Dislocation Dislocation Dislocation BoE Stimulus Elevates Yield Premium for UK Dividend Payers

In this brief, we outline why UK equities now offer an even more compelling income alternative to fixed income:

+ Brexit fears and BoE stimulus have driven a UK fixed income valuations to historic highs. Investment-grade UK credit yields no longer beat inflation.

+ With bonds offering increasingly negative risk-adjusted yields, the term risk incurred has lost justification. Cash, or better still, dividend equities, represent superior income alternatives.

+ Broad baskets of dividend payers may provide investors with an efficient, low-volatility solution to tackling the deepening income crisis.

Dislocated Bond Markets May Present UK Equity Value Opportunity

Chart 1 compares the earnings yield (inverse of the 12 month trailing P/E ratio) of the FTSE All-Share Index against 10Y UK Gilt yields. Since the turn of the millennium, the equity-bond yield spread has progressively widened, underpinned by successive rounds of QE and rate cuts by the BoE in recent years. As bond yields have been driven to the floor, valuations have overextended, leaving UK gilts now at their most expensive since 1997.

By contrast, UK equity market valuations appear to be at their most attractive in recent years relative to UK bonds. Consider the FTSE All Share’s current earnings yield: at 4.8% vs the redemption yield of 10Y Gilts at 0.67%, equity valuations are a far cry from crisis levels, particularly dividend payers.

Let’s then look at the 1999 tech bubble : overextended equity market valuations drove earnings yield to just half the 5.5% redemption yields of 10Y UK Gilts. Following the tech-bubble burst, discounted equity valuations remained barely on par with longer-dated Gilts, providing not enough of an incentive for long-term investors to allocate back into equities. For instance, in a dramatic asset allocation shift, the defined benefit pension scheme of Boots PLC actually sold out of its 75% equity exposure in 2001, converting the portfolio into a 100% long-dated high-grade bonds position.

Alternatively, take the 2008 financial crisis: the equity yield was at a premium to bonds following deep monetary policy rate cuts by the BoE and amidst a broad-based slump of UK equities, most notably in financials and materials. Despite an earnings recession, the discount of UK equities was disproportionate, and with earnings yields nearly double the yields of long-dated gilts in 2009. The value proposition of the UK equity market was a lot better then, compared to the tech-bubble burst.

Now, in the aftermath of the financial crisis, the BoE’s 550 bps policy rate cuts have since amplified the dislocation of equity vs bond yields. As earnings of UK equities recovered, though not keeping up with share price performance, the subsequent re-rating of UK equities has paled in comparison to the bubble unfolding in UK bond markets. Having now reached another critical juncture in Brexit, and with BoE QE in place for at least the next eighteen months (the initial horizon for corporate bond purchases, with additional gilt purchases taking place over the coming six months) BoE stimulus will likely drive this yield disparity wider once again.

Risk-Adjusted, UK Equities Are Already More Attractive Than Bonds

What if bond yields have fallen so low that compared to the volatility incurred, dividend paying stocks are already more attractive?

Since the financial crisis ended, the dividend yields of the broader UK equity market have consistently exceeded the risk-free rate[1], while shifts in the yield curve moved long-dated gilt yields both into premia and discount to the risk-free rate. On a standalone basis, the yield premium argument is not complete. There is no free lunch since higher yield premia is often accompanied by higher volatility. Hence, when longer-dated bonds offer a premium to the risk-free rate, the right comparison to make against the equity yield premium is to adjust both yield premia for volatility.

By comparing the redemption yields of UK gilts and dividend yields (12M trailing) of UK equities respectively against their total return volatility, we can get a sense of how much risk investors incur for the (distributed) income earned. Chart 2 encapsulates the growing divergence taking place whereby UK gilts are offering increasingly negative risk-adjusted yields compared to risk-adjusted dividend yields for investors with a medium-term investment horizon[2].

