What's Hot: Copper's conductive forces

Key Takeaways

- Tariff Anticipation Fuels Rally: The U.S. may impose 25–50% tariffs on copper imports under a national security review, leading to aggressive metal inflows and stockpile build-up in COMEX warehouses.

- Tight Market Signals: LME copper is in steep backwardation—spot prices well above futures—highlighting acute short-term supply tightness.

- COMEX Outperformance: U.S. copper prices have surged 25% YTD versus 13% on the LME, with a 13% premium already pricing in potential tariffs.

- Supply Disruptions Amplify Deficit Risks: Mines in the DRC and Chile face output cuts, and the ICSG now reports an April deficit, suggesting a shift to full-year shortage.

- Strong Chinese Demand Meets Supply Stress: China's power grid investments and plunging TC/RCs (now even negative) underscore rising demand and raw material scarcity.

Widespread expectations that the U.S. Department of Commerce's Section 232 (s232) investigation on copper will result in import tariffs later this year have ignited aggressive positioning in copper markets. The Section 232 study, launched in February 2024, is designed to assess whether copper imports pose a threat to U.S. national security. A similar study previously led to substantial tariffs on aluminium and steel. If copper is deemed critical to domestic security—given its essential role in defence, electrical infrastructure, and clean energy—the U.S. may impose protective tariffs as high as 25% or even 50%.

As anticipation builds, traders are moving metal into the U.S. at an unprecedented pace. The impact is visible in inventory trends: COMEX warehouse stocks have ballooned, while inventories on the London Metal Exchange (LME) and Shanghai Futures Exchange (SHFE) have drained rapidly.

Source: WisdomTree. Bloomberg. June 2024 to June 2025. Historical performance is not an indication of future performance and any investments may go down in value.

