A year to focus on currency risk: What can European investors do?

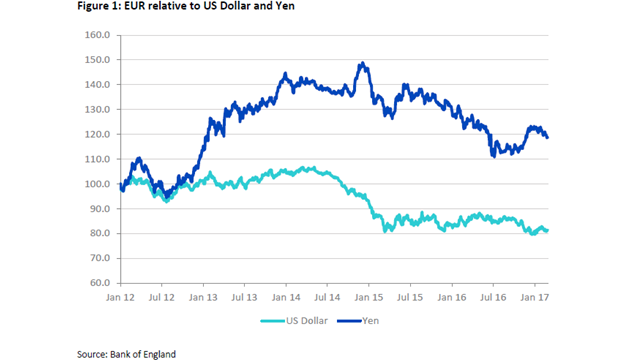

European investors are well acquainted with not just the impact of currency risk but the consequences on their equity returns. Over the past three years the Euro has weakened substantially versus the US Dollar, falling by over 22% since January 2014. This has been a boon for investors holding US Dollar denominated assets, typically represented by US equities, which comprise over 60% of a standard MSCI World Developed Markets benchmark. Japan, which at 8.7% is the second largest market in MSCI World, is also an exposure where managing currency risk is key.

2017 may prove to be a landmark year for foreign exchange rates and risk, especially in the context of the Euro. Realised 60 day volatility against the US Dollar, which reached long term low levels at below 4% as recently as September 2014, have recently risen to over 11%. Whilst below previous highs of close to 13% reached in September 2015, it is likely that in an environment of heightened political risk, volatility will remain at elevated levels.

In the short term the key risk for the Euro is further weakness based on the twin prongs of a resurgent US Dollar and the concerns, from various political angles, about the viability of the Euro. In this context it is entirely possible that the Euro could reach parity, which would imply a potential further depreciation of 5%. Counteracting this is the medium term expectation that once through the bulk of the most contentious European elections and with the prospects of rising US interest rates sufficiently discounted the Euro may well enter a phase of stability against the US Dollar.

To hedge or not to hedge?

Two themes are therefore relevant to consider in these scenarios. Specifically having a hedged exposure to US equities via a hedged share class can be important to preserve the equivalent of local equity returns should the Euro strengthen. The flexibility afforded through having an unhedged share class also means that investors can switch accordingly depending on their view of currency movements.

A weak Euro makes it worthwhile to consider export oriented stocks. These typically benefit from such currency moves, and are dominated by large cap multinational companies. We offer both a hedged and unhedged European Equity strategy which provides investors with different choices from a portfolio perspective. Owning Eurozone equities with a long position in the US Dollar via the US Dollar hedge is a way to take into account two sets of returns.

The Yen represents a different opportunity for investors with the Japanese economy in the midst of substantial structural reform and with growth expectations predicated on a weaker Yen. As European investors have seen over the past six months, this decline in the Yen even in the face of a weak Euro would have impacted the returns of unhedged investors in Japanese equities. The Bank of Japan is committed to targeting close to zero interest rates and the government is committed to stimulating domestic demand. In order to position for the expected rebound in corporate earnings and economic activity, WisdomTree believes that an export tilted basket of dividend paying equities combined with a currency hedge may be appropriate. European investors can use either a hedged or unhedged strategy allowing for a flexible approach to managing currency risk.

We expect that currency volatility will remain a feature of markets in 2017 due to the significant number of macro-economic forces at play. Managing currency risk allow investors to focus on the core part of their investment allocation in equities which is typically assessing local equity returns.

WisdomTree’s currency hedged strategies as shown in the table below, offer both choice and ease of use.

WisdomTree's available currency strategies

|

Export-tilted strategies |

Equity Income |

|||

|

WisdomTree Europe Equity |

WisdomTree Japan Equity |

WisdomTree Germany Equity |

WisdomTree US Equity Income |

|

|

Unhedged |

||||

|

USD hedged |

- |

|||

|

GBP hedged |

||||

|

EUR hedged |

- |

- |

||

|

CHF hedged |

- |

|||