Gold could rise to over US$1800/oz if geopolitical risks remain elevated

Gold prices have moved very quickly in the past two months, gaining 14% in that short space of time. Gold’s gains have been consistent with the sudden drop in Treasury yields and rise in demand for safe haven assets. As we highlighted in The gold market reigns supreme, growing tensions between the US and China in the form of both a trade and a currency war have kept the market on edge, thus driving up the demand for safe haven assets. Both the market and the Trump administration appear to have forced the Federal Reserve’s (Fed) hands to ease policy. Market tantrums clearly have influenced Fed’s decision making, with the central bank changing policy course after equity markets faltered earlier this year. The Trump administration’s flip-flopping on the trade front, has also led the Fed to provide an “insurance” rate cut. Fed fund futures indicate that the market expects more rate cuts to come during the course of the year and that is likely to keep US Treasury yields low.

Clearly the outlook for the economy, interest rates and exchange rates have changed since we published our gold outlook last month. Here we provide an updated outlook and focus on a scenario in which geopolitical and financial market uncertainty remains elevated.

Base case forecast

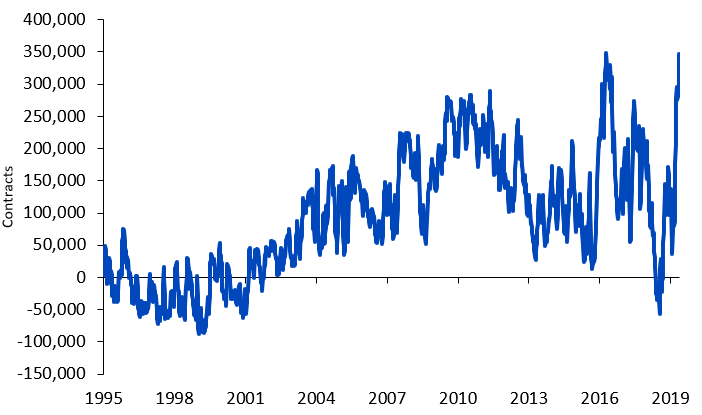

Our new base case forecast is for gold prices to rise to US$1550/oz in Q2 2020, up from US$1500/oz in mid-August 2019. This forecast is based on US 10-year Treasury yields and the US dollar basket holding around current levels at 1.65% and 97 respectively. We expect inflation to hover around 1.8%. While we don’t think that there are immediate negative price pressures on the horizon, inflation any higher than this level would be inconsistent with the Fed cutting rates. Currently speculative positioning in the gold futures market is very elevated at 346k contracts net long according to data from the Commodity Futures Trading Commission (CFTC). That is just a fraction below the all-time high set in July 2016 at 348k contracts net long. Market sentiment toward gold has shifted very quickly in a short space of time. In November 2018, sentiment towards the metal was so weak that speculative positioning was net short. As we have never seen positioning remain as high as it is today for a long stretch of time, in our base case forecast we bring positioning down to a more sober 120k contracts net long.

Figure 1: Gold Price Forecast

Source: WisdomTree Model Forecasts, Bloomberg Historical Data, data available as of close 13 August 2019.

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

What if speculative positioning remains elevated?

Being conservative in our base case, we reduce speculative positioning to something closer to the long-term average, but what if speculative positioning remains as high as it is today until Q2 2020 (i.e. at 346k contracts net long)? Our model indicates that would drive gold prices to close to US$1815/oz.

Figure 2: Gold futures speculative positioning

Source: Bloomberg, WisdomTree, data as of 13 August 2019.

Estimates are not a reliable indicator of future performance and any investments are subject to risks and uncertainties

There are a number of geopolitical and financial risks that have driven positioning in gold futures to elevated levels:

- Trade negotiations between the US and China reaching a stalemate, increasing the probability of greater protectionism between the two economic superpowers

- Market fears that the Fed is committing a policy mistake by loosening policy when labour markets are tight, and inflation is not falling

- The probability of a hard Brexit rising under a new Prime Minister in the UK

- Tension in the Middle East rising as Iran continues to enrich uranium above the levels permitted under the nuclear accord. Attacks on vessels moving around the Strait of Hormuz – through which a third of the world’s seaborne oil passes – have added to tensions in the region after the Trump administration has applied punitive sanctions on Tehran

- The Argentine economy and equity/bond market falling back into a crisis, sparking fears of a broader emerging market sell-off

- Political uncertainty resurfacing in Italy as a vote of confidence is being put forward against the sitting Prime Minister

- Political unrest in Hong Kong as opposition to an extradition bill - that would allow criminal suspects to be tried in mainland China – has triggered demands for broader democratic reform

While many of these issues could be resolved quickly, there is a strong chance that they are not. For example, trade discussions between the US and China have been ongoing for more than two years without a clear resolution as the expectations from both sides appear so far apart. It is not clear what will be the catalyst to bring the two sides closer. Brexit equally looks like an intractable problem with the terms of the deal negotiated by the previous prime minister unacceptable to current government and the European Union unwilling to negotiate on the key stumbling blocks.

With Iran looking like it is politically isolated, the chances of the country continuing to rattle sabres appears higher than it capitulating to US demands.

Should geopolitical concerns deteriorate further, speculative positioning could rise even more. If positioning were to rise to 400k contracts net long, our model indicates gold prices could rise to US$1875/oz – a whisker away from the all-time high gold price of US$1900/oz set on 5 September 2011.

Related blogs