Electric Vehicle adoption to augment commodity demand

Last year global Electric Vehicle (EV) sales surpassed the 2.3% penetration rate in the auto industry. Tighter emission regulations coupled with greater advancement in battery technology are spurring the adoption of EVs which we believe has the potential to favourably impact the demand for commodities such as nickel and copper.

Evolution within battery technology

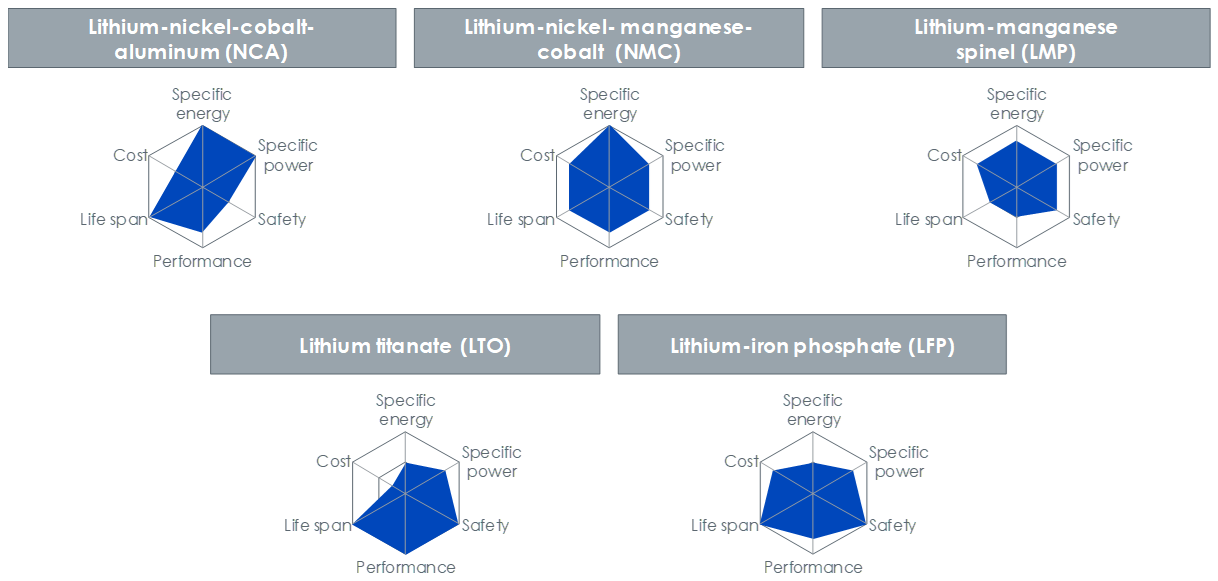

Lithium-ion batteries (LiBs) are the most widely used batteries in EVs owing to their high energy density. These batteries adopt a range of chemistries that employ various combinations of anode and cathode raw materials. Currently the five most advanced technologies used in the cathode of LiBs are: Lithium Manganese Oxide (LMO), Lithium Cobalt Oxide (LCO), Nickel Cobalt Aluminium (NCA), Nickel Manganese Cobalt (NMC) and Lithium Iron Phosphate (LFP). Some of these, such as NCA and NMC, are also amongst the most widely accepted technologies. This can be seen on figure 1.

Figure 1: Five most widely accepted Lithium based battery technologies:

Source: Boston Consulting Group (BCG) as of December 2018

Each of the above lithium ion technologies can be compared along six dimensions: safety, lifespan, performance, specific energy, specific power and cost. Safety is by far the most important criterion for LiB. Battery producers face a constant tug of war between cost and safety as no single technology delivers on all six dimensions. While the NCA boasts of high performance it poses safety challenges, the LFP ranks high on safety but it has lower specific energy. While battery technology has taken great strides, there is no single technology that ranks highly on all six dimensions. Battery technology remains in a constant struggle to find the right chemistry to achieve the optimum performance across all six dimensions.

