India: at the junction of recovery and growth

In an otherwise challenging and often bearish investment landscape, India is the only large accessible economy that is projected to grow at 7% or more for a foreseeable future(1). Unlike China, which for many years economists have emphasised should shift from an export-centric model to a more self-contained economy, India has been an economy sustained by its own consumption.

Below, we highlight what a roaring Indian economy might mean for investors.

Indian model: sustainable debt levels with demographics and households driving consumption-led growth

+ Underleveraged: Due to its relatively low debt levels, India can increase debt issuance with ease, thereby accelerating growth without running into the risk of excess debt levels. In 2015 Domestic Credit to the private sector (% of GDP) stood at 52.6% for India compared to 153.3% for China. This reflects China’s years of rising debt and state-driven investments which have created excess capacity in several sectors.

+ Demographics propelled: By 2050, India’s workforce (that is, people between 15-59 years old) is expected to have grown from the current 674 million to a staggering 940 million. To put this into perspective, the US workforce will be a little over 200 million in 2050 at its current rate and China is likely to be facing a shrinking workforce. This will potentially drive up labour costs in China – which would be a dent to its competitiveness.

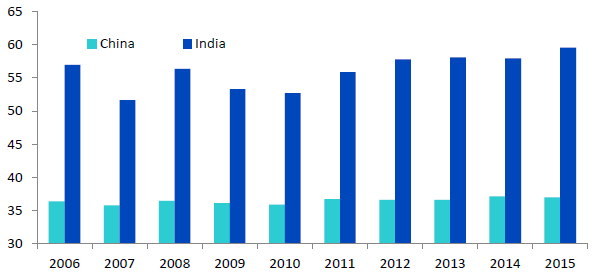

+ Consumption driven: Juxtaposing India’s favourable demographics with its consumption expenditure, it’s no surprise that India’s ~60% consumption expenditure to GDP ratio is much higher than the ~39% of China(2). This indicates an economic model that is hugely influenced by local consumption (see figure 1) with greater potential insulation from global headwinds.

Figure 1: Household consumption expenditure (% of GDP)

Source: World Bank, as of 31/01/2017

Participating in the growth of India

Unlike China’s, India’s growth is, to a great extent, fuelled by its fast-growing middle-class and internal consumption. When we combine these consumption numbers with burgeoning demographics, we get an economy that we believe offers unparalleled growth potential.

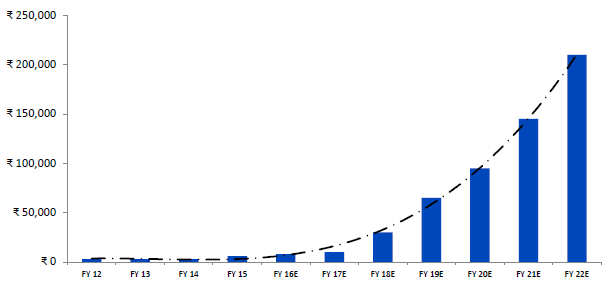

To give a sense of growth trends in India, there is an astounding projected rise of Indian Gen ‘X’ mobile banking use, as shown in figure 2.

Figure 2: Mobile banking - projected market size(in INR (₹) Billion)

Source: Bank of America, Merrill Lynch as of 30/06/2016

Liberalisation of the economy and key reforms

Another key element to India’s growing economy is that the Modi government has been gradually opening various sectors of the economy to foreign investors. Areas like Construction Projects, Cable Networks, Agriculture and Plantation (Coffee, Rubber and Palm Oil, etc.), Air Transportation (non-scheduled and ground handling) are now allowed to have 100% Foreign Direct Investment (FDI). While other sectors like Defence and Broadcast have been allowed, for now, an increase to 49% in FDI. We believe this creates opportunities for investors to invest in sectors which were not accessible earlier.

The Modi government is also in the process of implementing what could be the single biggest tax reform under the ‘Goods and Services Tax’ or GST bill. Under this taxation scheme, all states and central taxes would be combined to create a consistent tax structure across the entire country, converting the whole nation into one market place. Several other key reforms on boosting consumption, infrastructure spending, debt recovery for banks, etc., are also in the process of being implemented.

Market outlook

Strategically India has strong growth potential, but what about tactical opportunities? From a monetary policy standpoint the Reserve Bank of India (RBI), after having successfully fought inflation from highs of 11.51% YoY as of November 2013 to its current lows of 3.41% as of December 2016, has engaged in consecutive rate cuts to spur growth.

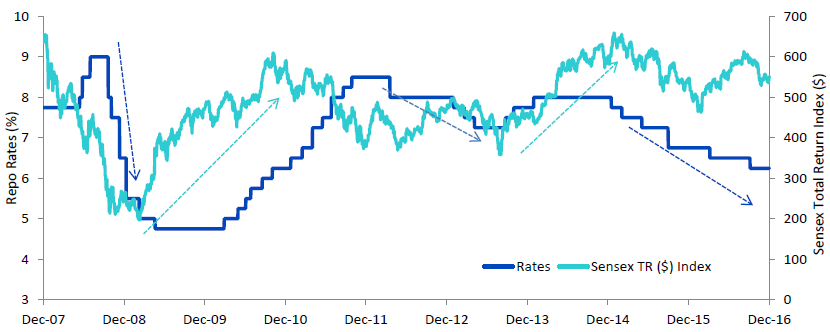

Figure 3 shows how the Sensex, India’s leading index, has traditionally delivered double-digit annual returns, with a lag, following the last two rate cut cycles by the RBI. The table breaks down realised returns for a one-year period after the corresponding rate cuts cycle ended.

Figure 3: Sensex reacting positively to rate cuts (12/31/2007 - 12/31/2016)

Source: Bloomberg, WisdomTree. Past performance is not a reliable indicator of future performance.

Table 1: Returns delivered by Sensex Index one year after past rate cut cycles ended

|

Consecutive Repo Rate Cut Cycles |

SENSEX Returns (in $) |

||||

|

Phases |

Time Period Engaged |

Rate Starting Level |

Rate Ending Level |

Time Length |

Total Returns |

|

Phase 1 |

Oct. 2008 - May 2009 |

9.00% |

4.75% |

May 2009 - May 2010 |

19.46% |

|

Phase 2 |

April 2012 - May 2013 |

8.50% |

7.25% |

May 2013 - May 2014 |

18.53% |

|

Phase 3 |

Jan 2015 - Present* |

8.00% |

6.25% |

- |

- |

*As of 31/12/2016. Source: Bloomberg, WisdomTree. Past performance is not a reliable indicator of future performance.

Conclusion

India is at an interesting crossroad where leadership is pro-actively taking tough reforms for long-term growth. Two pillars of the Indian economy, that is consumption and demographics, have encouraging projected growth numbers.

What we see right now in India is the following:

(1) Policymakers are not shy of taking bold steps and opening the economy

(2) A central bank that successfully fought inflation is now supportive of growth through lenient monetary policy

(3) We have a global macro environment that is not disruptive of growth in India

(4) Financial planning that is accelerating consumption, infrastructure and digitisation

Source

(1) Source: IMF projections until 31/12/2020, as of 31/12/2016

(2) World Bank, as of 31/1/2017

You might also be interested in reading…

+ 2017 Japan outlook: poised to perform

+ Our thoughts on allocating for a President Trump world

Investors sharing this sentiment may consider the following UCITS ETFs: