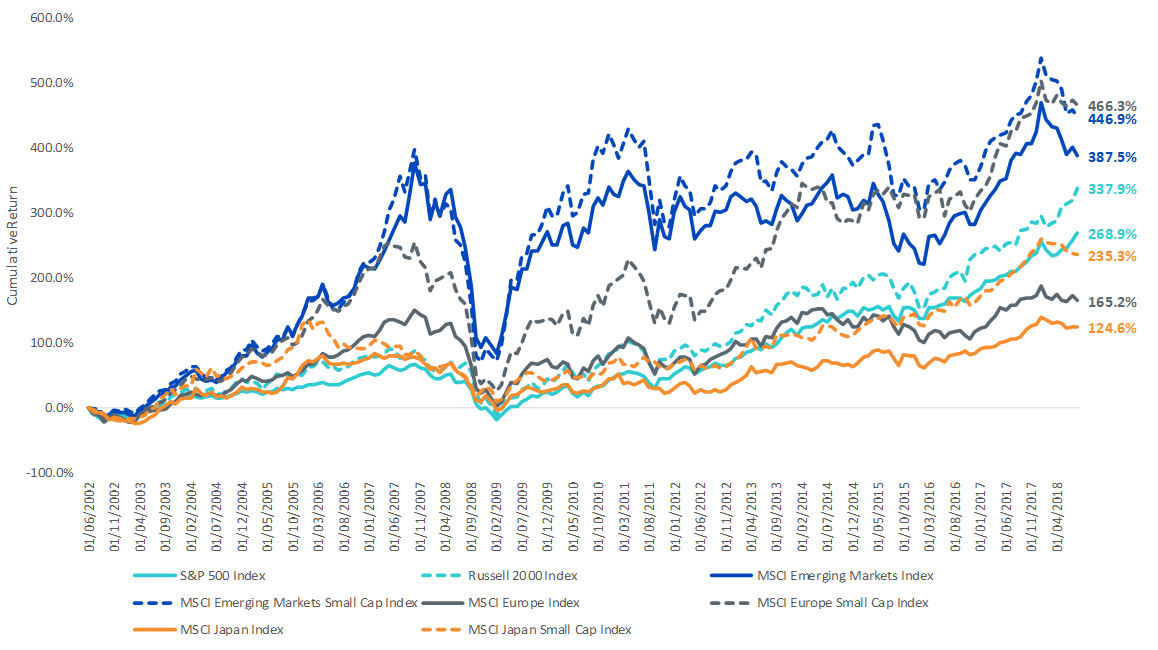

History has shown, as can be seen in Figure 2, that small caps have delivered strong performance over their large cap counterparts from 30 June 2002 to 31 August 2018.

Figure 2: Small caps vs. large caps in select regional equity markets

Source: Bloomberg. Returns are shown net of foreign tax withholdings. The period of 30 June 2002 to 31 August 2018 was selected due to data availability for the Russell 2000 30% Net of Tax Index, which is used to calculate the Russell 2000 Index’s return’s net of withholding taxes for non-US based investors. You cannot invest directly within an Index.

Historical performance is not an indication of future performance and any investments may go down in value.

We have listed four areas where we believe small caps are of particular interest:

United States

In a world dominated by trade-rhetoric, small cap companies in the US do the majority of their business within US borders and are less exposed to trade. Additionally, prior to the corporate tax cuts of December 2017, they were paying higher effective tax rates than their large cap peers, and therefore benefitted more from this policy change.

Japan

Japanese small caps receive the vast majority, approximately 80%, of their revenues from inside Japan. As the economic policies from Prime Minister Shinzō Abe focus on domestic Japan, small caps may be a better way to benefit than larger, export-oriented firms.

Europe

European small caps tend to be very well geared to shifts in sentiment, and they also do most of their business domestically. At times when it has been beneficial to avoid Europe’s largest banks, small caps have had this natural side effect.

Emerging Markets

Many investors we speak to focus on the billions of consumers within emerging markets raising their standards of living and driving global growth. Small cap companies better tap into this demographic theme.

Small caps can complement existing strategies

In many cases, we have seen the most enthusiasm from investors who have not considered small cap equities before, particularly in markets outside of their home region. Tapping into local revenue streams could be a critical element to bring the potential for differentiated performance.

Related blogs

+ The unique advantages of dividends

+ The large advantages of small companies

Related products

+ WisdomTree Europe SmallCap Dividend UCITS ETF (DFE)

+ WisdomTree Japan SmallCap Dividend UCITS ETF - USD (DFJ)

+ WisdomTree Emerging Markets SmallCap Dividend UCITS ETF (DGSE)

+ WisdomTree US SmallCap Dividend UCITS ETF (DESE)