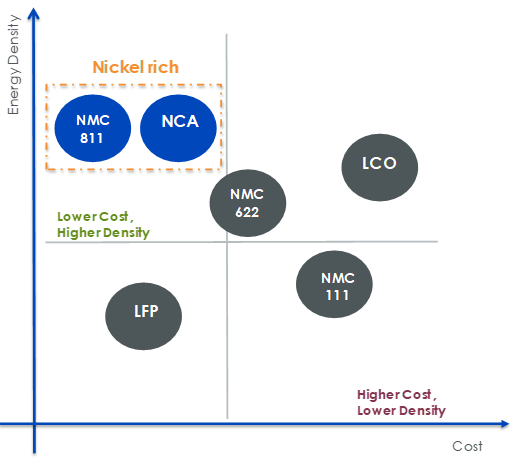

Nickel’s demand bolstered by shifting battery mix

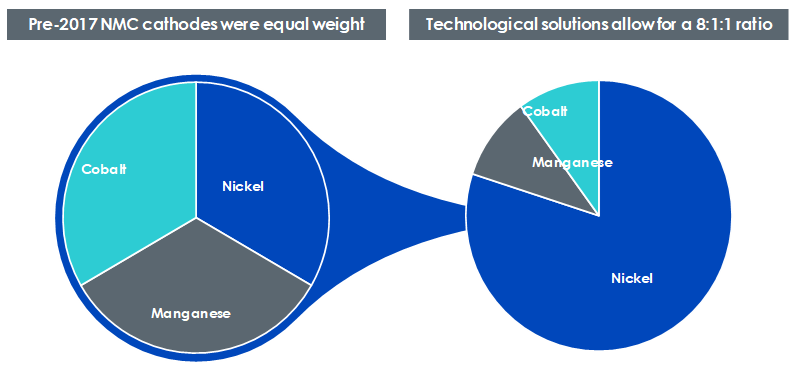

Prior to 2017, the NMC battery that contained equal parts of nickel, cobalt and manganese (in a ratio of 1:1:1) gained widespread acceptance among manufactures. Battery manufacturers are now changing the composition ratios of these metals and are favouring a higher proportion of nickel. Implementing a higher proportion of nickel provides the benefit of higher energy in the batteries over long distances and makes the batteries lighter. However, the lifetime of these batteries is short.

Figure 2: Higher portions of nickel favoured in the NMC battery

NMC: Nickel Manganese Cobalt, NCA: Nickel Cobalt Aluminium, LCO: Lithium Cobalt Oxide, LFP: Lithium Iron Phosphate. Source: Vale, WisdomTree as of December 2018

Added to that, higher nickel ratios reduce battery manufacturers dependence on cobalt. Most of the world’s supply of cobalt arises from the Democratic Republic of Congo. Owing to the country’s political instability combined with human rights spotlight on child labour, a large portion of the world’s supply of cobalt remains at risk.

Figure 3: Evolution of battery technology favour’s higher nickel content

Source: WisdomTree as of December 2018

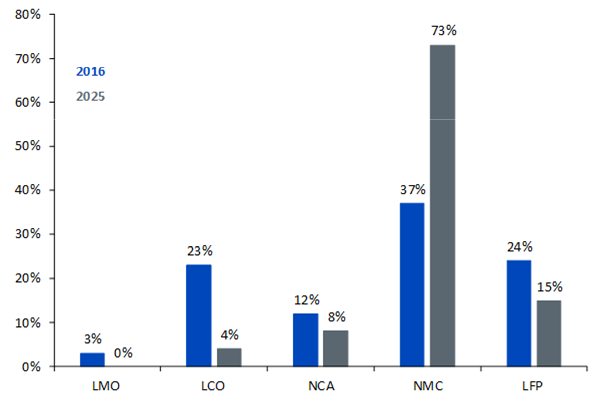

According to Roskill and Benchmark Mineral Intelligence (BMI), NMC batteries featuring higher nickel proportions of 5:2:3 and 6:2:2 are already in use and manufactures are pushing to commercialise the NMC 8:1:1. However the NMC’s 8:1:1 highly stringent requirement in terms of dust, moisture and contamination control are holding back efforts to make the battery commercial. NMC 8:1:1 is expected to gain significant market share in the EV market by 2020 evident from the chart below which supports higher demand for nickel.