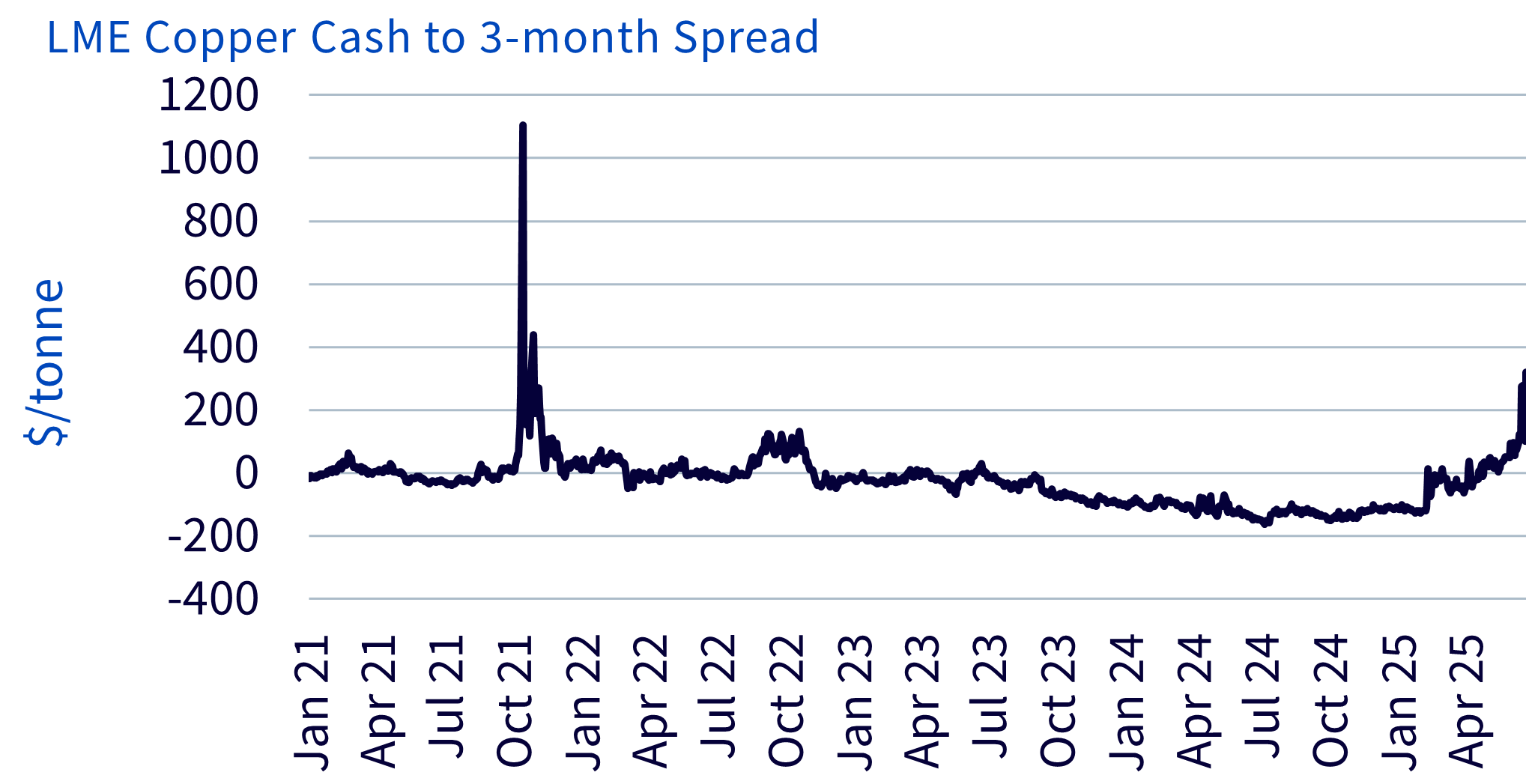

Distortions in Market Structure: LME Backwardation Signals Tightness

The frantic movement of physical copper is distorting the market’s pricing structure. On the LME, spot prices are now trading at their highest premium to 3-month prices since 2021, a classic backwardation signal. This condition reflects localized supply shortages, in contrast to the usual contango where future prices trade at a premium to spot.

Source: WisdomTree. Bloomberg. January 2021 to June 2025. Historical performance is not an indication of future performance and any investments may go down in value.

COMEX Price Outperformance and Tariff Premiums

COMEX copper has rallied 25% year-to-date, compared to a 13% gain on the LME. This relative outperformance reflects the market's pricing-in of potential U.S. tariffs. As of late June:

- COMEX copper trades at $5.0480 per pound, or about $11,127 per metric tonne

- LME copper stands at $9,889 per metric tonne

That equates to a 13% premium for COMEX over LME prices. If a 25% tariff is implemented, COMEX prices could climb further to close the gap. In the event of a 50% tariff (as seen with aluminium), the upside for U.S. prices could be significantly larger.

Beyond Tariffs: Tightening Fundamentals Support Prices

The U.S. tariff speculation isn’t the only bullish force in the copper market. The International Copper Study Group (ICSG) reported that refined copper shifted into a 50,000-tonne deficit in April 2025, after months of surplus. Although the cumulative 2025 balance remains a surplus of 233,000 tonnes, the trend appears to be reversing.

That trend is being reinforced by a string of supply disruptions:

- Ivanhoe Mines has cut 2025 guidance by 28% at its Kamoa-Kakula complex in the DRC due to seismic-related flooding. New mine plans have been introduced, and 2026 guidance has been withdrawn entirely.

- Teck Resources' Carmen de Andacollo (CdA) mine in Chile faced a mechanical shutdown in June, expected to last about a month. Teck aims to minimize the impact via rescheduled maintenance, but there is still uncertainty around annual output.

Given these developments, we expect the copper market to shift into a full-year deficit, and forecast that ICSG will revise its surplus projection to a deficit in its next update due October 2025.

Demand-Side Tailwinds: China’s Grid Boom

On the demand side, China is pouring record investment into its electrical grid. Grid expansion entails installing copper-intensive transmission and distribution cabling, providing a robust structural demand backdrop.

Source: WisdomTree. Bloomberg. January 2010 to May 2025. Historical performance is not an indication of future performance and any investments may go down in value.

