OPEC signals it is ready to start increasing supply

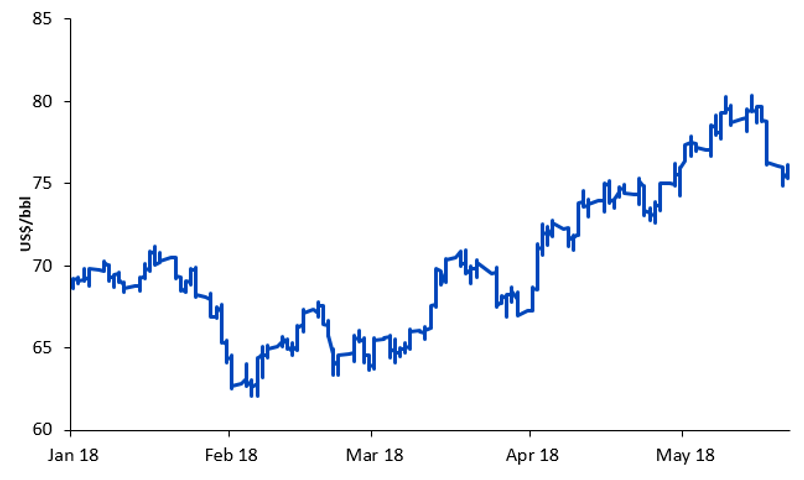

Brent oil price is retreating after rising over US$80/bbl on 22 May 2018. Hitting that psychological barrier has triggered a question across the market: has the Organization of Petroleum Producing Countries (OPEC) overdone it with their supply curbs? Their strategy to reduce global inventories was successful, but is it now time for the cartel to reap the rewards before the US eats away at the group’s market share? Oil prices fell sharply after a meeting between Saudi Arabia and Russia on 25 May confirmed that easing the curbs on production is being discussed.

Figure 1: Brent oil price

Source: Bloomberg, WisdomTree, data available as of close 30 May 2018, hourly data.

Past performance is not indicative of future results. You cannot invest directly in an Index.

After oil prices hit US$80/bbl, OPEC and its non-OPEC partners have been forced to re-think their strategy. Oil prices had spiked in May 2018 as Venezuelan production continued to decline and the threat of US extraterritorial sanctions on Iran – however detested by its trading partners – is widely expected by the market to tighten oil supplies. Back in 2014, OPEC increased production to take market share from what they thought were high-cost producers like the US. A reversion back to managing global output in 2017, has re-introduced the same problem they faced in 2014: OPEC is losing market share and thus losing out on oil revenues.

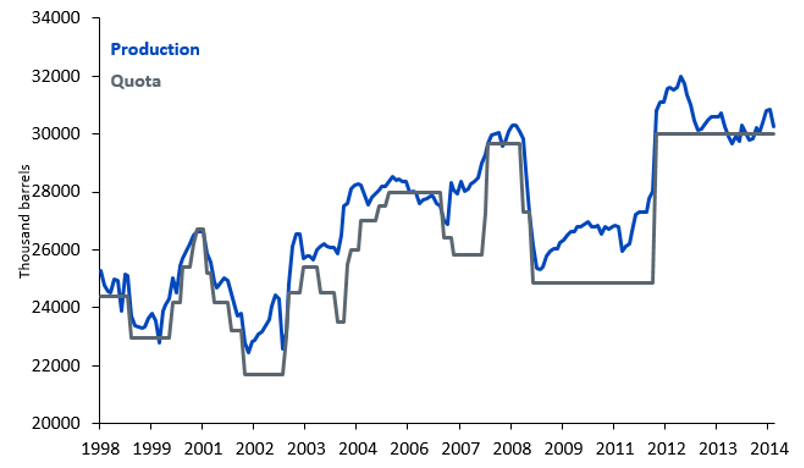

For the 14-member cartel and 10 other countries to agree on a programme to curb production with such a strong level of compliance was an achievement. OPEC historically has been poor at adherence, although a large part of the ‘over-achievement’ this time is due to Venezuela’s economic implosion. Saudi Arabia and Russia now feel the pressure to make up for the shortfall that Venezuela and Iran are likely to leave behind.

