Die wichtigsten Erkenntnisse

- Nvidia’s strong earnings exceeded expectations, but the stock fell as investors recalibrated their expectations given its high valuation

- AI-driven growth in semiconductors is significant, but raises concerns about sustainability due to the industry’s cyclical nature

- The broader semiconductor ecosystem is vital for AI’s growth, but diversifying investments across the AI value chain more broadly, particularly in unloved areas of software, could capture long-term growth potential

Nvidia recently reported its earnings, showcasing strong performance, but it failed to meet the market's high expectations. Despite beating analyst forecasts, the stock faced a sharp sell-off as investors reassessed the company's future growth prospects.

Earnings Reaction

Nvidia posted impressive quarterly results, with revenue reaching $30 billion, surpassing the consensus estimate of $28.8 billion1. The data center segment was particularly strong, contributing to the majority, at $26.2 billion1. Looking ahead, Nvidia provided Q3 guidance with revenue expected to reach $32.5 billion1, aligning with analyst expectations and on track for over $120 billion in revenue for 20242.

Figure 1: Nvidia’s Historical Calendar Year Revenue Growth

Source: Koyfin as of 29th August 2024. Blue bar is forecasted calendar year end revenue estimate. Historical performance is not an indication of future performance and any investments may go down in value. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Despite these strong numbers, Nvidia’s stock initially dropped by 8% in after-hours trading, eventually settling around $120 per share. This reaction reflects the heightened expectations investors have placed on Nvidia following a series of 'blowout' quarters. While Nvidia's performance was solid, it wasn’t spectacular enough to appease investors given its high valuation. Investors appear to be recalibrating their expectations as Nvidia's guidance didn’t significantly exceed to the upside as it had done in the past. This adjustment hints at concerns that the company’s exponential growth may be beginning to slow, leading some investors to take profits.

Key Earnings Call Highlights

During the earnings call, Nvidia’s CEO, Jensen Huang, provided insights into the future of the company and the broader AI market. A significant portion of the discussion focused on the ramp-up of Blackwell GPUs, expected to drive several billion dollars in revenue in Q4 20243. Huang also emphasized the growing importance of modernizing data centers with Nvidia’s accelerated computing capabilities. He highlighted the cost savings and efficiency gains that can be achieved by transitioning from CPU-based infrastructure to GPU-accelerated systems, calling it a ‘trillion dollar opportunity’.

However, questions remain regarding the return on investment for Nvidia’s major customers, particularly the cloud service providers. Despite record capital expenditures, there has not yet been any apparent impact on revenue for these companies, raising concerns about the returns on these big bets on AI.

Broader Market Implications

Nvidia’s earnings and the market's reaction underscore broader trends and challenges in the semiconductor and AI industries. While AI has revitalized the semiconductor market, its cyclical nature raises concerns about the sustainability of this growth. Nvidia’s stock, with a higher valuation multiple compared to peers, could face significant contraction in the face of any headwinds.

The AI arms race amongst tech giants is driving massive capital expenditures, particularly in building 'AI factories' equipped with the most advanced computing hardware to train large language models. Huang emphasized that constructing ‘AI factories’ involves more than just GPUs—it requires a comprehensive suite of hardware, software, and systems designs expertise. This complexity highlights the need for end-to-end solutions to build efficient accelerated computing infrastructure. So far, Nvidia has been the only player uniquely positioned to serve this demand. However, competitors like AMD are making strategic moves, such as acquiring ZT systems to enhance their own end-to-end system design capabilities4. Furthermore, the success of these AI factories will depend not only on Nvidia or AMD designed GPUs, but also on other critical players in the AI value chain, such as SK Hynix and Micron, which supply essential memory chips for AI computing.

The key question for investors is when this AI-driven growth will begin to normalize or become more evenly distributed across other ecosystem players. As more entrants grab market share and sales growth potentially slows due to market saturation or supply chain challenges, a repricing of Nvidia’s stock is possible. The cyclical nature of the semiconductor industry suggests this is more a question of when, not if. This concern is heightened by the industry's reliance on a concentrated list of manufacturers, namely Taiwan Semiconductor, which is currently the only one able to produce the most advanced chips.