Figure 4: Nickel’s demand outlook supported by commercialisation of NMC battery

LCO: Lithium Cobalt Oxide, LMO: Lithium Manganese Oxide, NCA: Nickel Cobalt Aluminium, NMC: Nickel Manganese Cobalt, LFP: Lithium Iron Phosphate.

Source: Mc Kinsey, WisdomTree as of September 2018.

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Demand for copper bolstered by EV infrastructure growth

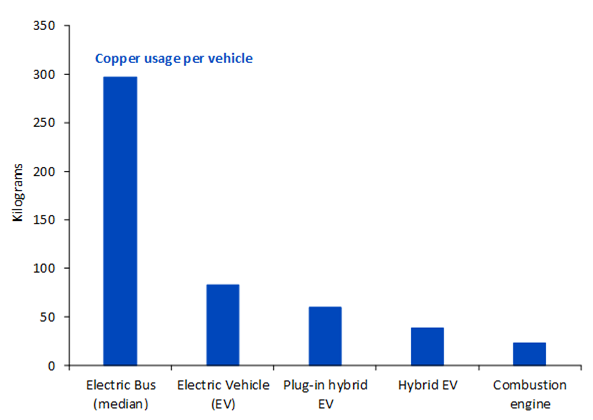

In the case of Copper, the additional amount of copper required for an electric vehicle compared to an internal combustion engine justifies the growth in demand. While a traditional vehicle would require 23kgs of copper, a pure battery electric vehicle will require nearly 83kgs of copper which amounts to nearly 20 – 60 kgs more copper usage in comparison to a vehicle with a combustion engine. A pure battery powered electric bus, contingent on the battery size is expected to require nearly 224-369kgs of copper. However, copper is not only needed in the vehicle itself but is also required for generating electricity, for the power grid and for the charging stations. While the lion’s share of copper’s demand nearly 73% stems from the vehicles themselves an additional 13% would be required for generating electricity and for the grid infrastructure and 4% for the grid storage. According to the International Copper Association (ICA), as additional 100,000 tons of copper would need to be discovered to equip the 40 million additional charging stations that are needed to support the adoption of EVs globally.

Figure 5: Copper usage by vehicle type

Source: International Copper Association, WisdomTree, data as of September 2018

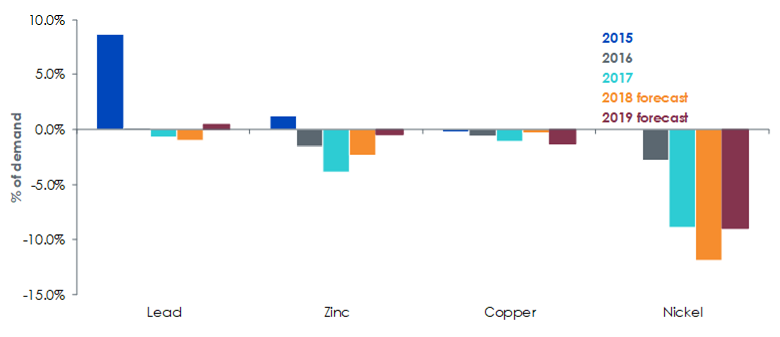

Fundamentals support copper and nickel

The EV hype has allowed smaller elements such as lithium and cobalt to stage a stronger price performance over the last few years in comparison to the base metals such as copper and nickel. In 2018, copper and nickel saw lacklustre price performance due to the uncertainty surrounding trade wars despite supportive fundamentals. According to the International study groups, copper and nickel are expected to remain in a supply deficit in 2019. Since the start of this year, industrial metals including copper and nickel have risen considerably largely driven by the de-escalation of trade wars between the US and China. However, we believe its underlying supportive fundamentals coupled with the stronger demand story from the EV industry strengthens the outlook for both nickel and copper over the long run.

Figure 6: Metals supply in a deficit

Source: International Copper Study Group (ICSG), International Nickel Study Group (INSG), International Lead and Zinc Study Group (ILZSG), WisdomTree data as of November 2018.

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Related blogs

+ Electric Vehicles are ICEing traditional cars

Related products