Diversified and Enhanced Commodities Investing: Part I: How to lower volatility

- Single commodities are subject to specific and sometimes unique factors which drive price trends to be distinct and for volatility to be elevated.

- The probability of historic average positive and negative returns can help better conceptualise volatility and the dispersion of returns of different asset classes.

- Mixing single commodities to form a broad diversified commodity exposure can significantly reduce volatility compared to single commodities and broad equities.

In this first instalment, we take a closer look at some of the most important drivers responsible for the volatility seen in single commodities and how to mitigate with commodities diversification.

Cyclicality

The forces driving volatility of single commodities are typically unique. Consider copper for example: Cyclical turning points in the economic and business cycle can overwhelm investor sentiment and shift latent secular trends. During the commodities boom instigated by China’s investment spending splurge from 2001 to 2007, copper futures rose 260%, 10 times as fast as the S&P 500. Copper’s marked price reversal since 2010 and the sharp price swings since, shows just how significant expectations around China’s outlook on export and infrastructure spending drive the soft / hard landing rhetoric and how closely tied they are into industrial metals sentiment.

Seasonality

Another factor driving volatility is seasonality and abnormal weather conditions, particularly prevalent in energy and agricultural sectors. Several snaps of cold weather in the US that extended into the spring and tightened and disrupted energy supply conditions in recent years have distorted prices of US natural gas futures, instigating shifting futures curves. With this has come large price swings as was seen in 2012 and 2013 when March contracts rolled over into April contracts. Other adverse weather conditions such as the severe droughts that devastated farmland and crops in the US, Russia, Egypt in recent years, which led to temporary – but large shortages – also contributed to isolated but volatile price moves in food staples such as corn and wheat without affecting energy, precious and industrial metals. Supply and demand shocks reverberate around futures curves shifting in contango and backwardation will amplify volatility.

Regulation and Technology

Regulatory freedom and technology are further examples for why, within certain commodity sectors, price trends appear insulated from global macro trends. The relative ease with which new technologies to extract mineral fuels such as hydraulic fracturing in shale formations have been adopted and scaled-up in the US has reinforced the decoupling of US natural gas prices from not just crude oil prices but also European natural gas prices. For instance, using OECD’s benchmark of average natural gas prices for Europe’s fragmented energy markets, US natural gas has been trading at a more than 60% discount to European natural gas effectively since 2010.

“Financialisation”

Reinforcing the distinct price trends in single commodities has also been the “financialisation” of commodity markets, through the development of exchange traded products (ETPs). These vehicles have unlocked large pools of wealth from retail and institutional investors., As a result, price discovery underpinned by the fundamental supply and demand expectations of primarily commercial traders is increasingly being affected by investors of different types. Strategic asset allocators as well as day traders and speculators now more often than not reinforce if not overwhelm, or on occasion disrupt trends in commodity prices.

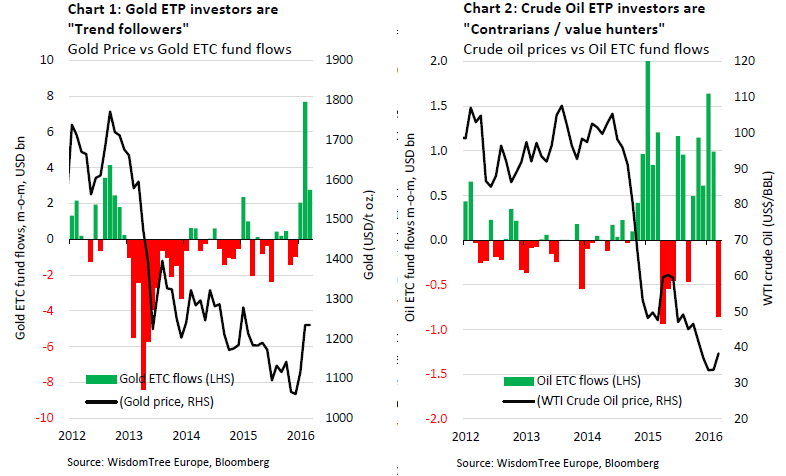

For instance, Chart 1 shows trend following and herd-like behaviour by investors, buying into gold when prices rise and selling out of gold when prices fall, exacerbating volatility along the way. For instance, while in 2013 gold futures fell 28% as investors redeemed $38 billion from gold ETPs, this year to end of March, gold futures’ rise of 16% coincided with investors pouring some $12.5 billion back into gold ETPs.