Figure 2: Semiconductor Market Cyclicality, Revenue Growth by Calendar Year for 10 Largest Firms by Market Cap

Source: Koyfin as of 29th August 2024. Blue bar is forecasted calendar year end revenue estimate. Historical performance is not an indication of future performance and any investments may go down in value. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Importance of the Semiconductor Ecosystem for AI

While Nvidia's garners a lot of attention in the semiconductor space, the entire semiconductor ecosystem is foundational to both AI and modern technology. In 2023 alone, revenue for the top 10 semiconductor firms surpassed $300 billion, up from $150 billion in 2014, highlighting the industry’s critical role in society as well as its long-term growth potential.

Figure 3: Semiconductor Revenue (USD, Mn) by Calendar Year, 10 Largest Firms by Market Cap

Source: Koyfin as of 29th August 2024. MU represents Micron Technology, AMD represents Advanced Micro Devices, NXP represents NXP Semiconductors, INTC represents Intel, TSMC represents Taiwan Semiconductor, AVGO represents Broadcom, TXN represents Texas Instruments, ADI represents Analog Digital, QCOM represents Qualcomm, NVDA represents Nvidia. Historical performance is not an indication of future performance and any investments may go down in value.

As NVIDIA continues to grow in dominance within the semiconductor landscape, the long-term success of AI also relies on the development of various other chips, networking equipment, and software that work along with GPUs, enabling the training of multi-billion parameter AI models. As investors, we must acknowledge the importance of the sector as a whole and the interconnected nature of the devices that enable technologies like AI.

Beyond Hardware

The next phase of the AI revolution will likely be driven by software and applications. Nvidia is aware of this, as their success hinges on the success of their customers. Nvidia is partnering with major companies like ServiceNow, SAP, and Snowflake to develop AI copilots and other AI-powered software solutions5. Customers like Foxconn and Mercedes-Benz are using Nvidia’s Omniverse Cloud to build digital twins for industrial applications5. Amgen and Recursion Pharmaceuticals are using Nvidia’s BioNeMo toolkits for Ai-enabled drug discovery6. The applications of AI are endless, and Nvidia seems to be partnering with everyone, across all domains.

Investment Perspective

It is clear Nvidia remains a dominant player in the AI and semiconductor space. However, given the market's reaction to its latest earnings, it may be prudent for investors to diversify their exposure across the broader AI ecosystem. While Nvidia’s prospects are strong, there are significant opportunities in other areas of the AI value chain, particularly in software.

