OPEC: Short Term Gain, Long Term (continued) Pain?

It’s coming down the wire. The upcoming OPEC Vienna meeting this week may represent yet another change to the status quo for 2016, with the cartel possibly cementing its first production cut in eight years and complete a dramatic shift in strategy. We believe that whilst this may present short-term tactical opportunities for oil investors, long-term positioning remains a challenge.

A Much Needed Change of Strategy

From an economic perspective, a supply cut is justified given how current strategy has been ineffective at best, and self-defeating at worst. OPEC’s response of ramping up production to counter the threat of US shale oil has not only depressed oil prices but severely dented the public finances of oil producing nations.

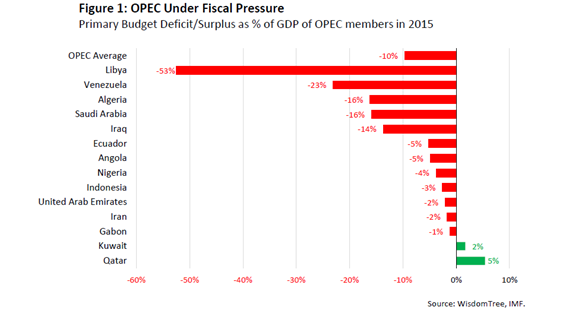

Figure 1 highlights the fiscal damage brought about by collapsing oil prices with Saudi Arabia, the world’s largest oil producer, of particular concern having run up a budget deficit of 16% of GDP in 2015. With oil prices having flatlined for much of 2016, continued weakness in the Kingdom’s finances raises serious concerns about its ability to maintain generous defence spending and combat the growing geopolitical instability in the region. Alongside this is an endemic youth unemployment crisis (nearly 30% of 16-29 year olds are unemployed) that remains unaddressed, and which could pave the way for rising social unrest if not tackled in due course. These issues, though unique to Saudi Arabia, represent just a handful of growing problems plaguing OPEC members, all of which have stemmed from weak oil prices.

Against this backdrop, it is little wonder why OPEC members, along with Russia, have seemingly brushed aside longstanding conflicts in favour of a more accommodating stance.

Perhaps a stronger rationale for a binding agreement being reached however, if not for economic sense, lies in the interests of self-preservation. OPEC has suffered a slow demise at the hands of the US shale industry, a fate that has been compounded by infighting and ineffective policy making. As its influence on global oil markets has waned, many are calling into question its continued relevance and purpose in the current climate of subdued oil prices. To avoid being consigned to the depths of history, OPEC needs to find a renewed sense of purpose and strike a deal that will remind markets that it maintains the ability and willingness to dictate the path of oil prices.

A Long Term Oil Price Rally Looks Unlikely

Following the unexpected announcements at Algiers, markets are hotly anticipating Vienna to be a success with many investors having revised up oil price expectations. Although a deal appears imminent at this point in time, we believe that widespread optimism on a sustained oil price rally is simply unrealistic considering the key obstacles outlined below.

Arguably the biggest stumbling block to higher oil prices longer term lies with the willingness of Iran and Iraq to adhere to any supply cut agreements. Iran, looking to reclaim lost market share following years of trade embargoes and isolation, and Iraq, heavily reliant on oil revenues to fund its fight against ISIS, maintain strong incentives to defer from production cuts.

Unless concessions are offered, Iran and Iraq will continue to avoid committing to any deals, undermining negotiation efforts and signaling a return to the status quo of high output, low prices and continued fiscal pain. At the same time, any concessions offered will not only blunt the effectiveness of a supply cut, since the two are the second and third largest oil producers within the bloc, but also set a dangerous precedent that could encourage other OPEC members to cheat. Therefore, the immediate success of any agreement hinges upon an amicable solution emerging.

The threat of US shale oil also represents another major source of uncertainty. With OPEC production levels at record highs of 34 mb/day, and having climbed higher since the last meeting, any meaningful impact on prices will require substantial output cuts. Of course, any supply void left by OPEC will likely encourage nimbler US shale oil producers to start pumping again; their efficient production techniques enabling them to produce at much lower costs. According to Figure 2, whereby the WTI spot price has been overlaid against Baker Hughes’ rig count, US oil rigs take approximately four months to adjust to higher (or lower) oil prices. This implies that any supply cut will only provide a temporary boost to prices, before attracting other producers to commence operations again and limiting OPEC’s advantage from higher prices.

The final threat lies with Trump and his push to secure US energy independence, a move that is likely to entail opening up federal land for oil and gas production, coupled with greater infrastructure spending. This could see domestic production being ramped up significantly over the coming years and place further pressure on oil prices. Although no concrete plans are in place as yet, oil investors will undoubtedly be keeping a keen eye out for upcoming policy clues.

Implications for Oil Investors

The balance in oil markets remains delicate with global demand still lackluster and not expected to accelerate in the near future. Pricing pressures will continue to be driven largely by supply side dynamics, with the Vienna meeting potentially playing a significant part in correcting the persistent supply glut. However, investors should consider the risks of any agreement being derailed and calibrate oil price expectations accordingly.