Economics trumps politics in Europe: it’s bearish bonds, bullish banks

The bullish conviction in European bonds is dissipating, while bank stocks are rallying. Blame Brexit, Trump’s US presidential win, Italy’s “no” referendum on constitutional reform and now the ECB’s QE “taper.” These macro events have inflicted violent price corrections in government bonds but the longer term ramifications to specific risk assets – most notably bank stocks – may be bullish. The Eurozone’s deeply discounted banking sector – particularly Italy’s – offers investors potential entry points as the premium prices of safe havens are under pressure.

We believe the Eurozone’s banking sector discount will continue well into 2017. For the reasons outlined below, bearish bonds and bullish banks is a tactical asset allocation trade that investors may consider before the end of the year.

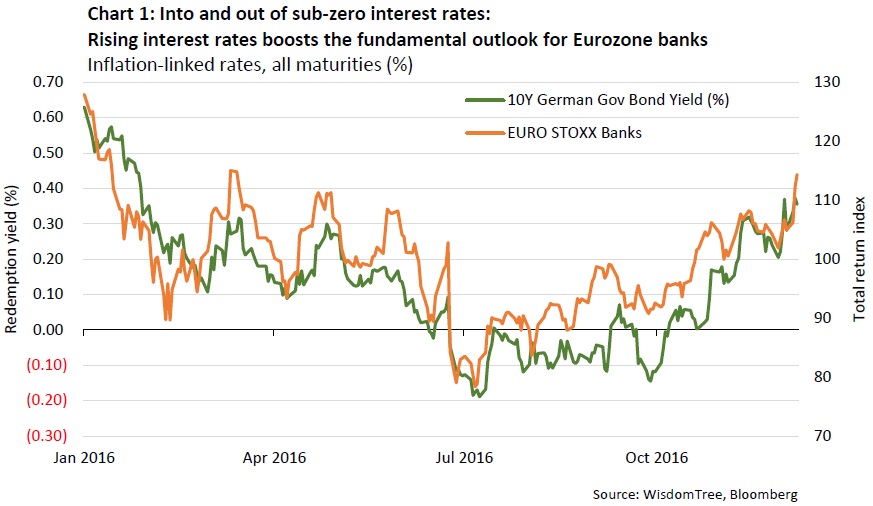

Chart 1 below shows how – underpinned by these macro events – the rise in interest rates since July has sharply reversed the downbeat sentiment in Eurozone bank stocks. Since July the EURO STOXX Banks index is up 37% and the yield of Europe’s safest save haven, the German Bund, rose 49 bps.

Past performance is not indicative of future performance

ECB’s QE taper - extend to shield against 2017 political risk downside

The ECB’s language has become more upbeat, arguing a moderate but firming recovery in the Eurozone as a key driver for its decision to taper the monthly purchases from EUR 80bn down to EUR 60bn between March 2017 to at least December. If the extension works as a shock-absorber during renewed political uncertainty with next year’s general elections in France (in May), and Germany (in September) – then we believe bond markets should prepare for the lowered upper bound to come down after these elections in September. With pressure on investors to discriminate high grade debt in Europe more vigorously, we expect government bond yields to adjust higher and credit spreads to widen.

Trump win - reinvigorating to risk-on asset allocation shift

The upbeat expectations of US economic growth appear to have brushed aside the geopolitical uncertainties around Trump’s anti-transatlantic partnerships on trade and defence rhetoric. Trump’s win reverberated in European bond markets more forcefully than Europe’s own internal political strife. European government debt yields rose sharply in the days leading up to the US presidential election and, following Trump’s victory, settled 50 to 100 bps higher. If investors expecting Trump’s aggressive pro-growth agenda to improve fundamentals for the US economy, we believe the expectations of the Fed further tightening may raise credit risks in European sovereign debt where a low to no inflationary environment adds to the real interest burden, most notably of overextended countries such as Italy.

Trump has reawakened the risk-on asset allocation shift. In so doing bond yields globally have risen, and in Europe emerged out of zero/sub-zero territory. The ramifications of US-induced rising rates in Europe to banks’ loan and trading books we believe will potentially be a boost to the outlook of bank profitability. Banks can, in all likelihood, still refrain from charging deposit account holders additional fees and risk losing customers if they do, even while steepening yield curves revive opportunities for banks to engage in carry trades.

No referendum and Renzi resignation not cutting short Italian bank sentiment

Signs have emerged in Italy of a heightened sense of urgency to deal with bank restructuring before the caretaker government under Renzi dissolves for new elections next year.

Following its asset sale of Polish lender Pekao and of its investment arm Pioneer to be sold to Amundi, Unicredit has opened up an opportunity to warm investors for a EUR 13 billion capital raising to bolster its capital buffers, and in so doing alleviate concerns of systemic risk posed by Italy’s largest bank. The large upside potential, underpinned by the deeply discounted valuations with which Italian banks trade relative to peers elsewhere in Europe and broader equity market benchmarks, we believe will compel investors to react positively to the market-based solutions sought by Italy’s largest banks to restructure and recapitalise.

While not systemic but politically toxic, the fate of Banco Monte Dei Paschi Di Siena (BMPS) is likely to be an isolated event. It is readying itself for state support while preventing a political fallout through a plan that may revert to using deposit insurance as a means to limit the losses on retail investors holding significant exposure in BMP’s subordinated bonds, which – according to EU rules on bank rescues – must take losses before tax money is deployed to fund the bail-out. Whatever happens to BMPS, the markets have begun re-rating Unicredit and others regardless.

Brexit - credit at risk amid deteriorating state finances and uncertain trade models

Bond market bearishness in the UK has been underscored by concerns over import-driven inflation fears following the plunge of the Sterling as a result of the Brexit vote earlier this year. The marked debased value of the Sterling is against a backdrop of debt-fuelled spending by households who, faced with likely much higher energy bills and transportation costs, could see their propensity to spend diminished. In that case the feedback loop is negative – slowing economic growth will translate into a weakening tax take for the Treasury. This at a time when it is preparing to unleash more deficit spending to soften the blow on the persisting uncertainties of the kind of trade model the UK seeks with the EU. So far it’s too early to see if Brexit has damaged trade, investment or growth. Going by the latest releases, the economy appears to be on a strong growth trajectory and sentiment is upbeat. The constant back and forth discussions of parties in Parliament over the when and how to leave the EU in an orderly fashion suggests the stakes are high enough to warrant the date for when Article 50 is triggered – currently planned for March 2017 – to be pushed out.

Conclusion

Political macro events have reinvigorated a risk-on asset allocation trade, most notably in Europe where the premium prices charged on government debt contrasts with deeply depressed valuations of bank stocks. That these dislocated valuations are beginning to unravel (close/reverse) between both asset classes are in response to ECB’s confidence in Eurozone’s path to sustainable recovery as it pairs back QE, and the urgency of seeking market solutions for bank restructuring ahead of any political outcome in Italy and Europe. Economics, more than politics, is trumping the sentiment in Europe’s financial markets. We believe investors should consider acting on the former accordingly.