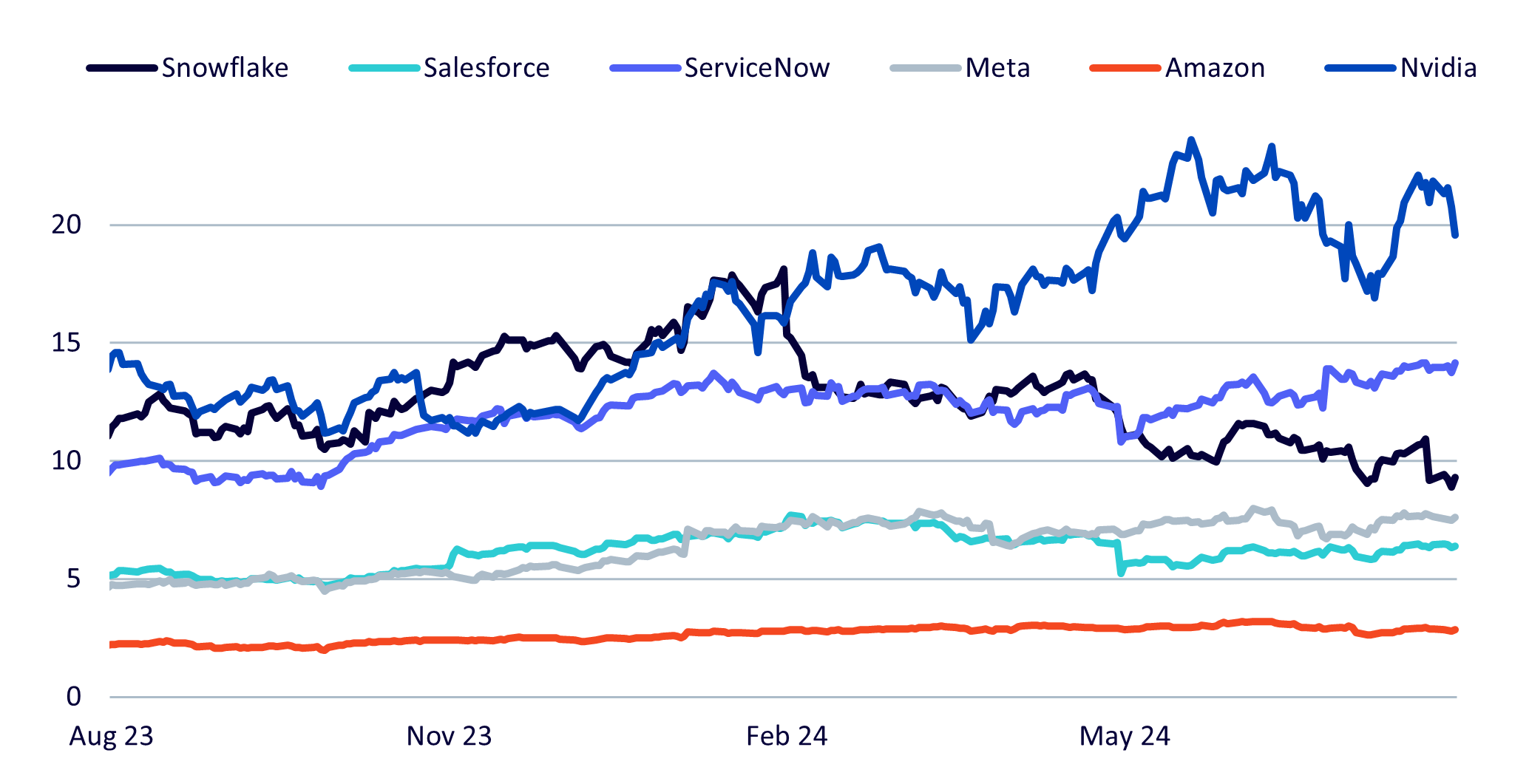

Companies like Amazon, Meta, and Salesforce, which are key players in AI software, are currently trading at less than half the sales multiple of Nvidia. Similarly, companies like Snowflake have seen their valuations contract significantly as the market reacted to weakened outlooks driven by economic slowdown and tighter enterprise spending. This temporary downturn could present an attractive entry point for investors looking to diversify as these companies continue to build out their AI offerings. As the AI market matures, spreading investments across different segments could provide a more balanced approach to capturing the long-term growth potential of AI.

Figure 4: Enterprise Value to Forward Sales Ratios, Select Software Firms vs. Nvidia

Source: Bloomberg as of 29th August 2024. Historical performance is not an indication of future performance and any investments may go down in value.

Conclusion

Nvidia’s latest earnings report was strong, but the market's reaction suggests that investors are becoming more cautious about the company's future growth prospects. While Nvidia continues to lead in the AI hardware space, the broader question remains how long this growth can be sustained. As the AI revolution unfolds, investors should consider a diversified approach, taking into account the entire AI ecosystem, from hardware to software, to maximize their portfolios’ potential for capturing the 'next industrial revolution' - the AI revolution.

1 Bloomberg as of August 29, 2024

2 Koyfin, as of August 29, 2024

3 Q2 2025 Nvidia Earnings Call, August 28, 2024

4 https://ir.amd.com/news-events/press-releases/detail/1211/amd-to-significantly-expand-data-center-ai-systems

5 Q2 2025 Nvidia Earnings Call, August 28, 2024

6 https://www.fiercebiotech.com/medtech/nvidia-expands-drug-discovery-footprint-new-amgen-recursion-alliances