On the other hand, oil ETP investors tend to be contrarian, with a strategic, if not default allocation to crude oil: when crude oil prices rise, investors cut back, when crude oil prices fall they typically top-up their allocation in crude oil ETPs. For instance when WTI crude oil fell 77% from its peak in July 2008 to its February low of 2009, US$ 6 billion flowed into oil ETPs in the same period. And during the dramatic drop of crude oil from over 100 US$/bbl since July 2014 to below 40 US$/bbl by the end of March this year, crude oil ETPs saw nearly US$ 10 billion of inflows.

If flows of value hunters failed to work as a shock absorbing counterforce to crude oil’s sharp price swings, then increased speculative positioning by hedge funds and proprietary trading desks is likely to blame for much of the elevated volatility in some commodity markets. On NYMEX earlier this month, approximately 28% of open interest of derivatives contracts on WTI crude oil (futures and options mainly) were held on a non-commercial, i.e. speculative basis, up from 14% just 5 years ago. In China, a crackdown by regulators is currently underway to curtail excessive speculation in industrial metals, most notably steel where in spite of widespread excess capacity futures of rebar steel have rallied.

So with this volatility, what is an investor to do?

Chart 3 describes the volatility of major benchmarks covering equities, fixed income and commodities in two ways. First, the blue diamonds show the annualised standard deviation of weekly returns since 2001. Ranked from lowest to highest within each asset class, the benchmarks displaying the least volatility are shorter dated government debt in developed, low inflation countries (far left), with standard deviations of less than 3% for 1 to 5 year UK gilts and Japanese government debt for instance. Moving up the volatility spectrum, standard deviations hovering around 18% are prevalent in major developed market equities, with readings typically exceeding 20% in the narrower, cyclical benchmarks such as the DAX 30, NASDAQ 100 and Hang Seng. However, it is within commodities where the volatile return pattern is most pronounced. Crude oil futures – whether WTI or Brent – are amongst the most volatile benchmarks within commodities and, as displayed on the far right of the chart, have standard deviations of more than 30%[1].

Second, a more approachable way to conceptualise volatility is to profile the historic weekly returns dispersion as shown in the candlestick chart (dark grey), with the ends of the vertical thick bars indicating the cut-off, and the end-points of the thin lines the average of the bottom and top 10% (10th percentile and 90th percentile respectively) of weekly returns since 2001. A 35% standard deviation for WTI crude oil is high -- the the average weekly return of around 8% occurred approximately 10% of the time, with the same probability also for average weekly returns of around -8%. This is indicated by the top and bottom ends of the thin line in the candle stick chart for WTI crude oil. In other words, if history is any guide, there is a 1 in 5 chance investors stand make or lose 8% on average, when staying invested in WTI crude oil for a week.

The 10% and 90% decile of weekly returns distribution (i.e. the ends of the thin minimum bars), describe volatility as a measure of returns dispersion in slightly different way. Here, for both WTI and Brent crude oil there is a 1 in 5 chance that investors stand to gain or lose at least 5% on a weekly basis. This stands in marked contrast to UK equities, where there is a 1 in 5 probability that investors will stand to make or loose around half as much as on crude oil on average on a weekly basis, (i.e. around +4% and -4%, respectively), or to make or lose around 2.3% a week. [1] Left out for reasons of scalability, US natural gas is probably the most volatile across energy and commodities in general, having annualised standard deviation of 48%.

When individual commodities join the larger basket

Once single commodities such as crude oil, copper, gold and wheat are mixed into a broad commodities basket, then the volatility is markedly reduced. Chart 3 shows that the weekly excess returns of Broad Commodities[1] -- a broad basket of energy, industrial metals, precious metals and agricultural commodities - has an annualised standard deviation of 15.6%, 10% lower than copper, almost 14% lower than wheat, and 15% lower than crude oil. To phrase this differently, historic weekly returns since 2001 suggests that there is a 1 in 5 chance investors stand to make or lose at the minimum around 2.5% on a weekly basis, which compares to the volatility that investors would historically have been exposed to when investing in the UK large-cap equity market[2]. Because of the unique drivers of returns of single commodities volatility has historically exceeded most equity markets. However, once mixed into a broad basket of other single commodities, investors get access to an asset class that, once diversified, significantly reduces its volatility. Investors sharing this sentiment may consider the following UCITS ETFs.

- WisdomTree Enhanced Commodity UCITS ETF – USD (WCOG)

- WisdomTree Enhanced Commodity UCITS ETF – USD Acc (WCOA / WCOB)

[1] Bloomberg Broad Commodities Index (BCOM)

[2] FTSE 100.