Nickel rally defies industrial metals rut

Nickel has rallied 54% in the last three months to US$18,175/tonne, compared to 1.4% for the Bloomberg Industrial Metals sub-index (to 12 September 2019), in part as a result of the ban on nickel ore exports from Indonesia that will be implemented in January 2020. Nickel is a silvery-white metal that is known for its ability to make steel and other alloys better able to withstand extreme temperatures and corrosive environments. After this recent strong rally, it is also now getting a reputation for strengthening people’s investment portfolios. We don’t believe that nickel’s upside is over, but the next leg of gains may take more time to crystallise.

Nickel is already in one of the deepest supply deficits of all base metals. But a ban on Indonesian ore exports that was expected in 2022 has been brought forward to January 2020. That could leave nickel markets severely undersupplied. Although there is enough inventory to meet short-term needs, there is a risk of deepening deficits.

Figure 1: Metal supply in deficit

Source: International Copper Study Group, International Nickel Study Group, International Lead and Zinc Study Group, WisdomTree, data available as of 2 September 2019.

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Why is the Indonesian government banning ore exports?

The government wants to control more of the nickel supply chain. With electric vehicles and the batteries that power them acting as a positive shock to nickel demand, the Indonesian government wants to strategically position the country for the forthcoming increase in demand for the finished metal. By banning the exports of the ore it hopes to encourage more processors and smelters to set up operations in Indonesia, before they export the finished nickel product. It’s a risky policy – one that they tried between 2014 and 2017 with a lack of success. In 2017 the ban was placed on pause until 2022, but the decision in August 2019 has brought that forward to January 2020.

Figure 2: 2018 nickel mine production (2.3 million tonnes)

Source: US Geological study, WisdomTree, data available as of 2 September 2019.

Historical performance is not an indication of future performance and any investments may go down in value.

Long-term prospects for Nickel

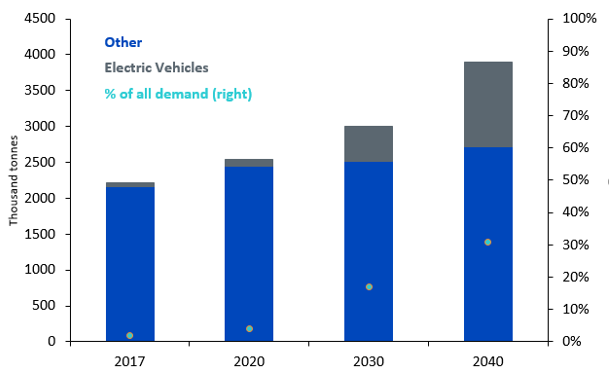

We maintain a long-term bullish view on the metal in light of demand from the battery market (see Electric Vehicle adoption to augment commodity demand). Although that is a long-term story, projections from Wood Mackenzie indicate the nickel market could grow from a 2.3mn tonne market to close to a 4mn tonne market by 2040. Over that time frame nickel used in battery applications is forecasted to rise from under 5% of nickel demand to over 30% of nickel demand.

Figure 3: Total primary nickel demand

Source: Wood Mackenzie.

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties

However, prices languishing around $12,000/tonne, as they were in June 2019, would not have been enough to start the projects desperately needed to get nickel out the ground as demand is expected to ramp up in coming years. With prices now over $18,000/tonne, the likelihood of projects starting has improved. That price gain is probably still not enough to encourage the scale of mining needed to get enough metal out of the ground to meet future battery demand, but it is a start in the right direction.

New mining projects - with notoriously long lead times – are unlikely to alleviate short-term tightness, but inventory can be drawn on in the short-term.

Inventory is not limitless. Judging by the shape of the nickel futures curve – which is in backwardation until 2022 – inventory for the metal is tight. So, we think prices have further to rise, possibly above $24,000/tonne in the long-term to be able to unlock the amount of nickel needed by the market over the next decades. But adding $6,000/tonne to today’s price may take a lot longer than the 3 months taken to accumulate the last $6,000/tonne. We are now a playing a long-term game, with the short-term Indonesian ore ban story now largely priced-in.

Related blogs

+ Electric Vehicle adoption to augment commodity demand

Related products