How does roll yield affect your commodity returns?

Robust global economic growth and rising geopolitical tensions give commodity investors plenty of reason to be upbeat in 2018. This positive sentiment is reflected in both prices and investor flows, with broad commodity baskets having outperformed the S&P 500 year-to-date, and global commodity ETF flows hitting multi-year highs.

However, unless investors are attentive to the return components driving commodity ETPs and the underlying futures being tracked, they could be left disappointed with their investment’s performance. Hence, we explore the different return components of commodity futures, focusing particularly on the impact of roll yield.

Dissecting returns

Most commodity spot prices are not investable. Instead, the futures market represents the easiest and most efficient way for investors to gain access to commodities and investing in commodity futures comprises of three components: the spot return, roll return (or roll yield) and collateral return.

The spot return simply reflects the change in the price of a given commodity for immediate delivery. Of equal importance however, is the roll return - an often-forgotten component that reflects the inherent costs (or benefits) of physically owning commodities, such as storage costs, insurance costs and transportation costs. Depending on the shape of a commodity’s futures curve, the roll return can significantly impact investors’ returns.

In contango markets, the futures curve is upward sloping (i.e. there is a net cost associated with holding a commodity, hence longer dated futures contracts are more expensive than near-dated contracts), thus the roll return is typically negative as futures prices converge over time to spot.

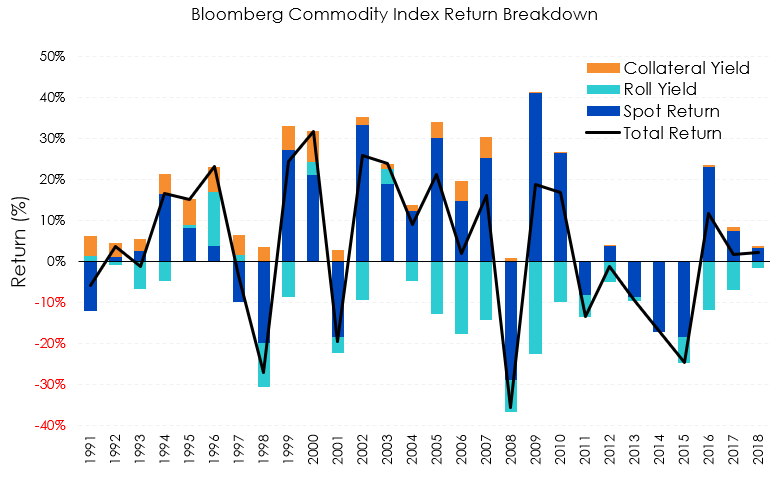

Figure 1: Don't Ignore Roll Yield in Your Commodity Returns

Source: Bloomberg, WisdomTree, data available as of 31 March 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Table: Composition of returns over time

Source: Bloomberg, WisdomTree, data available as of 31 March 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Conversely, if the curve is downward sloping (i.e. there is a net benefit to owning commodities now, hence further out contracts are cheaper than near-month contracts), the market is said to be in backwardation.

Given the prevalence of contango across commodity markets over the past few decades, roll return in broad commodity baskets, such as the Bloomberg Commodity Index, has presented a drag on investor returns as seen in Figure 1. In 2016 for example, the roll drag on returns was equivalent to nearly 12%, reflecting a major supply glut in oil and Chinese stockpiling of base metals. Since then, this return drag has eased, and commodity investors may see roll yield being less of a concern for reasons outlined below.

From Structural Contango to Backwardation

Oil futures have seen a dramatic shift from structural contango to backwardation over the past year. This has eliminated one of the largest sources of negative roll return in broad commodity indices such as the Bloomberg Commodity Index. A bit of context explains these recent shifts.

In the post global financial crisis period of 2011-2014, oil futures were predominantly in backwardation. Strong global demand for oil was accompanied by OPEC’s strong control over oil supplies, and their policy of maintaining supply tightness allowed near-term prices to remain high.

In 2014 however, OPEC changed its strategy, seeking to reclaim lost market share from higher cost producers such as the US who had steadily ramped up production in response to higher prices. The resulting increase in OPEC production flooded global oil markets, causing spot prices to collapse from US$100+/bbl in 2014 to under US$30/bbl in 2016. This triggered a complete reversal in the futures curve for oil from backwardation to contango, as fears of oil shortages turned to fears of an unending supply glut. During this period, ongoing overproduction and a shortage of storage facilities helped push up storage costs, further deepening oil’s contango. The negative roll return during this time reached as high as 3.5% per month.

In 2016, OPEC changed strategy once again, and announced production curbs (to commence in 2017) to drain excess global inventories. That led to oil futures curves shifting back to backwardation. OPEC’s renewed credibility, following a protracted period of compliance with its curbs, has led to all major oil futures curves remaining in backwardation since the second half of 2017. With OPEC unlikely to abandon its recent strategy and no negative demand shocks expected, we are likely to see oil futures remain in backwardation for the foreseeable future.

Seasonal Contango Returns

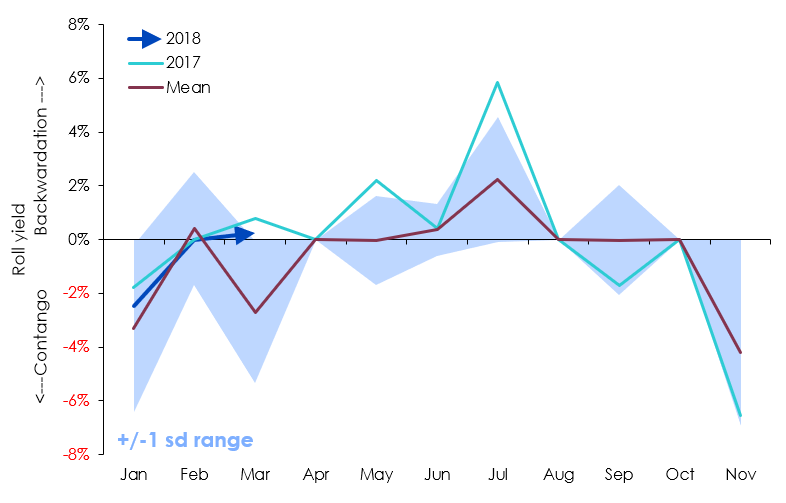

The roll pattern in some futures is highly seasonal. In contrast to oil, where traditionally we have seen long periods where the whole curve is in backwardation or whole curve is in contango, some commodities like natural gas or livestock are in backwardation in some parts of the curve and contango in other parts of the curve.

The timing of the backwardation/contango tends to be persistent following a seasonal pattern. For example, backwardation in livestock futures tends to become pronounced between May and July. Prompt month prices tend to be higher due to peak demand in the summer and prices tend to be lower further out in the curve as supply increases later in the year due to biological factors and weather.

Figure 2: Seasonality in livestock roll yields

Source: Bloomberg, ETF Securities, data available as of close 04 May 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Although the seasonal patterns for hogs and cattle are slightly different, as a group livestock has consistent seasonality as seen in Figure 2. Positive roll yields in July average 2.3% (1992 to 2017), while negative roll yields average 4.2% in November (1992 to 2017). With the summer months fast approaching, the seasonal backwardation and positive roll return in livestock commodities could present an additional source of returns for commodity investors.

Conclusion

Negative roll returns have long represented a drag on commodity investors’ returns, both for individual commodities and broader baskets. However, we expect this to ease amidst improving commodity fundamentals, such as oil’s easing supply glut, and the seasonality element for livestock commodities, both of which are enforcing backwardation across several key commodities.