For UK bonds, while regarded as safe to compensate for lower yields, when compared to higher short term interest rates today, the term risk incurred as a result of holding longer-dated bonds is in fact a drag for investors. The meagre gilt yields on offer do not sufficiently compensate for the additional risk incurred versus cash and since the recently announced BoE QE stimulus, this is set to worsen. As seen in the chart, the risk-adjusted yield premium for equities is significantly above the now negative risk-adjusted yields for bonds. If incurring term risk in fixed income all but loses its justification, the investment decision for investors to make, even for medium-term investment horizons, is to either hold cash and earn no yield, or hold equities that offer higher risk-adjusted yields than high grade UK bonds.

WisdomTree’s Smart Beta Solution: Higher Yield Without Compromising Volatility

Equity price appreciation can no longer be counted on as a key driver of total returns amidst ongoing concerns of slowing global economic growth and sub-standard earnings performance. Under such market conditions, dividend payers offer a defensive response, potentially forcing insurance and pension funds which are being crowded out by BoE’s corporate QE to allocate more into UK dividend payers.

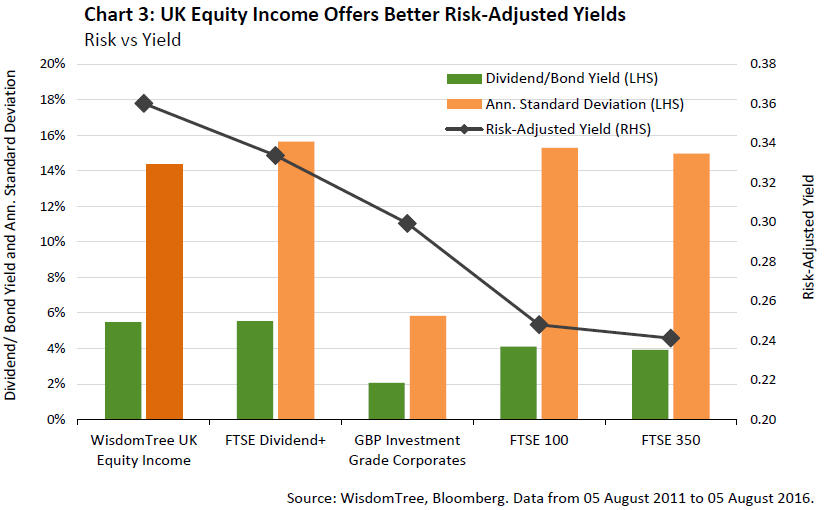

Equity income strategies in particular may offer investors an efficient, low volatility solutionto satisfying income needs. Such strategies incorporate rules-based dividend screens, typically by dividend yield, in the stock selection process to create broad diversified baskets of dividend payers only. Chart 3 highlights the significant yield premium on offer, with the WisdomTree UK Equity Income Index offering a 5.5% dividend yield - a sizeable premium of 350 bps compared to GBP investment grade corporates, and up to 160 bps more additional yield relative to broad UK equity peers such as the FTSE 250.

In fact, WisdomTree’s UK Equity Income Index actually offers the lowest volatility in equities at 14.4%, reflecting the quality tilt introduced to the basket through weighting stocks by total cash dividends paid. In so doing, the annual rebalance rewards dividend growers more so than share price performance, ultimately working as a mechanism to manage valuation risk. With a 46% allocation to mid- and small-caps, an overweight relative to other broad UK equity benchmarks, the apparent diversification benefits reaped by WisdomTree’s methodology offers another means of keeping volatility contained.

Exceptional BoE stimulus is not likely to go away anytime soon. Income seeking investors need to be mindful of a prolonged period of yield deprivation in traditional fixed income assets. Risk-adjusted, equities may offer better solutions.

Investors sharing this sentiment may consider the following UCITS ETFs:+ WisdomTree UK Equity Income UCITS ETF (WUKD)

All data is sourced from WisdomTree and Bloomberg, unless otherwise stated.

[1] 3M Libor assumed as risk-free rate for investors

[2] 3 year holding period assumed as a base scenario to compare risk-adjusted yields that investors earn in bond and equity markets