Why Chasing Momentum in Emerging Markets May Be Short-Lived: Rebalancing to take advantage of better value

It is often thought that “inefficient markets” – like Emerging Markets (EM) – are where there are great opportunities for active managers to add value. It would stand to reason that if there is a large opportunity for outperformance, there is also a large opportunity for underperformance. In other words, someone must be on the other side of the ‘inefficiencies.’

Goldman Sachs strategists Caesar Maasry and Jane Wei recently wrote a note about how the trends towards ETFs and passive strategies have been impacting Emerging Markets’ asset prices. Goldman notes the large ETF flows have been associated with “the sharp rise of EM asset prices; the underperformance of EM actively managed funds, and the rotation out of EM small caps into large caps.”[1]

Active EM equity strategies have garnered less than $20bn of cumulative flows over last 13 years, while passive flows have seen more than $110bn of inflows on a cumulative basis. In Europe, passive strategies for EM equities have been exceptionally resilient this year, recording EUR7.5bn of inflows – more than the EUR6.4bn of inflows in 2013, 2014 and 2015 combined (see Chart 1) as well as beating the flows in active strategies in each calendar year.

Passive investment strategies for Emerging Markets have demonstrated their effectiveness. However, the real question is: How does an investor allocate to the countries and sectors that make up Emerging Markets?

What has moved in Emerging Markets this year was the out-of-favour value exposures in countries like Brazil and Russia, each of which have a high Energy and Materials equity bias. There has undoubtedly been strong performance across Emerging Markets countries this year. For instance, of the 10 largest countries in the WisdomTree Emerging Markets Dividend Index, we have observed the following rank in YTD performance in USD terms [2]:

At the top of the performance list was Brazil, rising by 59% which saw large gains in both its equity market and its currency. Second was Russia, gaining 36%, followed by Indonesia (30%), Thailand (26%) and South Africa (23%). Something these countries all have in common is their connection to commodity prices and exports. Following years of subdued and negative expectations, stability in commodities led to a strong rebound in all these markets and their currencies. [3]