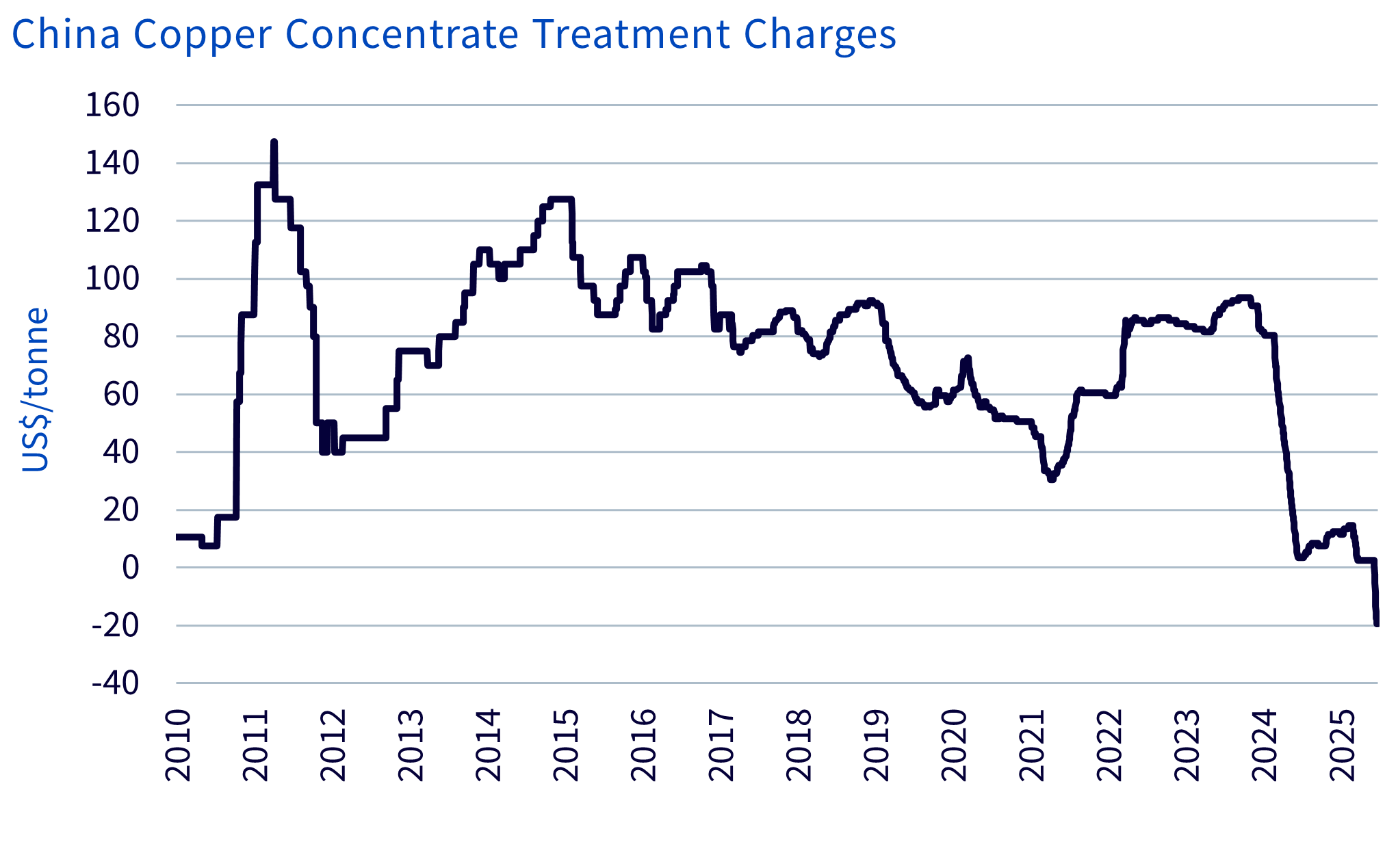

China's Refining Economics Reflect Supply Stress

In a sign of raw material scarcity, copper treatment and refining charges (TC/RCs) in China have fallen below zero. This implies that smelters are effectively paying miners to secure copper ore, due to insufficient concentrate supply and overcapacity in smelting.

On June 27, Reuters reported that Antofagasta agreed to a zero TC deal with Chinese smelters—a record low (but actually a positive surprise that it was not negative). The willingness of smelters to accept such punitive terms may be offset by the value of byproducts like gold and silver, which are extracted alongside copper in refining processes and can help cushion losses.

Source: WisdomTree. Bloomberg. January 2010 to June 2025. Historical performance is not an indication of future performance and any investments may go down in value.

Conclusion: Bullish Outlook with Policy and Structural Drivers

Copper prices are being supported by a rare combination of factors: anticipated trade policy shifts, physical market tightness, production downgrades, and strong Chinese infrastructure demand. If the U.S. imposes tariffs on copper, the price divergence between COMEX and global benchmarks could widen further, especially in a tightening supply environment. All signs point to a bullish trajectory in the second half of 2025.