Europe deflation and US rate hike risks: It’s paradoxically bullish for gold and silver

Deflation - not inflation; policy tightening - not easing is, ironically, giving gold and silver momentum. Here is why.

Deflation is destabilising state finances, creating uncertainty, mainly in the Eurozone. Meanwhile, the broad-based US expansion is fuelling expectations of when, not if, the Fed hikes interest rates.

Chart 1 summarizes these risks posed to fixed income markets in the US and Europe. The analogy of why this is bullish for precious metals follows next.

Worsening creditworthiness in Europe, rising risks of rate hikes in the US

Europe is at risk of facing entrenched deflation, worsening the creditworthiness of sovereigns of indebted members of the Eurozone in particular. With the disinflationary trend having already slowed down efforts of households and governments in Europe to pay down debt and deleverage the balance sheet in the last couple of years, deflation will work to reverse such efforts altogether: the value of outstanding debt will rise in real terms even as incomes are cut. The incentive to delay spending reinforces the cuts to household’s disposable income and government’s tax receipts. With deflation in Greece becoming more entrenched (core CPI of -1.6% y/y and headline CPI of -2.6% y/y for December 2014), there is no leeway for the government to loosen budgets or relax some of the austerity measures. If this means further political instability as populist fringe parties opposed to austerity gain in the polls, Greece is edging ever closer to the exit from the EMU. In the event this actually occurs, it will trigger an inflation shock as Greece reinstates its own currency and devalues. If there is any fundamental driver for gold to regain strength then, besides the recent comments made by German officials openly suggesting that a Greece exit is manageable, it may be because of the looming prospects of recurring hyperinflation in Europe’s periphery. The bond markets of Europe’s indebted economies of Italy and Spain have rallied over the last few years. This to the point that their low bond yields now compare poorly against not just their own deteriorating credit metrics, but also against the rising contagion risk of Greece. Deflation and upcoming elections are driving it. At the moment, bond investors are still pricing in positive inflation (see chart 1), but the falling trend portends more disappointment if the actual CPI readings confirm deflation over the months ahead. Then there is the risk of a US policy interest rate hike. The US economy is in broad-based expansion, but inflation so far has failed to climb closer to the 2% target. Coupled with lacklustre wages, the US recovery appears incomplete. It compels the Fed to delay the rate hike until inflation is firmly entrenched in the US economy. But the mere speculation of when, not if, the Fed is going to raise rates is enough to make investors nervous about US Treasuries. For instance, the yield on 2Y US Treasuries, widely regarded as the barometer for where US policy rates are headed, has over a volatile course in the last 6 months gradually risen to 50 bps. The yield is now more than double the level seen before the ‘taper talk’ in May 2013.

Bond yields are negative or too low on a risk-adjusted basis

The risk of deflation in Europe and a policy rate hike in the US has led to increasingly dislocated yields on bond markets. The safe havens in core Europe, which next to government debt of Germany include that of France and a few smaller members in Europe’s northern hemisphere, offer next to no yield on long maturities, and sub-zero yields on short maturities. For instance, any German investor looking to preserve capital for the next 2 years by buying a 2 year German government bond would do so only if he/she expects Germany to enter deflation that will last until 2016. If not, then it’s the German government, not the investor, who will be making money on the negative yields the 2 year German government bonds currently offer. In the US, the prospect of the Fed raising interest rates is likely to have driven fixed income investors to shift allocations away from the policy sensitive shorter dated debt and into longer dated debt, helping yields on longer dated US Treasuries to fall further. But behind the bullish trend in longer dated US Treasuries masks rising uncertainty. Evidence for the unease is the rise of 10Y US Treasuries’ implied volatility which, at around 7% suggests sentiment is as downbeat as during the 2013 ‘taper talk’ (see chart 1). Hence, within European government bonds, the choice is between zero to negative yields in the core and low but riskier yields in the periphery. Within US Treasuries, the choice is between rising uncertainty priced in long dated maturities and the volatile and rising yields n short dated maturities.

Source: WisdomTree Europe, Bloomberg. Data as at 12 January 2014

Tactically positioning: bearish US fixed income, bullish precious metals

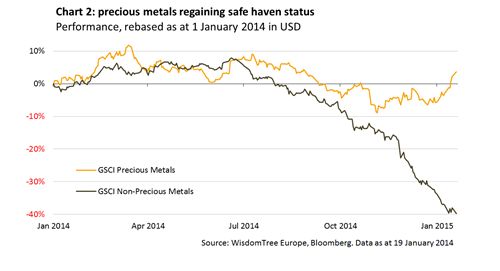

Given the downside risk to peripheral European and US government fixed income markets and the record low yields on offer, precious metals are regaining some of their lost appeal as investors seek alternative safe haven assets. As chart 2 shows, precious metals have regained ground after their downtrend since the summer and have steadily broken away from the collapse in energy and industrial metals commodities. This year precious metals are up 10%, even as non-precious metals are down 10%. Gold and silver may continue to gain in an environment where fixed income can offer negative yields or insufficient yield on a risk adjusted basis.

Tactically, investors sharing this sentiment may want to consider the following long precious metals ETPs:

Tactically, investors sharing this sentiment may want to consider the following short fixed income ETPs: