Defensive Assets: The duration your portfolio needs

This blog is the third instalment of our new blog series on Defensive Assets: ‘Offence wins games but defence wins championships’.

The previous instalment of this blog series focused on defensive equity strategies and highlighted how quality or multi-factor exposure could provide useful tools to navigate the current uncertainty in global markets. This week, we will focus on local currency fixed income i.e. fixed income assets denominated in the home currency of the investor. For the purpose of this blog, we look at euro assets for euro-based investors, but our main findings support other currencies like US dollar-denominated assets for US dollar investors, for example. After reading this blog, we hope to provide investors with greater insight into some of the advantages and drawbacks of the different fixed income assets when trying to protect a portfolio against equity risk, highlighting the diversifying power of longer duration investments and the potential risk of an uncontrolled flight to quality.

Using the defensive framework we unveiled in the first blog of this series, which revolves around the following 4 main characteristics, risk reduction, versatility and asymmetry of returns, diversification and valuation, we will aim to highlight which assets strike the right balance between a defensive profile that protects a multi asset portfolio against equity downside and a reasonable upside potential to navigate uncertain periods and late cycle rallies.

Fixed Income: The poster child for defensive assets

Historically, the natural starting point for a multi asset portfolio has been a 60%/40% asset mix (60% in equities and 40% in fixed income). This mix aims to provide exposure to the historically superior returns exhibited by equities, meanwhile also granting the diversification benefits available in fixed income assets. Within this framework, fixed income assets are considered the ultimate defensive assets providing some cushioning in the event of an equity downturn, partly due to their lower volatility but, more importantly, thanks to their negative correlation to equity returns.

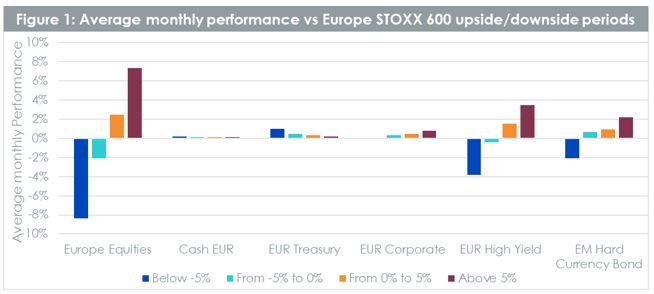

In Figure 1, we consider the average monthly performance of various fixed income assets (left axis) during different equity market regimes using the Europe STOXX 600 as a reference. The average returns of each asset during the 2 regimes where equities perform negatively, as illustrated by the two blue bars, (European equity markets (i) losing more than 5% in a given month or (ii) losing between 0% and 5%) give us some insight on the risk reduction proprieties of the asset. The average returns of each asset during the 2 regimes where equities perform positively can inform us on the asymmetry of their profile and their capacity to perform well in good times.

Source: WisdomTree, Bloomberg. Period July 2000 to December 2019. Calculations are based on monthly returns in EUR.

Historical performance is not an indication of future performance and any investments may go down in value.

Looking at the results on the risk reduction side, we can note that cash and government bonds deliver on their promise with positive returns in both negative regimes for equity. It is worth mentioning as well that Eurozone government bonds do not just cut drawdowns like cash but in fact also create positive uplift. However, as the credit risk increases within a fixed income asset, the risk reduction tends to disappear. In fact, over the last two decades, high yield bonds and emerging market bonds behaved more similarly to equities.

Focusing on the other side of the equation, with the performance in regimes where equities are doing well, the higher the credit risk of the fixed income asset, the better the performance. Cash highlights perfectly the pitfalls of focusing solely on risk reduction. Even if it does very well as an asset in the drawdown scenarios, it also does not benefit from the strong price appreciation that other bonds tend to exhibit during better economic times and therefore it cannot be considered as a medium to long term investment.

Long duration government bonds, a balanced choice between risk reduction and upside potential

In Figure 2, we take a deeper dive into government bonds and assess the impact of duration and ratings on their performance profile. On the risk reduction side, the higher the credit rating of the asset, the higher the performance in an equity downturn (see EUR Treasury AAA). This is partially driven by investor behaviour and their tendency to allocate money to non-risky, safe-haven assets in times of crisis (such as German bunds or US treasuries). But interestingly enough, in times when equities dropped in price, history has shown that lengthening duration was the most beneficial lever to pull—even doing better than increasing credit quality (see EUR Treasury 15+ vs EUR Treasury 1-3). Such long duration assets show greater sensitivity to changes in interest rates in scenarios where equity prices fall and bond prices rise (bond yield falls).

.jpg?sc_lang=fr-lu&hash=7C722E4B7DE3AC0E782A5034FFDB3DC4)

Source: WisdomTree, Bloomberg. Period July 2000 to December 2019. Calculations are based on daily returns in EUR.

Historical performance is not an indication of future performance and any investments may go down in value.

In the other two regimes, increasing the credit rating of the fixed income assets deteriorate significantly the performance. Like cash, AAA government bonds exhibit a very strong performance drag in any market scenario outside of equity crashes, creating a large opportunity cost on the money invested.

The effect of changing the duration, on the other hand, seems to vary depending on the credit rating. For AAA treasury, increasing the duration magnifies the underperformance in regimes where equities performed positively. For lower quality bonds such as Italy treasuries (rated A-/BBB), increasing the duration improves the performance. In fact, long duration Eurozone government bonds (average rating AA-/A+) deliver strong outperformance in equity drawdowns thanks to their negative correlation to equities and higher volatility profile but delivers a strong performance also in other regimes.

In conclusion, by aiming for government bonds with average credit quality and high duration (see EUR Treasury 5-7 or 15+) it is possible to get better risk reduction than cash, German bunds or EUR Treasury meanwhile participate in the upside performance potential that is close or on par with EUR corporates.

In Figure 3, we can observe that in line with previous findings, treasuries and more particularly higher rated treasuries exhibit strongly negative correlation to equities while corporate bonds and high yield bonds show a high positive level of correlation. Focusing on correlation during equity drawdowns only, we observe that higher volatility such as longer duration assets or corporate bonds seem to benefit strongly with correlation falling significantly more than for other types of assets.

.jpg?sc_lang=fr-lu&hash=78CA93212339F51A4BE74FB1889F5103)

Source: WisdomTree, Bloomberg. Period July 2000 to December 2019. Calculations are based on monthly returns in EUR.

Historical performance is not an indication of future performance and any investments may go down in value.

Once the asset allocation mix which best suits an investors risk profile has been selected, the implementation process requires strong consideration. Fixed income is such a sprawling asset class that there are an infinite number of ways to invest in a given segment. Linking ourselves back to our framework, the objective is to extract the asset class behaviour we are looking for, meanwhile, considering asset class valuations (i.e. to improve the yield we can extract from the underlying assets). WisdomTree’s view is that by using systematic strategies, it is possible to enhance the income potential of a fixed income segment, such as treasuries or aggregates, by sourcing opportunities and shifting exposures across countries and duration buckets within that segment to increase yield and therefore improve the long term outcome of such a portfolio. In particular, using a treasury focused enhanced yield strategy, which exhibits on average higher yield and slightly higher duration than traditional benchmarks, it is possible to improve the performance in good economic scenarios while delivering the same defensiveness in downturns.

Next week, we will continue our tribulations in the different asset classes and search to our expanding collection of defensive assets focusing on Currencies.

Related blogs

+ Defensive Assets: Is playing too safe too risky?

+ Defensive Assets: Are all equity strategies created equal?