A Premium Yield For Less Credit Risk in Emerging Markets: High-Yielding Dividend Payers Trump High-Grade Bonds

If you’re in the hunt for yield, you’ll know that Emerging Markets (EM) are once again, fair game. The restructuring of corporate balance sheets, stabilising commodity and currency markets coupled with receding investor concerns on China, all make EM an attractive prospect.

We also believe that central banks’ high-grade bond buying programmes deprive investors of yield unless significantly more term and credit risk is assumed. Therefore, equity income rather than fixed income should be the strategy for Emerging Markets.

A simple, efficient equity income strategy comprising of a stock basket of high dividend yielders that is broad and all-inclusive provides higher yield with less financial leverage than High-Grade bonds.

For example, WisdomTree’s EM Equity Income UCITS ETF (DEM) [1] are favoured because:

+ Prospective dividend yields (12M forward) are at a premium to redemption yields of EM high-grade EM corporate bonds, overall.

+ Indebtedness (Net Debt to EBITDA) of non-financial companies is lower for than for EM High-Grade corporate bonds, overall.

Two drivers explain the premium in yield and discount in leverage

+ With a low overlap of parent companies’ issuing equity and debt, we estimate DEM constituents reflect less than one third of an EM High-Grade corporate bond universe. Quasi government issuers are over-represented in EM, but typically don’t pay dividends.

+ Our selection is based on all-inclusiveness, to get the broadest set of new and old dividend payers. The 30% of highest yielding stocks will range from large-cap energy, miners and banks, to small-cap consumer and tech.

Crowding out of High-Grade bonds reinforces the premium of dividend payers

If ultra-loose monetary stimulus is here to stay, as Fed Chairman Janet Yellen also acknowledged at the Jackson Hole’s summit at the end of August, the descent of high grade Developed Markets (DM) corporate and sovereign bond yields should continue to be relentless.

In this context, central banks such as the ECB, BoJ and recently now too the BoE, have begun to crowd out the credit market for long dated fixed income, depriving in particular, institutional investors of corporate bonds not yet caught in zero/sub-zero yield territory. To limit the damage inflicted to final salary schemes and life insurance policies as they grapple with rising funding shortfalls, institutional investors will be forced to venture into riskier fixed income (eg borderline and sub-investment grade in DM to riskier EM sovereigns and corporates) to get whatever yield above zero remains and for long as QE programmes endure.

The desperate hunt for yield catching up to riskier EM credit is evident from the benign impact the sharp downturn of commodity markets and EM currencies had last year to EM bonds: sharp losses were inflicted on EM equities as a result of energy and base metals prices slumping, with the MSCI EM (USD) Index falling 34% from peak to trough in the period of 2015 to date. While it has rebounded sharply this year, since 2015, the MSCI EM is still down by 2.5%. This is in contrast to EM High-Grade corporate bonds, with the Bloomberg EM USD Investment Grade Bond Index up 9% over the same period. The continuation of last year’s sell off in crude oil into January this year hit EM equities anew, yet EM bonds barely budged as yields of dollar denominated issues continue to trend down.

Amidst the artificial support for High-Grade bonds, the heavily discounted share prices have created a yield premium favouring high dividend yielding equities over High-Grade bonds. As Chart 1 shows, the WisdomTree Emerging Markets Equity Income Index, which comprises the 30% highest dividend yielding stocks in EM, has approximately a 5% dividend yield (TTM) [2], which is about 2% more than the redemption yield of the Bloomberg EM USD Investment Grade Corporate Bond Index. The widening of this yield premium since 2010 is a marked difference from when EM bonds and equities reacted with similar magnitude when commodities crashed in the financial crisis and is a reversal from the years prior, when High Grade bonds yielded more than dividend payers.

EM restructuring efforts put credit at risk too

There remains plenty of risks lurking within EM bonds, not least given the pessimism of rating agencies to corporate credit issuers in China, where, according to the Bank of International Settlements, outstanding debt of non-financial corporations has ballooned to 163% of GDP. High indebtedness has triggered a surge in the number of downgrades to company credit ratings in Q2 2016 by likes of S&P, Moody’s and Fitch which, both in absolute terms as well as relative to the number of upgrades, have reached 2008-2009 financial crisis levels. In Q3 2016, that trend has started to reverse as signs emerge of companies have started to restructure and deleverage their balance sheets.

This initially ends up taxing for equity investors. Some high-profile EM companies this year have effectively called on shareholders’s bail out bondholders, seeing their equity share diluted or heavily discounted by rights issues, as well seeing their asset base shrink.

+ ArcelorMittal bought back $2.7 billion in USD and EUR denominated bonds through a $3 billion rights issue, which along with scrapping its dividend, divestitures and cost savings aimed to cut its $16 billion debt pile.

+ Brazil’s iron ore miner Vale SA, which has twice this year tapped the bond market to refinance maturing debt and after scrapping the 2016 dividend, is planning to raise $10 billion from asset sales to bring down its $27.5 billion of net debt load by around a third over the next 18 months, saying there is no cash for expansion, only debt repayments.

However, credit investors are not immune to restructuring. When the debt load proves too much for equity investors to bear, debt writedowns, such as cuts to interest and principle as well as rescheduling all eat into a bond’s Net Present Value.

+ China has recently enforced debt restructuring to the steel and coal industry which struggles from overcapacity and inefficiencies, by forcing banks to renegotiate loans on better terms and conditions. An alternative to what effectively amounts to a writedown, the government could force banks to swap the loans for riskier corporate bonds, or in the worse-case, equity.

This begs the question: amidst signs of corporate restructuring taking hold on major EM companies can EM dividend payers offer a better alternative to EM corporate bonds?

More yield for less leverage: high dividend yielders vs High-Grade EM corporates

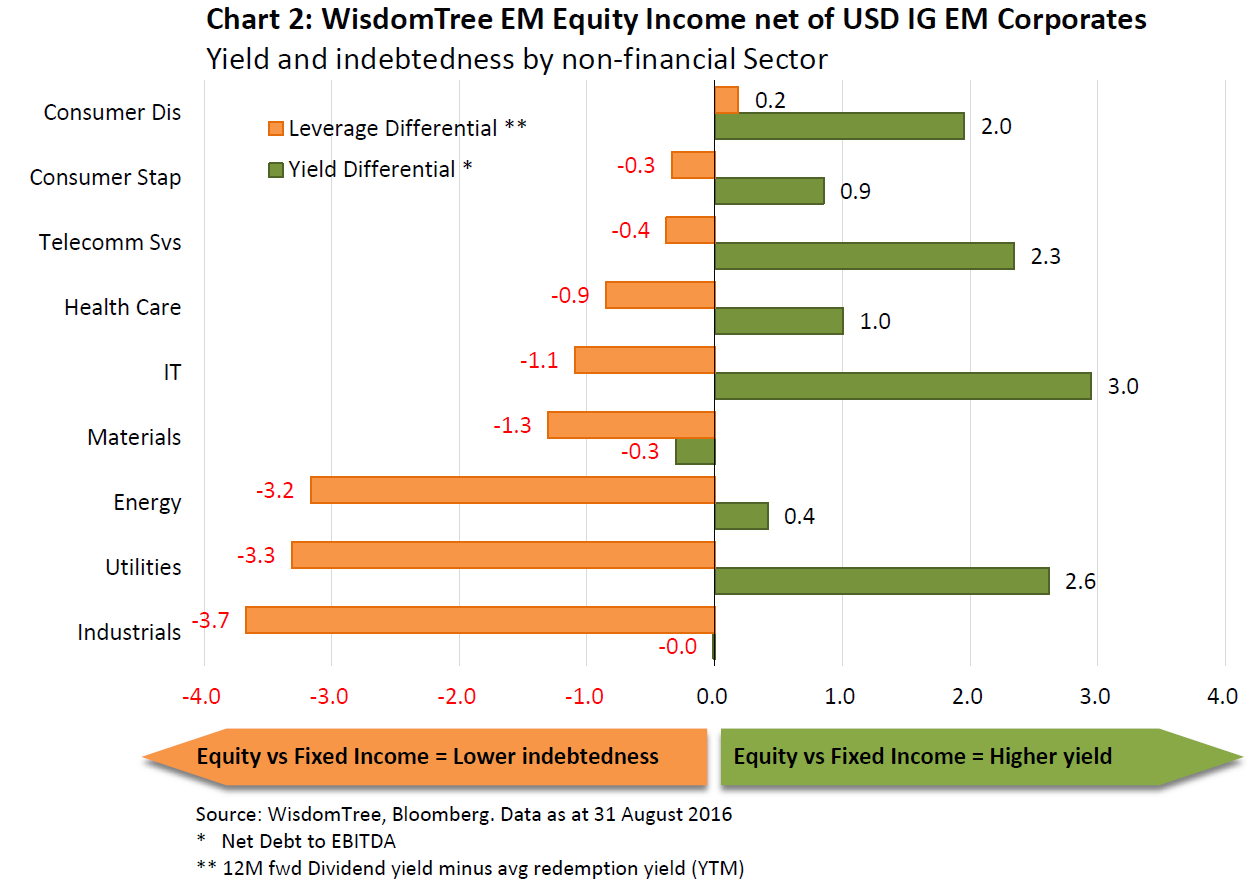

Many of the high dividend yielding stocks currently offer prospective dividends that are at a premium to redemption yields on High-Grade corporate bonds. For example, Chart 2 below shows how the degree of financial leverage (i.e. indebtedness) and the dividend yield of stocks in the WisdomTree Emerging Markets Equity Income Index compare to EM corporate issuers of Investment-Grade USD denominated bonds [3]. Chart 2 shows that for non-financial sectors [4] on average, WisdomTree Emerging Market Equity Income strategy (ticker=DEM) has, relative to the High-Grade EM corporate bond universe:

+ lower financial leverage (i.e. lower Net Debt to EBITDA, as indicated by the orange bars)

+ higher yields (i.e. 12-month forward dividend yield exceed redemption yields, as shown by the green bars)

The strong presence of quasi-government companies such as PEMEX (Mexico), ECOPETROL (Columbia), ENAP (Chile), Codelco (Chile), PTT (Thailand) and CNOOC (China), distort the picture of comparing yield and credit metrics between EM equities and EM bonds. While quasi government debt securities enjoy significant weight in the EM corporate bond universe given their large issuance of wide-ranging types of debt securities, many don’t issue stock and pay dividends, hence their representation in EM equities is markedly reduced. Based on our own research, we estimate that the universe of High-Grade corporate bonds represent less than one third of the basket of WisdomTree’s Emerging Markets Equity Income UCITS ETF.

To reduce the skew of leverage and yield towards quasi-government companies and give pure private-sector issuers a bigger part in EM equity and bond universes alike, simple averages – rather than weights-adjusted averages – will give in our view a fairer, less distorted representation of the financial leverage and hence credit risk assumed and yields demanded by investors.

All-inclusiveness in high-dividend yield screen captures new economy stocks

As demonstrated in Chart 2, the lower financial leverage and/or higher yield premium is generally observed across non-financial sectors in WisdomTree Emerging Markets Equity Income Index. Importantly, the leverage in the commodity-driven sectors such as Materials and Energy in the WisdomTree Emerging Markets Equity Income Index, which at 2.5x and 1.6x Net Debt to EBITDA, respectively, is significantly lower than the leverage of 3.8x and 5x Net Debt to EBITDA of High-Grade corporate bond issuers.

IT stocks on average offer dividend yields of 6%, many of which have such liquid balance sheets that cash balances more than cover debt. Allocations[5] into IT (12.6%), Consumer Discretionary (5.4%), Consumer Staples (1.3%), Healthcare (0.3%), and Telecoms (13.1%) drive the new economy in EM, and approximately one third of the WisdomTree Emerging Markets Equity Income Index has exposure to these sectors, making it not just a deeper value/yield proposition compared to High-Grade EM corporate bonds, but also a secular growth strategy. It should therefore come as no surprise that Taiwan (23%) and China (21%) comprise 44% of the basket.

The yield premium vs leverage discount of WisdomTree’s EM high dividend yielders lies inherently in its screening and selection methodology, which creates a dividend payer universe where the emphasis is on both high yields and all-inclusiveness: screening for the top 30% of highest dividend yielders which have paid cash dividends for the last 12 months or longer. Through it, exposure to the established multinationals operating in traditional dividend paying sectors such as banks, energy and utilities is reduced, to include into the basket maturing technology, healthcare and consumer stocks, alongside mid- and small-cap stocks.

Our screening of High Grade corporate bond issuers in Emerging Markets shows that the basket of WisdomTree’s Emerging Markets Equity Income strategy includes a relative unique list of dividend paying companies: less than one third of its weight are companies whose debt securities are part of the High Grade EM corporate bond universe, making the basket for the majority (ie two thirds) distinct to the universe of EM High-Grade corporate bonds.

The deep discount of high dividend yielders assessed against credit metrics and compared to EM corporate credit suggests that many high dividend yielders now offer a better yield proposition. A dividend focused strategy where high yielders and all-inclusiveness are combined in one ETF offer investors a targeted approach to extract maximum value out of Emerging Markets today.

Sources

[1] Dividend yields and Net Debt to EBITDA are as of 31 August 2016:

[2] Trailing twelve months

[3] Based on WisdomTree research for screening the emerging markets corporate bond universe, using the Bloomberg USD Investment Grade EM Corporate Debt Index as a proxy for high grade corporate EM issuers.

[4] Net Debt To EBITDA is not a meaningful leverage metric for banks and insurance companies as customers’ and investors’ funds are typically aggregated in liabilities, thereby inflating the leverage metrics

[5] Sector allocations refer to 31 August 2016