Figure 2: OPEC adherence to quota pre-2014 was patchy

Source: Bloomberg, WisdomTree, data available as of close 30 May 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

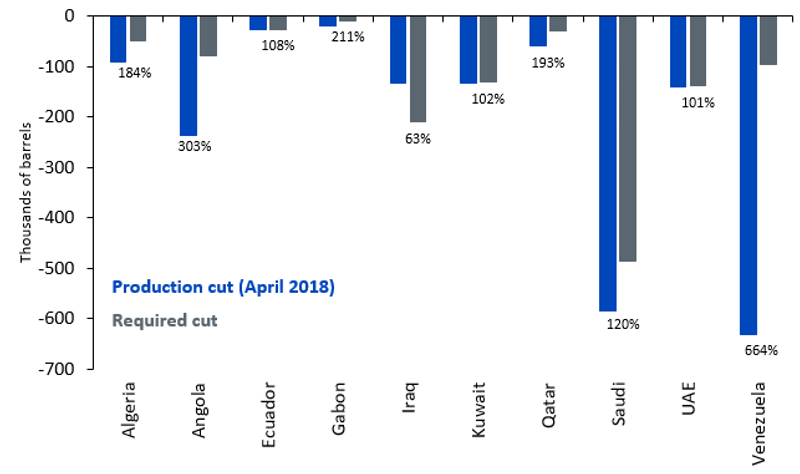

Figure 3: Compliance in current deal

Source: OPEC (Based on secondary communication), WisdomTree, data available as of close 30 May 2018. Label highlights the compliance level in percentage against agreed cuts in November 2016.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Of course, OPEC member nations are not going to do this for pure altruistic market balance reasons. Many OPEC nations experienced an economic slowdown in 2017 and will rely on higher oil revenues to help them stage a recovery this year and next. For those countries able to increase volumes, that will be an easier way for them to boost revenues compared to waiting for further price increases.

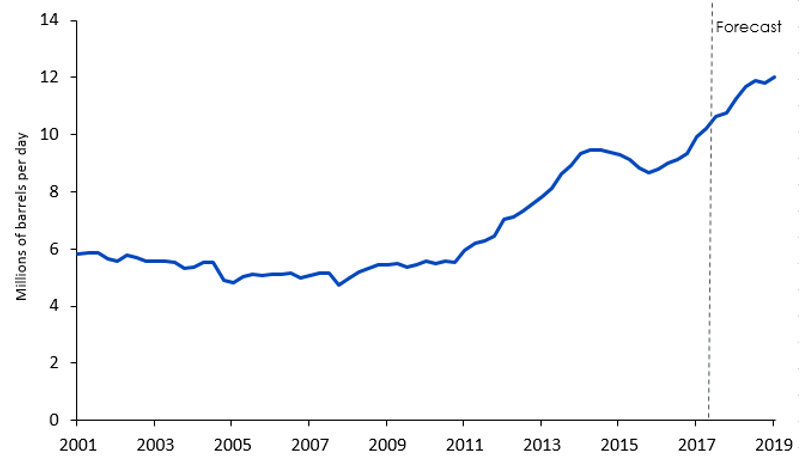

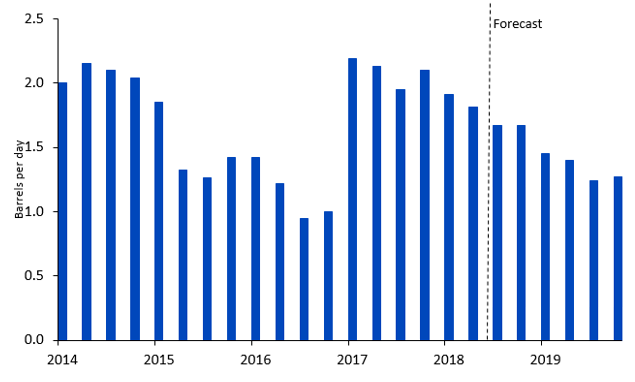

Given that the US is expected to increase production by 1.4mn barrels per day this year (source: US Energy Information Agency), compared to a 0.5mn barrel per day increase last year, OPEC needs to seize the moment and absorb the market share, before the US ramps up production so much that it crowds out OPEC oil.