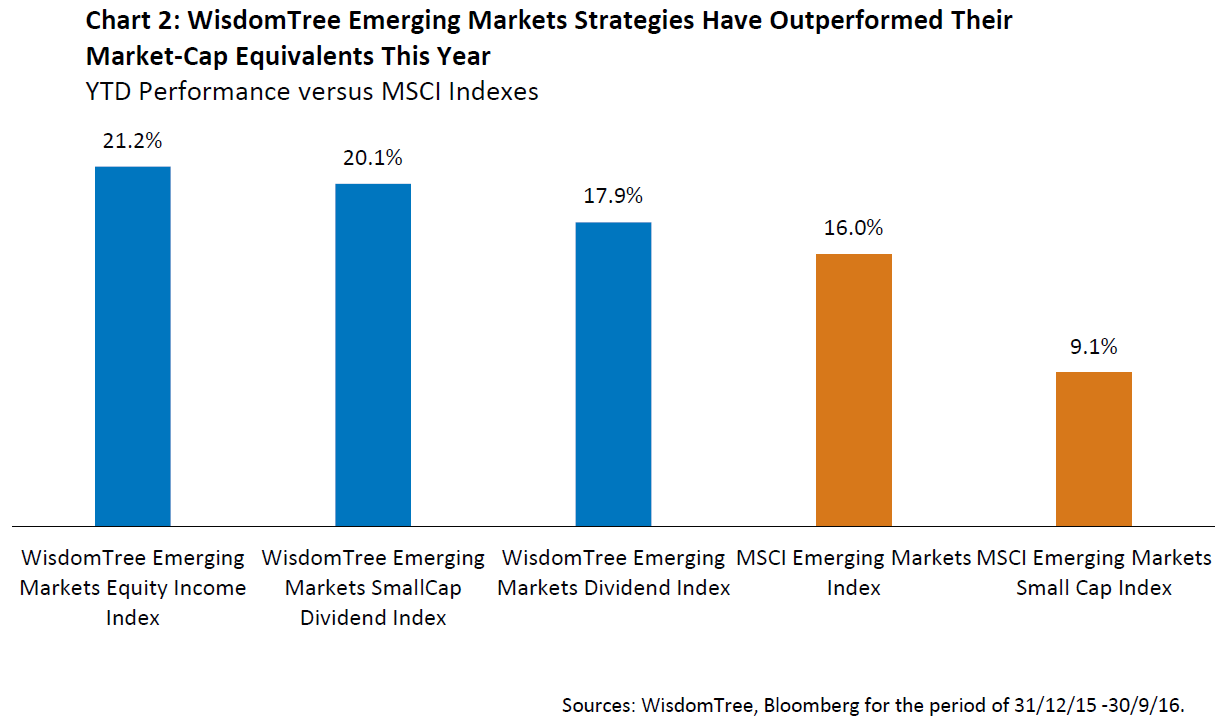

Investors will have chased momentum but will have ignored (high) valuations if they invested in a market-cap based strategy where exposure is based on price. Can we now expect this passive approach to continue to perform well when, on the back of higher prices, valuations have risen?

Rebalancing away from commodity-based sectors to mitigate valuation risk

Commodity-oriented sectors and countries have been strong market performers in 2016, and the gains are coming at levels greater than changes in the underlying fundamentals of companies, as measured by their Dividend Streams® in USD.

Following the close of trading on 20 October the WisdomTree Emerging Market Indices rebalanced into new holdings and weights, and WisdomTree announced its latest Index constituents on the back of it.

From the annual screening date, the:

(1) WisdomTree Emerging Markets Equity Income Index (ETF: DEM) reduced weight in the commodity sectors [4] by more than 6% while increasing exposure in Telecommunications and Utilities stocks by a similar total in aggregate

(2) WisdomTree Emerging Markets Small-Cap Dividend Index (ETF: DGSE) reduced weight in the commodity sectors by 3% while adding 2.5% in Telecommunications and Utilities stocks

Brazil is a reflection of this, as its gains were far and above any other country. Consequently, Brazil exposure was reduced to under 5% across both strategies. By contrast, the biggest recipients of added weights were Taiwan in DEM and Thailand in DGSE (about 3%).

This is a big difference between a cap-weighted index – which rides momentum of stocks to higher and lower weights – and a dividend-weighted and high-yield screened index that is designed to identify opportunities based on changes in relative valuations.

Market-Cap indices: Momentum following means being insensitive to valuation

To reiterate: Traditional market cap-weighted indices do not look for valuations and fundamentals in setting exposure. They look only at stock prices (multiplied by shares outstanding).

While the gains in commodity-based stocks in 2016 were due to more than the underlying changes in dividends – and hence our index process lowers exposure to these companies – the overall valuations still result in an over-weighted position.

Of all the indices we calculate, the lowest valuations and highest dividend yields tend to be found in the WisdomTree Emerging Markets Equity Income Index. Following this rebalance, we expect the valuations of the portfolio to compare favourably to market cap based passive strategies, resulting in a lowering of valuation metrics such as the price-to-earnings (P/E) ratios and a raising of the dividend yields.

If investors are revisiting Emerging Market, they should be considering the value proposition of high dividend yielding companies as opposed to chasing the momentum story.

- WisdomTree Emerging Markets Equity Income UCITS ETF (DEM)

- WisdomTree Emerging Markets SmallCap Dividend UCITS ETF (DGSE)

Sources

(1) Goldman Sachs Blog post: “Global Markets Daily : Active vs Passive and the EM alpha challenge” by Maasry , and Wei as of 13 October 2016

(2) WisdomTree. Performance from 31 December 2015 to 30 September 2016

(3) WisdomTree, Bloomberg, 12/31/15–9/30/16. Currency return measured against the U.S. dollar.

(4) Commodity sectors are: Materials and Energy