Figure 4: US oil production forecast

Source: EIA, WisdomTree, data available as of close 30 May 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

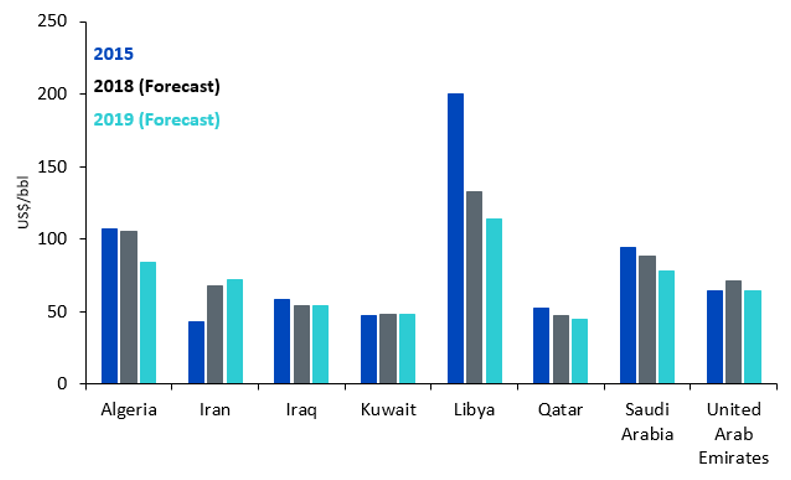

While many think that OPEC would like the era of high oil prices to continue, citing the so-called fiscal break evens – the price of oil required for the government’s revenue to match their spending obligations – we note that for many countries the current price of oil is above these break even rates (including Iran, Iraq, Kuwait, Qatar and United Arab Emirates). Many OPEC nations have survived with oil prices significantly below fiscal break-evens for many years. In fact, the era of lower oil prices from 2014-2017, allowed these countries to engage in a belt-tightening exercise, reducing consumer petro-product subsidies for example and sharpened their focus on diversifying their economies. Saudi Arabia, under the lead of Mohammad bin Salman bin Abdulaziz Al Saud (MbS), has developed “Vision 2030” – economic reform focused on restructuring and diversifying the economy.

Figure 5: Fiscal Break-evens

Source: IMF, WisdomTree, data available as of close 30 May 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Many believed that Saudi Arabia would like higher oil prices to meet the target valuation of Saudi Aramco (the government announced a valuation of US$2trn) prior to its IPO. But as far as we can tell, the international IPO is on ice with the domestic IPO delayed to 2019 at the earliest on the local Saudi Arabia’s Tadawul exchange and virtually no preparedness for a simultaneous or sequential flotation on a foreign exchange. The Saudi officials have not even decided whether they would prefer a London or New York flotation. Propping up oil prices for this event can no longer be a chief driver of Saudi-OPEC strategy.

Saudi Arabia, the de-facto OPEC leader and Russia, the largest non-OPEC partner in the production curb programme were in discussions last weekend and floated the idea of raising production by 1mn barrels per day. With total OPEC spare capacity around 2 million barrels, we could see further increase in production when the group meet to discuss policy on 22 June.

Figure 6: OPEC Spare Capacity

Source: EIA, WisdomTree, data available as of close 30 May 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Related blogs

+ Sanctions will not kill Iranian oil exports but will keep geopolitical premium high